JP Morgan Chase 2005 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 2005 JP Morgan Chase annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

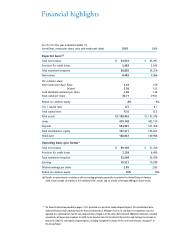

9

Equally important, we materially increased investment

in areas that will drive future growth. Specifics include:

spending hundreds of millions of dollars to open new

branches (this will drive growth in and beyond);

adding more retail loan officers; hiring additional private

bankers; funding the build-out of our energy and mortgage

trading capabilities in the Investment Bank; and investing

in state-of-the-art “blink” credit card technology (which

enables customers to use credit cards for small payments

without having to sign anything). Now being piloted in

six cities, blink is an investment that has put us at the fore-

front of changes in payment systems and card innovation.

In addition to making across-the-board investments to

build our businesses, we are making investments in our

infrastructure that anticipate growth and prepare us to

successfully manage it for years to come. In , we

invested over $billion in platform conversions, including

those for Texas and Card Services.

By consolidating and improving platforms, we are elimi-

nating the inefficiencies and competitive disadvantages

associated with multiple operating platforms. In the process,

we will create best-in-class platforms in many areas, such as

global cash clearing, credit card, retail branches and some of

our trading business. We believe that long-term success is

not possible without great systems and operations. They will

drive efficiency, innovation and speed to market. Much of

this will be accomplished by the end of .

III. Are we properly managing our risks?

Almost all of our businesses are risk-taking businesses –

and we spend a great deal of time thinking about all

aspects and types of risk inherent in them, including:

•Consumer and wholesale credit risk

•Market and trading risk

•Interest rate and liquidity risk

•Reputation and legal risk

•Operational and catastrophic risk

The notable fact about the first three risk areas is that they

are cyclical, and all of them have elements of unpredictabil-

ity. This requires us to be prepared for inevitable cycles. A

company that properly manages itself in bad times is often

the winner. For us, sustaining our strength is a strategic

imperative. If we are strong during tough times – when

others are weak – then the opportunities can be limitless.

Protecting the company is paramount. I will highlight the

types of risks we focus on to give you a sense of the threat

they pose and how we plan for it.

Consumer and wholesale credit risk

Over the years, our company has substantially reduced its

wholesale credit exposure by using a disciplined process for

extending credit and maximizing return on shareholder

capital. In the consumer market, we have controlled our

risk by limiting the amount of low-prime and sub-prime

credit we issue in our card and other consumer businesses.

In addition, we have decided, at the expense of losing some

volume, not to offer higher-risk, less-tested loan products,

such as negatively amortizing Option ARMs.

While we are taking the right steps, we estimate that in

arecession, consumer and wholesale credit costs could

possibly get worse by more than $billion. This daunting

reality requires us to be prepared and well protected.

Protection #is having larger and more durable profits to

absorb the losses. We are accomplishing this by increasing

our margins virtually across the board. Protection #is

maintaining a fortress balance sheet. We try to understand

and manage every asset and every liability and make sure

that someone is accountable for each one. It also means

maintaining, as much as possible, strong loan loss reserves.

Finally,having a well-capitalized firm is critical. With

Tier capital at .%and total capital at %, we believe we

are there. The important point is that we need to manage

the business, the balance sheet and the investments to earn

adequate returns through the cycles and to be prepared for

surprises. We do not want to realize high returns at the top,

only to give them all back at the worst part of the cycle.