Cogeco 2006 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2006 Cogeco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

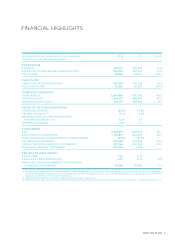

Management’s Discussion and Analysis COGECO CABLE INC. 2006 11

FREE CASH FLOW

Free cash fl ow is defi ned as cash fl ow from operations less capital expenditures (including assets acquired under capital

lease that are disclosed in Note 15 b) on page 59 which are not refl ected in the consolidated statements of cash fl ow) and

increase in deferred charges. The fi nancial community also closely follows this indicator since it measures the business’

ability to repay debt, distribute capital to its shareholders and fi nance its growth.

RGU GROWTH AND PENETRATION OF SERVICE OFFERINGS

RGU expansion is a critical driver of revenue growth and measures the success of the marketing strategy and the

competitiveness of the service offering and pricing. Penetration statistics measure Cogeco Cable’s market share.

Cogeco Cable computes the penetration for basic services as a percentage of homes passed and, in the case of all other

services, as a percentage of basic customers in the cable systems where the service is offered.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

The preparation of fi nancial statements in accordance with Canadian GAAP requires management to adopt accounting

policies and to make estimates and assumptions that affect the reported amounts of assets and liabilities, contingent

assets and liabilities, and revenue and expenses during the reporting year. A summary of the Corporation’s signifi cant

accounting policies is presented in Note 1 on page 42 of the consolidated fi nancial statements. The following accounting

policies were identifi ed as critical to Cogeco Cable’s business operations:

REVENUE RECOGNITION

The Corporation considers revenue to be earned as services are rendered, provided that ultimately collection is reasonably

assured. The Corporation earns revenue from several sources. Revenue recognition from the main sources is as follows:

• Monthly fees from cable television and related services, from HSI services and from Telephony services are recognized

when services are provided.

• Since management considers the sale of home terminal devices as a single unit of accounting of a multiple element

arrangement, equipment revenue is recorded upon activation of the service.

• Installation revenue is deferred and amortized over the average life of a customer’s subscription, which is four years.

Management considers that installation revenue is part of a multiple element arrangement and has no standalone value.

Accordingly, installation revenue is deferred and amortized at the same pace as cable television, HSI services and Digital

Telephony monthly fees are earned.

• Promotional offers are accounted for as a deduction of revenue when customers are taking advantage of such offer.

ALLOWANCE FOR DOUBTFUL ACCOUNTS

A large proportion of the Corporation’s revenue is earned from individual customers. Accordingly, allowance for doubtful

accounts is calculated by examining such factors as the number of overdue days of the customer’s balance owing as well

as the customer’s collection history with Cogeco Cable. As a result, conditions causing fl uctuations in the aging of customer

accounts will directly impact the reported amount of bad debt expenses.

CAPITALIZATION OF DIRECT LABOUR AND OVERHEAD

As outlined in the recommendations of the Canadian Institute of Chartered Accountants (CICA) with respect to property,

plant and equipment, capitalization of costs includes the expenditures to acquire, construct, develop or improve an item

of property, plant or equipment, and includes all costs directly attributable to those activities. The cost of an item includes

direct construction or software development costs, such as materials and labour, and overhead costs directly attributable

to the construction or software development activity. The cost to enhance the service potential of an item is considered an

improvement and as a result is capitalized. Costs incurred in the maintenance of service potential are expensed.

Cogeco Cable capitalizes direct labour and direct overhead costs incurred to construct new assets, enhance existing assets

and connect new customers. Although capitalization of fi nancial expense is permitted for construction activities, it is the

Corporation’s policy not to capitalize them.