Ingram Micro 2008 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2008 Ingram Micro annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

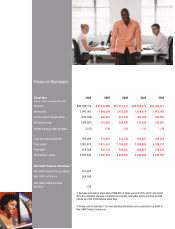

services. We will continue to evolve our business model to meet the changing requirements of our customers (both

suppliers and resellers).

Company Strengths

Despite the global economic downturn that is dampening demand in each of the company’s regions, we believe

that the current technology industry generally favors large, financially-sound distributors that have broad product

portfolios, economies of scale, strong business partner relationships and wide geographic reach. Two-tier distri-

bution continues to be an integral element of the go-to-market strategy for IT suppliers bringing products to market,

particularly in an environment in which suppliers are compelled to streamline processes and eliminate costs. We

deliver value to our partners by making reseller customers more valuable to their end-user customers and making

suppliers more profitable. As such, our strengths position us well to meet the needs of our reseller and vendor

partners worldwide in the current environment and create a firm foundation for future growth as the economy

recovers. Our solid financial position helps us to better manage the challenges presented by economic instability

and volatility. We have identified several catalysts for growth in our IT distribution businessand in new markets. We

believe that the following strengths enable us to further enhance our leadership position in the IT distribution

industry and in adjacent technology product categories.

•Strong Working Capital Management and a Solid Financial Position. We have consistently demon-

strated strong working capital management regardless of economic conditions. In particular, we have

maintained a strong focus on optimizing our investment in inventory, while preserving customer fill rates

and service levels. We have maintained our inventory days on hand at a stable range for the last seven years

as a result of our focused and sustainable initiatives towards minimizing excess and obsolete goods while

improving our purchasing processes and product flow. Furthermore, we continue to manage our accounts

receivable through timely collections, credit limit setting, customer terms and process efficiencies to

minimize our working capital requirements. Our conservative stance on capital management, as well as our

diversified portfolio of capital resources, improves our position in the tighter credit markets. Our financial

strength enables us to provide valuable credit to our customers, employing a disciplined approach to account

management and credit worthiness. We also believe that we are well-positioned to support our growth

initiatives in our IT distribution business and invest in incremental profitable growth opportunities. Finally,

we believe our solid financial position provides us with a competitive advantage as a reliable, long-term

business partner for our supplier and reseller partners.

•Continuous Focus on Optimizing Productivity. We continue to seek ways to improve our processes and

streamline our business model, while refining our cost structure to respond to changes in market demand.

During 2008, we streamlined our European operations and made targeted headcount reductions in

North America, EMEA and Asia-Pacific. We continue to incorporate cost-savings measures in all business

processes. We leverage our IT systems and warehouse locations to support custom shipment requirements,

and by optimizing delivery methodologies, we deliver faster, while reducing shipping costs. We remain

focused on ensuring that our catalog includes the products most desired by our customers, optimizing

inventory management, realizing higher margin opportunities, and developing merchandising and pricing

strategies that produce enhanced business results. In order to fully leverage our global operation, we make

continuous investments in our IT infrastructure and streamline and standardize business processes to drive

efficiency and provide best-in-class quality in our processes and systems throughout the world.

•Business Diversification. Our ability to execute on new initiatives and adapt to new business models

provides a competitive advantage by allowing us to overcome the risks, volatility and demand fluctuations in

a single market, vendor or product segment.

•Products. Based on publicly available information, we believe we offer the largest breadth of products

in the IT industry. Our broad base of products allows us to better serve our customers, as well as mitigate

risk. Our broad line card, or catalog of product offerings, makes us less vulnerable to market dynamics or

actions by any one vendor or segment, or volatility in market demand in specific product lines. We

continuously focus on refreshing our business with new, high-potential products and services. We are

focused on moving deeper into new adjacent product categories and globalizing our efforts. Recent

2