Mercury Insurance 2010 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2010 Mercury Insurance annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

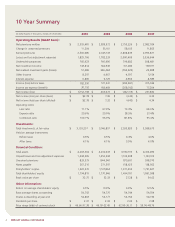

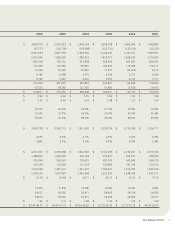

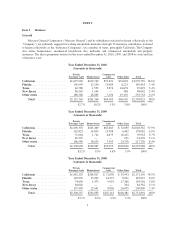

The Company experienced favorable development of approximately $13 million on the 2009 and prior

accident years’ losses and loss adjustment expenses reserves due primarily to the result of re-estimates of

accident year 2009 California BI losses. See “Critical Accounting Estimates—Reserves” in “Item 7.

Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

For the year 2008, the Company experienced favorable development of approximately $25 million on prior

accident years’ losses and loss adjustment expenses reserves. The favorable development is primarily due to the

result of re-estimates of accident year 2008 and 2007 California BI losses, partially offset by unfavorable

development from earlier accident periods.

For the years 2005 through 2007, the Company experienced unfavorable development of approximately

$107 million to $147 million on prior accident years’ losses and loss adjustment expenses reserves. The

unfavorable development from these years relates primarily to increases in loss severity estimates and loss

adjustment expense estimates for the California BI coverage as well as increases in the provision for losses in

New Jersey and Florida. Reserves from these years showed further unfavorable development after December 31,

2008 primarily as a result of re-estimates of the 2005 and 2006 accident year loss reserves in New Jersey and

re-estimates of the 2005 and 2006 accident year loss adjustment expenses reserves in New Jersey and California.

For 2004, the unfavorable development relates to an increase in the Company’s prior accident years’ loss

estimates for personal automobile insurance in Florida and New Jersey. In addition, an increase in estimates for

loss severity for the 2004 accident year reserves for California and New Jersey automobile lines of business

contributed to the deficiencies.

For 2003, the favorable development largely relates to lower inflation than originally expected on the BI

coverage reserves for the California automobile line of insurance. In addition, the Company experienced a

reduction in expenditures to outside legal counsel for the defense of personal automobile claims in California.

This led to a reduction in the ultimate expense amount expected to be paid out and therefore favorable

development in the reserves at December 31, 2003, partially offset by unfavorable development in the Florida

automobile lines of business.

For years 2000 through 2002, the Company’s previously estimated loss reserves produced deficiencies that

were reflected in the subsequent years’ incurred losses. The Company attributes a large portion of the

unfavorable development to increases in the ultimate liability for BI, physical damage, and collision claims over

what was originally estimated. The increases in these losses relate to increased severity over what was originally

recorded and are the result of inflationary trends in health care costs, auto parts, and body shop labor costs.

Statutory Accounting Principles

The Company’s results are reported in accordance with GAAP, which differ in some respects from amounts

reported under SAP prescribed by insurance regulatory authorities. Some of the significant differences under

GAAP are described below:

• Policy acquisition costs such as commissions, premium taxes, and other costs that vary with and are

primarily related to the acquisition of new and renewal insurance contracts, are capitalized and

amortized on a pro rata basis over the period in which the related premiums are earned, rather than

expensed as incurred, as required by SAP.

• Certain assets are included in the consolidated balance sheets whereas, under SAP, such assets

are designated as “nonadmitted assets,” and charged directly against statutory surplus. These assets

consist primarily of premium receivables outstanding more than 90 days, deferred tax assets that do not

meet statutory requirements for recognition, furniture, equipment, leasehold improvements, capitalized

software, and prepaid expenses.

• Amounts related to ceded reinsurance are shown gross as prepaid reinsurance premiums and

reinsurance recoverables, rather than netted against unearned premium reserves and losses and loss

adjustment expenses reserves, respectively, as required by SAP.

6