Comfort Inn 2002 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2002 Comfort Inn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

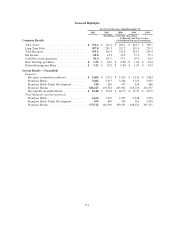

Liquidity and Capital Resources

Net cash provided by operating activities was $99.0 million for the year ended December 31, 2002,

representing a slight decrease of $2.7 million from $101.7 million for the year ended December 31, 2001. The

decrease in cash provided by operating activities was primarily due to lower repayments related to marketing and

reservation activities offset by improved management of working capital. As of December 31, 2002, the total

long-term debt outstanding for the Company was $307.8 million, $23.8 million of which matures in the next

twelve months.

During each of the past three years, the Company has realigned its corporate structure to increase its

strategic focus on delivering value-added services and support to franchisees, including centralizing the

Company’s franchise service and sales operations, consolidating its brand management functions and realigning

its call center operations. The Company recorded a $1.6 million restructuring charge in 2002 of which

approximately $0.4 million was paid in 2002. The restructuring charges represented employee severance and

termination benefits. The restructuring was initiated and completed in 2002 and the Company expects the

remaining liability to be paid during 2003. The Company paid $3.1 million related to the 2001 restructuring

liability during the year ended December 31, 2002, and expects the remaining $0.6 million liability to be

substantially paid in 2003. The Company paid $0.2 million related to the 2000 restructuring liability for the year

ended December 31, 2002, which completed the restructuring.

The Company received net cash repayments related to marketing and reservation activities totaling

$17.2 million and $20.3 million during the years ended December 31, 2002 and 2001, respectively. The 2002 and

2001 net repayments are associated with cost reductions from restructured operations, growth in fees from

normal operations and increases in property and yield management fees. The Company expects marketing and

reservation activities to generate positive cash flows between $16.0 million and $19.0 million in 2003.

Cash (utilized in) provided by investing activities for the years ended December 31, 2002, 2001 and 2000,

was ($14.7 million), $87.7 million and ($16.6 million), respectively. During the years ended December 31, 2002,

2001 and 2000, capital expenditures totaled $12.2 million, $13.5 million and $16.6 million, respectively. Capital

expenditures include the installation of system-wide property and yield management systems, upgrades to

financial and reservation systems, computer hardware and renovations to the Company’s corporate headquarters

(including a franchisee learning and training center). During 2001, the Company received a cash payment of

$101.9 million from Sunburst related to a note receivable due to the Company.

On September 1, 2000, the Company monetized $16.3 million in principal and interest of the $115 million

principal, five-year Subordinated Term Note (the “Old Note”) to Sunburst issued in October 1997. The Company

received three MainStay Suites properties through the monetization transaction. In connection with an

amendment of the strategic alliance agreement between the Company and Sunburst, effective October 15, 2000,

interest payable on the Old Note accrued at a rate of 11% per annum compounded daily. The Company

implemented this amendment prospectively beginning on January 1, 1999, and recognized interest on the

outstanding principal and accrued interest amounts at an effective rate of 10.58%. Total interest accrued at

December 31, 2000 was $42.2 million. On January 5, 2001, the Company received $101.9 million, a parcel of

land valued at approximately $1.5 million and a $35 million seven-year senior subordinated note bearing interest

at 11 3/8% (the “New Note”) in settlement of the balance of the Old Note. In 2000, the Company recognized a

pre-tax loss of $3.5 million resulting from this transaction. The New Note accrued interest up until June 2002, at

which point interest became payable semi-annually in arrears. As of December 31, 2002, the Company’s balance

sheet includes an interest receivable from Sunburst of $2.3 million which is included in other current assets in the

accompanying consolidated balance sheets and was paid to the Company by Sunburst in January 2003.

Financing cash flows relate primarily to the Company’s borrowings under its credit lines and treasury stock

purchases. In June 2001, the Company entered into a five-year $265 million competitive advance and multi-

currency credit facility. The credit facility provides for a term loan of $115 million and a revolving credit facility

F-10