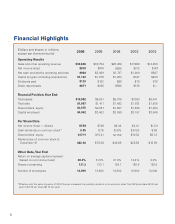

Sunoco 2006 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2006 Sunoco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

from cokemaking operations and higher gains from litigation settlements. Partially off-

setting these positive factors were higher business development and other expenses.

Sunoco received a total of $309 million in exchange for interests in its Jewell cokemaking

operations in two separate transactions in 1995 and 2000. Sunoco also received a total of

$415 million in exchange for interests in its Indiana Harbor cokemaking operations in two

separate transactions in 1998 and 2002. Sunoco did not recognize any gain as of the dates

of these transactions because the third-party investors were entitled to a preferential return

on their respective investments.

In December 2006, Sunoco acquired the limited partnership interest of the third-party

investor in the Jewell cokemaking operation for $155 million and recognized a $3 million

after-tax loss in connection with this transaction. This loss is included in Net Financing

Expenses and Other under Corporate and Other in the Earnings Profile of Sunoco

Businesses.

The preferential returns of the investors in the Indiana Harbor cokemaking operations are

currently equal to 98 percent of the cash flows and tax benefits from such cokemaking

operations during the preferential return period, which continues until the investor enti-

tled to the preferential return recovers its investment and achieves a cumulative annual

after-tax return of approximately 10 percent. The preferential return period for the Indiana

Harbor operations is projected to end during 2007. The accuracy of this estimate is some-

what uncertain as the length of the preferential return period is dependent upon estimated

future cash flows as well as projected tax benefits which could be impacted by their poten-

tial phase-out (see below). Higher-than-expected cash flows and tax benefits will shorten

the investor’s preferential return period, while lower-than-expected cash flows and tax

benefits will lengthen the period. After payment of the preferential return, the investors in

the Indiana Harbor operations will be entitled to a minority interest in the related cash

flows and tax benefits initially amounting to 34 percent and thereafter declining to 10 per-

cent by 2038.

Expense is recognized to reflect the investors’ preferential returns in the Jewell and Indiana

Harbor operations. Such expense, which is included in Net Financing Expenses and Other

under Corporate and Other in the Earnings Profile of Sunoco Businesses, totaled $31, $27

and $31 million after tax in 2006, 2005 and 2004, respectively. The 2006 amount includes

$9 million after tax attributable to the third-party investor’s preferential return in the

Jewell cokemaking operation. As a result of Sunoco’s acquisition of the investor’s interest

in this operation, such investor is no longer entitled to any preferential or residual return.

Income is recognized by the Coke business as coke production and sales generate cash

flows and tax benefits, which are allocated to Sunoco and the third-party investors. The

Coke business’ after-tax income attributable to the tax benefits, which primarily consist of

nonconventional fuel credits, was $38, $38 and $35 million after tax in 2006, 2005 and

2004, respectively.

Under existing tax law, most of the coke production at Jewell and all of the coke pro-

duction at Indiana Harbor are not eligible to generate nonconventional fuel tax credits

after 2007. In addition, prior to the expiration dates for such credits, they would be phased

out, on a ratable basis, if the average annual price of domestic crude oil at the wellhead is

within a certain inflation-adjusted price range. (This range was $53.20 to $66.79 per barrel

for 2005, the latest year for which the range is available.) The domestic wellhead price

averaged $60.03 per barrel for the eleven months ended November 30, 2006. The corre-

sponding price for West Texas Intermediate (“WTI”) crude oil, a widely published refer-

ence price for domestic crude oil, was $66.59 per barrel for the eleven months ended

November 30, 2006. Based on the Company’s estimate of the domestic wellhead price for

the full-year 2006, Coke recorded only 65 percent of the benefit of the tax credits that

otherwise would have been available without regard to these phase-out provisions. The

16