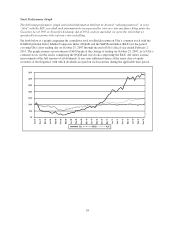

Ulta 2012 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2012 Ulta annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

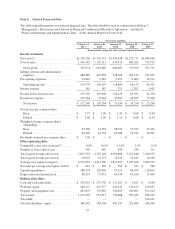

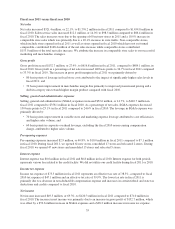

2012, compared to $128.6 million and $97.1 million in fiscal 2011 and 2010, respectively. Capital expenditures

increased in fiscal 2012 compared to fiscal 2011 due to the increase in our 2012 new store program. During fiscal

2012 we opened 102 new stores, remodeled 21 stores and relocated 3 stores, compared to 61 new stores,

17 remodels and 2 relocations during fiscal 2011 and 47 new stores, 13 remodels and 5 relocations during fiscal

2010.

Financing activities

Financing activities in fiscal 2012, 2011 and 2010 consist principally of capital stock transactions and the related

income tax effects and a dividend payment. Common stock repurchased in fiscal 2012 and 2011 represents the

fair value of common shares repurchased from plan participants in connection with shares withheld to satisfy

minimum statutory tax obligations upon the vesting of restricted stock.

We had no borrowings outstanding under our credit facility at the end of fiscal 2012, 2011 and 2010. The zero

outstanding borrowings position is due to a combination of factors including strong sales growth, overall

performance of management initiatives including expense control as well as inventory and other working capital

reductions. We may require borrowings under the facility from time to time in future periods to support our new

store program and seasonal inventory needs.

Dividend

On March 8, 2012, we announced that our Board of Directors had declared a $1.00 per share special cash

dividend to shareholders of record as of the close of business on March 20, 2012. The special cash dividend

totaling $62.5 million was paid on May 15, 2012.

Our Board of Directors may determine future dividends after giving consideration to our levels of profit and cash

flow, capital requirements, current and future liquidity, restrictions included as part of our credit facility as well

as financial and other conditions existing at the time.

Credit facility

On October 19, 2011, the Company entered into an Amended and Restated Loan and Security Agreement (the

Loan Agreement) with Wells Fargo Bank, National Association, as Administrative Agent, Collateral Agent and a

Lender thereunder, Wells Fargo Capital Finance LLC as a Lender, J.P. Morgan Securities LLC as a Lender,

JP Morgan Chase Bank, N.A. as a Lender and PNC Bank, National Association, as a Lender. The Loan

Agreement amended and restated the Loan and Security Agreement, dated as of August 31, 2010, by and among

the lenders. The Loan Agreement extends the maturity of the Company’s credit facility to October 2016,

provides maximum revolving loans equal to the lesser of $200,000 or a percentage of eligible owned inventory,

contains a $10,000 subfacility for letters of credit and allows the Company to increase the revolving facility by

an additional $50,000, subject to consent by each lender and other conditions. The Loan Agreement contains a

requirement to maintain a minimum amount of excess borrowing availability at all times. Substantially all of the

Company’s assets are pledged as collateral for outstanding borrowings under the facility. Outstanding

borrowings will bear interest at the prime rate or Libor plus 1.50% and the unused line fee is 0.225%.

On September 5, 2012, we entered into Amendment No. 1 to the Amended and Restated Loan and Security

Agreement (the Amendment) with the lender group. The Amendment updated certain administrative terms and

conditions and provides us greater flexibility to take certain corporate actions. There were no changes to the

revolving loan amounts available, interest rates, covenants or maturity date under terms of the Loan Agreement.

As of February 2, 2013 and January 28, 2012, the Company had no borrowings outstanding under its credit

facility and the Company was in compliance with all terms and covenants of the agreement.

Seasonality

Our business is subject to seasonal fluctuation. Significant portions of our net sales and profits are realized during

the fourth quarter of the fiscal year due to the holiday selling season. To a lesser extent, our business is also

affected by Mothers’ Day as well as the “Back to School” season and Valentine’s Day. Any decrease in sales

37