Snapple 2014 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2014 Snapple annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

5

Integrated business model. Our integrated business model provides opportunities for net sales and profit growth through the

alignment of the economic interests of our brand ownership and our manufacturing and distribution businesses. For example, we

can focus on maximizing profitability for our company as a whole rather than focusing on profitability generated from either the

sale of beverage concentrates or the bottling and distribution of our products. Additionally, our integrated business model enables

us to be more flexible and responsive to the changing needs of our large retail customers by coordinating sales, service, distribution,

promotions and product launches and allows us to more fully leverage our scale and reduce costs by creating greater geographic

manufacturing and distribution coverage. Our manufacturing and distribution system in the U.S. also enables us to improve focus

on our brands, especially certain brands such as 7UP, Sunkist soda, A&W, Squirt, RC Cola, Hawaiian Punch and Snapple, which

do not have a large presence in the bottler systems affiliated with The Coca-Cola Company ("Coca-Cola") or PepsiCo, Inc.

("PepsiCo").

Strong customer relationships. Our brands have enjoyed long-standing relationships with many of our top customers. We

sell our products to a wide range of customers, from bottlers and distributors to national retailers, large food service and convenience

store customers. We have strong relationships with some of the largest bottlers and distributors, including those affiliated with

Coca-Cola and PepsiCo, some of the largest and most important retailers, including Wal-Mart Stores, Inc. ("WalMart"), The Kroger

Co., SUPERVALU, Inc., Safeway Inc., Publix Super Markets, Inc. and Target Corporation, some of the largest food service

customers, including McDonald's Corporation, Yum! Brands, Inc., Burger King Corp., Sonic Corp., The Wendy's Company,

Subway Restaurants, Jack in the Box, Inc., Chick-fil-A, Inc., Whataburger Restaurants LLC and Arby's Group, Inc., and

convenience store customers, including 7-Eleven, Inc., Circle K Enterprises, Inc. and OXXO. Our portfolio of strong brands,

operational scale and experience across beverage segments has enabled us to maintain strong relationships with our customers.

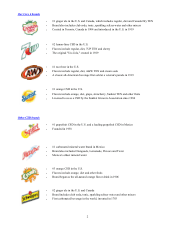

Attractive positioning within a large and profitable market. We hold the #1 position in the U.S. flavored CSD beverage

markets by volume according to Beverage Digest. We are also a leader in the Canada and Mexico beverage markets. Our portfolio

of products is biased toward flavored CSDs, which continue to gain market share versus cola CSDs, but also focuses on emerging

categories such as teas and juices. We believe marketing and product innovations that target fast growing population segments,

such as the Hispanic community in the U.S., could drive market growth.

Broad geographic manufacturing and distribution coverage. As of December 31, 2014, we had 19 manufacturing facilities

and 106 principal distribution centers and warehouse facilities in the U.S., as well as two manufacturing facilities and 12 principal

distribution centers and warehouse facilities in Mexico. These facilities use a variety of manufacturing processes. We have

strategically located manufacturing and distribution capabilities, enabling us to better align our operations with our customers,

reduce transportation costs and have greater control over the timing and coordination of new product launches. In addition, our

warehouses are generally located at or near bottling plants and geographically dispersed to ensure our products are available to

meet consumer demand. We actively manage transportation of our products using our own fleet of approximately 4,500 and 1,500

vehicles in the U.S. and Mexico, respectively, and third party logistics providers on a selected basis.

Strong operating margins and stable cash flows. The breadth of our brand portfolio has enabled us to generate strong operating

margins which have delivered stable cash flows. These cash flows enable us to consider a variety of alternatives, such as investing

in our business, repurchasing shares of our common stock, paying dividends to our stockholders and reducing our debt. As a result

of our stable cash flows and the reduction of our capital expenditures, we have been able to increase our dividends each year in

order to return more cash to our stockholders.

Experienced executive management team. Our executive management team has over 200 years of collective experience in

the food and beverage industry. The team has broad experience in brand ownership, manufacturing and distribution, and enjoys

strong relationships both within the industry and with major customers. In addition, our management team has diverse skills that

support our operating strategies, including driving organic growth through targeted and efficient marketing, improving productivity

of our operations, aligning manufacturing and distribution interests and executing strategic acquisitions.

OUR STRATEGY

The key elements of our business strategy are to:

Build our brands. We have a well-defined portfolio strategy to allocate our marketing and sales resources. We use an on-

going process of market and consumer analysis to identify key brands that we believe have the greatest potential for profitable

sales growth. We continue to invest most heavily in our key brands to drive profitable and sustainable growth by strengthening

consumer awareness, developing innovative products and extending brands to take advantage of evolving consumer trends,

improving distribution and increasing promotional effectiveness. We also focus on new distribution agreements for emerging,

high-growth third party brands in new categories that can use our manufacturing and distribution network. We can provide these

new brands with distribution capability and resources to grow, and they provide us with exposure to growing segments of the

market with relatively low risk and capital investment.