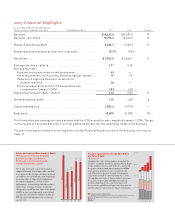

Eli Lilly 2007 Annual Report Download - page 6

Download and view the complete annual report

Please find page 6 of the 2007 Eli Lilly annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

4

the Humalog insulin family—was a key goal. Lilly made

progress against that goal in 2007, though we are not yet

satised. Humalog is gaining share again in some mar-

kets, driving 20 percent growth outside the U.S. for 2007

as a whole and 32 percent in the fourth quarter. In the

U.S., our total Humalog prescription volume grew in 2007

for the rst time in four years, and we aim to sustain that

trend along with gaining new-prescription market share.

Our summary of Lilly’s progress in 2007 would not

be complete without attention to the remarkable contribu-

tions of our Elanco Animal Health business unit. Elanco’s

worldwide sales reached nearly $1 billion in 2007, an in-

crease of 14 percent. The acquisition in 2007 of Ivy Animal

Health and the ongoing launches of products for compan-

ion animals—six are planned within four years—position

Elanco for continued signicant growth in the years ahead.

Pipeline Progress

The long-term health of any pharmaceutical company

is determined by its R&D pipeline—the promise of future

breakthroughs. By that measure, we believe that the

outlook for Lilly is robust. In 2007, Lilly brought 16 new

molecular entities (NMEs) into human trials—a record

unparalleled in our history. We increased our portfolio

of new molecules being tested on patients by nearly 50

percent, to 44, and in 2008 we are poised to add another

15 clinical candidates.

A highlight of our late-stage development in 2007

was the submission of prasugrel to the FDA for approval

at year’s end, after an all-out effort by Lilly’s medical and

regulatory affairs teams. Prasugrel (the proposed trade-

mark is Efent™) is a potential new treatment for patients

with acute coronary syndrome (ACS) who are undergoing

angioplasty.

In addition to prasugrel, Lilly has seven other NMEs

or NME-like therapies in Phase III trials or pending

regulatory approval, including potential new treatments

for osteoporosis, diabetes, multiple sclerosis, and non-

Hodgkin’s lymphoma, an inhaled version of insulin, a

weekly formulation of Byetta, and a long-acting injectable

form of Zyprexa. Lilly also has more than a dozen new

indications, line extensions, and delivery devices in Phase

III trials or under regulatory review.

If successful, most of those therapies will be approved

between 2008 and 2011, further strengthening Lilly’s prod-

uct portfolio as older patents expire. At the same time, Lilly

has the strongest mid-stage pipeline of molecules in its his-

tory, and we are accelerating the development of some of

them in a concerted strategy. As a result, Lilly should have

at least 10 NMEs in Phase III trials by 2011—with the goal

of launching two novel medicines per year starting at that

time, increasing to three per year in 2014.

Business Development

On the basis of increasing cash ow, Lilly invested

nearly $3 billion in acquisitions and licensing during

2007 to strengthen our sales performance and our R&D

pipeline. Most prominently, our successful integration

of ICOS’s operations allowed us to realize considerable

efciencies in the selling and marketing of Cialis—which

posted a 25 percent increase in worldwide sales in 2007,

to $1.216 billion.

Lilly’s acquisition of Hypnion in 2007 gave us access

to a promising new compound for sleep disorders as well

as a broader presence in this area of research. In addition,

we entered into licensing agreements with OSI Phar-

maceuticals and MacroGenics to gain access to exciting

compounds and research platforms focused on diabetes

and various autoimmune diseases, with Glenmark Phar-

maceuticals to obtain the rights to a portfolio of potential

pain-ghting compounds, and with BioMS Medical on a

potential therapy for multiple sclerosis.

Growing cash ow also allowed us to increase our

quarterly dividend in the fourth quarter of 2007 by

almost 11 percent, and it will give us continued freedom

to seek growth opportunities and improved pipeline value

through acquisitions and licensing in the years ahead.

Transformation

Earlier, we referred to Lilly’s vision of becoming a

truly patient-centered enterprise, focused on optimiz-

ing individual patient outcomes. While we realize that

the achievement of this vision will take many years, we

were pleased that 2007 brought early, tangible evidence

of Lilly’s transformation into a company that offers an

unmistakable value proposition to the people who depend

on its products.

For example, the effort to “tailor” our medicines to

individual patients’ needs—delivering the right drug at

the right dose at the right time—is bearing fruit. This will

lead to a clearer benet/risk understanding for patients,

doctors, and payers alike—based on a higher degree of

condence that a medicine will work effectively and with

manageable side effects.

Lilly’s large clinical trial of prasugrel is a great ex-

ample. Completed in 2007, the so-called TRITON study

yielded robust data on patients for whom the benets of

prasugrel clearly outweigh the risks; patients who ben-

eted from the drug but who also had increased risk of

bleeding (and might therefore be best served by a lower

dose); and the small percentage of patients who did not

appear to gain greater benet from prasugrel compared to

the potential risk.

Lilly also has made considerable progress in trans-

forming itself from a fully-integrated pharmaceutical com-

pany—the old “FIPCO” model—into what we refer to as

a fully-integrated pharmaceutical network—or “FIPNET.”

In the new model, we draw on a broad range of resources

outside our company’s walls—to increase our effective

capacity and access to external capabilities, to reduce our

level of risk and accelerate development, and ultimately to

help lower our average cost of R&D per molecule.