Kia 2001 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2001 Kia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

|

|

Financial Statements & Notes

46 47

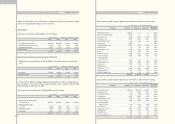

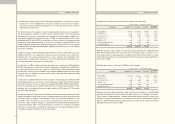

ranty costs incurred are charged against the accrual when paid.

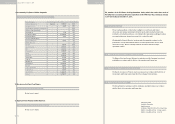

Accrued Severance Benefits

Employees and directors with more than one year of service are entitled to receive a lump-sum payment

upon termination of their service with the Company, based on their length of service and rate of pay at

the time of termination. The accrued severance benefits which would be payable, assuming all eligible

employees were to resign as of December 31, 2001 and 2000 amount to 1,026,529 million ($774,096

thousand) and 914,066 million ($689,289 thousand), respectively.

Accrued severance benefits are approximately 55 percent and 52 percent funded at December 31,

2001 and 2000, respectively, through an individual severance insurance plan. Individual severance

insurance deposits, in which the beneficiary is a respective employee, are presented as deduction from

accrued severance benefits.

Before April 1999, the Company and the employees paid 3 percent and 6 percent, respectively, of

monthly pay (as defined) to the National Pension Fund in accordance with the National Pension Law of

Korea. The Company paid half of the employees' 6 percent portion and is paid back at the termination of

service by offsetting the receivable against the severance payment. Such receivables, totalling 51,078

million ($38,517 thousand) and 55,726 million ($42,022 thousand) as of December 31, 2001 and 2000,

respectively, are presented as a deduction from accrued severance benefits. Since April 1999, accord-

ing to a revision in the National Pension Law, the Company and the employees each pay 4.5 percent of

monthly pay to the Fund.

Stock Options

The Company computes total compensation expense to stock options, which are granted to employees

and directors, by fair value method using the option-pricing model. The compensation expense has

been accounted for as a charge to current operations and a credit to capital adjustment from the grant

date using the straight-line method.

Derivative Instruments

All derivative instruments are accounted for at fair value with the valuation gain or loss recorded as an

asset or liability. If the derivative instrument is not part of a transaction qualifying as a hedge, the adjust-

ment to fair value is reflected in current operations. The accounting for derivative transactions that are

part of a qualified hedge, based both on the purpose of the transaction and on meeting the specified cri-

teria for hedge accounting, differs depending on whether the transaction is a fair value hedge or a cash

flow hedge. Fair value hedge accounting is applied to a derivative instrument designated as hedging the

exposure to changes in the fair value of an asset or a liability or a firm commitment (hedged item) that is

attributable to a particular risk. The gain or loss both on the hedging derivative instruments and on the

hedged item attributable to the hedged risk is reflected in current operations. Cash flow hedge account-

ing is applied to a derivative instrument designated as hedging the exposure to variability in expected

future cash flows of an asset or a liability or a forecasted transaction that is attributable to a particular risk.

The effective portion of gain or loss on a derivative instrument designated as a cash flow hedge is

recorded as a capital adjustment and the ineffective portion is recorded in current operations. The effec-

tive portion of gain or loss recorded as a capital adjustment is reclassified to current earnings in the

same period during which the hedged forecasted transaction affects earnings. If the hedged transaction

results in the acquisition of an asset or the incurrence of a liability, the gain or loss in capital adjustment is

added to or deducted from the asset or the liability.

In 2000, the Company entered into foreign currency forward contracts to hedge the exposure to

changes in the fair value of recognized foreign currency denominated asset and liabilities. The Company

recognized gain and losses arising from changes in the fair value of the foreign currency forward con-

tracts in net income on a current basis, the ineffective portion of which was 2,417 million (1,823 thou-

sand) as of December 31, 2000, with related liabilities of 39,207 million (29,566 thousand) included

in derivative instruments-credit.

In addition, the Company deferred the losses on the effective portion of foreign currency forward con-

tracts for cash flow hedging purpose from forecasted exports as capital adjustments, amounting

26,071 million (19,660 thousand) as of December 31, 2000, all of which were included in the deter-

mination of net income in 2001.

Accounting for Foreign Currency Transactions and Translation

The Company maintains its accounts in Korea won. Transactions in foreign currencies are recorded in

Korean won based on the prevailing rates of exchange on the transaction date. Monetary accounts with

balances denominated in foreign currencies are recorded and reported in the accompanying non-con-

solidated financial statements at the exchange rates prevailing at the balance sheet dates. The balances

have been translated using the Bank of Korea Basic Rate which was 1,326.10 and 1,259.70 to US

$1.00 at December 31, 2001 and 2000, respectively, and the translation loss and gain is reflected in cur-

rent operations

Income Tax Expense

The Company recognizes deferred income taxes. Accordingly, income tax expense is determined by

adding or deducting the total income tax and surtaxes to be paid for the current period and the changes

in deferred income tax debits (credits). The difference between the income tax expense and the amount

of income tax shown in the current period's tax return will be offset against the deferred income tax cred-

its (debits), which will occur in subsequent periods.

Earnings Per Share

Basic ordinary income per common share and basic earnings per common share are computed by

dividing ordinary income (after deduction for tax effect) and net income, respectively, by the weighted

average number of common shares outstanding during the year. The number of shares used in comput-

ing ordinary income per share and earnings per share is 387,672,624 in 2001 and 444,940,373 in 2000.

Diluted ordinary income per share and diluted earnings per share are computed by dividing ordinary

income and net income, after addition for the effect of expenses related to diluted securities on net

income, by the number of the weighted average number of common shares plus the number of dilutive

potential common shares. As the Company has not issued any diluted securities and the stock options

have no dilutive effect on basic ordinary income per share and basic earnings per share in 2001 and

NOTES TO NON-CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2001 AND 2000

NOTES TO NON-CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2001 AND 2000