JP Morgan Chase 2006 Annual Report Download - page 5

Download and view the complete annual report

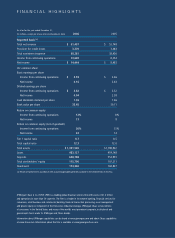

Please find page 5 of the 2006 JP Morgan Chase annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

3

Here are some examples of what we can achieve by

working well together. In all of these cases, the manage-

ment team came together – to review facts and critically

analyze and reanalyze issues – in order to find the right

answers for our clients and our company. We developed

and executed a game plan without the destructive poli-

tics, silly game-playing and selfish arguments about rev-

enue-sharing that can destroy healthy collaboration and

undermine progress.

Establishing the Corporate Bank

Previously, our investment bankers played the lead role

in managing our firm’s relationships with large clients,

even when a client might require non-investment-bank-

ing products and services, such as cash management,

custody, asset management, certain credit and derivatives

products, and others. The product salespeople outside

our Investment Bank operated somewhat independently

from the investment bankers. As a result, we were not

managing our relationships with many of our largest

clients in an integrated and coordinated way. Too many

people were selling their own products without feeling

accountable for JPMorgan Chase’s overall relationship

with the client.

Now, we have addressed this issue with dedicated

corporate bankers who cover the treasurer’s offices of our

largest, longest-standing and most important clients.

These corporate bankers, in partnership with our invest-

ment bankers, are focused on developing our entire rela-

tionship with our clients – orchestrating the coverage

effort with regular account planning, client reviews and

coordinated calling. This effort ultimately should add

hundreds of millions of dollars to revenue and create

happier clients.

Building the mortgage business – in Home Lending and

the Investment Bank

Home Lending is one of the largest originators and ser-

vicers of mortgages in the United States. Separately, our

Investment Bank has been working hard to build out its

mortgage capabilities as the mortgage business overall

has been undergoing fundamental change, i.e., mort-

gages are increasingly being packaged and sold to institu-

tional investors rather than being held by the company

that originates them.

Historically, our two businesses, Home Lending and

the Investment Bank, barely worked together. In 2004,

almost no Home Lending mortgages were sold through

our Investment Bank. This past year, however, our

Investment Bank sold 95% of the non-agency mortgages

(approximately $25 billion worth) originated by Home

Lending. As a result, Home Lending materially increased

its product breadth and volume because it could distrib-

ute and price more competitively. This arrangement

obviously helped our sales efforts, and the Investment

Bank was able to build a better business with a clear,

competitive advantage. In 2006, our Investment Bank

moved up several places in the league-table rankings for

mortgages. (Importantly, Home Lending maintained its

high underwriting standards; more on this later.) We

believe that we now have the opportunity to become one

of America’s best mortgage companies.

Growing credit card sales through retail branches

In 2006, we opened more than one million credit card

accounts through our retail branches, up 74% over

2005. Retail and Card Services teams drove this progress

by working together and analyzing every facet of the

business, including product design, marketing, credit

reporting, systems and staffing. It started slowly, but as

we’ve learned together and innovated, we’ve been able to

add increasingly more profitable new accounts. We have

the ability to provide – almost instantaneously – preap-

proved credit to customers while they are opening other

banking accounts with us. And, while respecting cus-

tomer privacy, we now can offer better pricing because

we can underwrite using both credit card and retail

customer information. Over time, this competitive

advantage will enable us to add more value and produce

better results for customers and for JPMorgan Chase.