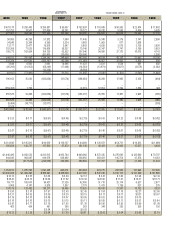

Chesapeake Energy 2005 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2005 Chesapeake Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

|

|

to our investors. I often believe that many investors do not fully

appreciate how much risk there is in this industry and how well we

manage it at Chesapeake. For example, in 2006 when natural gas

prices are widely expected to decline to below $6 per mmbtu by late

summer because of this past winter’s record warmth, we have hedged

71% of our 2006 natural gas production at $9.43 per mmbtu, 36%

of our 2007 natural gas production at $9.85 per mmbtu and 22% of

our 2008 natural gas production at $9.10 per mmbtu (excluding

CNR hedges).

Additionally, we are the only E&P company that has significantly

hedged its exposure to rising service costs by building drilling rigs

and investing in related service industry providers. To date, these

investments have appreciated in value by roughly $250 million. We

now own 32 rigs outright and have an additional 25 on order, which

should account for approximately 60% of the rigs we plan to operate

a year from now. Rig ownership is proving to be an extremely valuable

competitive advantage in both acquisitions and in operations.

Moreover, in a time of increasing geopolitical unrest around the

world, the prospect of asset loss in many areas of the world to arbitrary

tax and royalty changes or even outright contract cancellation by

foreign governments is a serious concern faced by all major integrated

oil companies and many large independent E&P companies. Except

for occasional chatter about a windfall profits tax in the U.S.,

Chesapeake’s assets are safe from such political risks.

I also emphasize that Chesapeake’s assets are all high and dry

onshore in the U.S. In a time of what appears to be a cycle of greater

hurricane activity in the Gulf of Mexico, many investors may not fully

appreciate the very high risks that Gulf of Mexico operators and

investors may face in hurricane seasons to come.

Not having access to rigs to develop our assets or owning assets

subject to confiscation by some foreign potentate or suffering damage

from hurricanes are risks to which we have no exposure. That is why,

dollar for dollar, we believe investors can achieve the very best risk-

adjusted returns in the industry right here at CHK.

OPPORTUNITY Now let’s talk about opportunity. Much

earlier than most companies, in fact as far back as 1998 and 1999,

Chesapeake’s management team anticipated changing industry

conditions and quickly recognized the trends that have driven

remarkable increases in oil and natural gas prices during the past

eight years. We also recognized the need to develop the building

blocks of future value creation in the E&P business – people, land

and science.

During the past eight years we have aggressively captured

opportunities in each of these critical areas. For example, before

talented people became scarce in this industry, we were hiring them

by the hundreds. Before prospects and leases became scarce, we

built a system of prospect generation and leasehold acquisition that

is second to none in the industry. And finally, when others were

reluctant to invest in science and new ideas, we aggressively entered

into virtually every major natural gas resource play in the U.S. east

of the Rockies.

Chesapeake has significantly strengthened its technical capabilities

during the past eight years by dramatically increasing its land,

geoscience and engineering staff to more than 600 employees. In

“Additionally, we are the

only E&P company that

has significantly hedged

its exposure to rising

service costs by building

drilling rigs and investing

in related service indus-

try providers. To date,

these investments have

appreciated in value by

roughly $250 million.”

8 CHK 2005 ANNUAL REPORT