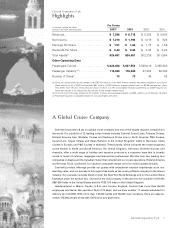

Carnival Cruises 2003 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2003 Carnival Cruises annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

|

|

10 Carnival Corporation & plc

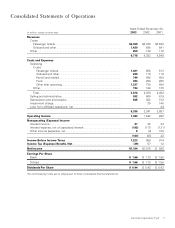

Preparation of Financial Statements

The preparation of our consolidated financial state-

ments in accordance with accounting principles gener-

ally accepted in the United States of America requires

us to make estimates and assumptions that affect the

amounts reported and disclosed in our financial state-

ments. Actual results could differ from these estimates.

All material intercompany accounts, transactions and

unrealized profits and losses on transactions within

our consolidated group and with affiliates are elimi-

nated in consolidation.

Commencing in 2003, we changed the reporting

format of our consolidated statements of operations

to present our significant revenue sources and their

directly related variable costs and expenses. In addition,

we have separately identified certain ship operating

expenses, such as payroll and related expenses and

food costs. All prior periods were reclassified to con-

form to the current year presentation.

Note 2—Summary of Significant Accounting Policies

Basis of Presentation

We consolidate entities over which we have control,

as typically evidenced by a direct ownership interest of

greater than 50%. For affiliates where significant influ-

ence over financial and operating policies exists, as typ-

ically evidenced by a direct ownership interest from 20%

to 50%, the investment is accounted for using the equity

method. See Note 6.

Cash and Cash Equivalents and Short-Term

Investments

Cash and cash equivalents include investments with

original maturities of three months or less, which are

stated at cost. At November 30, 2003 and 2002, cash

and cash equivalents included $937 million and $616

million of investments, respectively, primarily comprised

of strong investment grade asset-backed debt obliga-

tions, commercial paper and money market funds.

Short-term investments are comprised of marketable

debt and equity securities which are categorized as

available for sale and, accordingly, are stated at their

fair values. Unrealized gains and losses are included

as a component of accumulated other comprehensive

income (“AOCI”) within shareholders’ equity until real-

ized. The specific identification method is used to

determine realized gains or losses.

Inventories

Inventories consist primarily of provisions, gift shop

and art merchandise held for resale, spare parts, sup-

plies and fuel carried at the lower of cost or market.

Cost is determined using the weighted-average or first-

in, first-out methods.

Property and Equipment

Property and equipment are stated at cost. Deprecia-

tion and amortization were computed using the straight-

line method over our estimates of average useful lives

and residual values, as a percentage of original cost,

as follows:

Residual

Values Years

Ships . . . . . . . . . . . . . . . . . . . . . 15% 30

Buildings and improvements . . . . 0–10% 5–40

Transportation equipment

and other . . . . . . . . . . . . . . . . 0–25% 2–20

Leasehold improvements,

including port facilities. . . . . . . Shorter of lease

term or related

asset life

We review our long-lived assets for impairment

whenever events or changes in circumstances indicate

that the carrying amount of these assets may not be

fully recoverable. The assessment of possible impair-

ment is based on our ability to recover the carrying

value of our asset based on our estimate of its undis-

counted future cash flows. If these estimated undis-

counted future cash flows are less than the carrying

value of the asset, an impairment charge is recognized

for the excess, if any, of the assets carrying value over

its estimated fair value (see Note 5).

Dry-dock costs are included in prepaid expenses and

are amortized to other ship operating expenses using

the straight-line method generally over one year.

Ship improvement costs that we believe add value to

our ships are capitalized to the ships, and depreciated

over the improvements’ estimated useful lives, while

costs of repairs and maintenance are charged to expense

as incurred. We capitalize interest on ships and other

capital projects during their construction period. Upon

the replacement or refurbishment of previously capital-

ized ship components, these assets’ estimated cost

and accumulated depreciation are written-off and any

resulting loss is recognized in our results of operations.

No such material losses were recognized in fiscal 2003,

2002 or 2001. See Note 4.

Goodwill

Statement of Financial Accounting Standards (“SFAS”)

No. 142, “Goodwill and Other Intangible Assets” requires

companies to stop amortizing goodwill and requires an

annual, or when events or circumstances dictate, a more

frequent, impairment review of goodwill. Accordingly,

upon adoption of SFAS No. 142 on December 1, 2001,

we ceased amortizing our goodwill, all of which had

been allocated to our cruise reporting units. In April

2003, we recorded $2.25 billion of additional goodwill

Notes to Consolidated Financial Statements (continued)