Kentucky Fried Chicken 2005 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2005 Kentucky Fried Chicken annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

constructionperiodsbeginningJanuary1,2006andthere-

after,whetherpaidorsubjecttoarentholiday,inaccordance

withtheFASBStaffPositionNo.13-1,“AccountingforRental

CostsIncurredduringaConstructionPeriod”(“FSP13-1”).

WedonotanticipatethattheadoptionofFSP13-1willsignif-

icantlyimpactourresultsofoperations.

InternalDevelopmentCostsandAbandonedSiteCosts We

capitalizedirectcostsassociatedwiththesiteacquisition

andconstructionofaCompanyunitonthatsite,including

directinternalpayrollandpayroll-relatedcosts.Onlythose

site-specificcosts incurred subsequent tothetimethat

thesiteacquisitionisconsideredprobablearecapitalized.

Ifwesubsequentlymakea determinationthatasite for

which internaldevelopment costs have been capitalized

willnotbeacquiredordeveloped,anypreviouslycapital-

izedinternaldevelopmentcostsareexpensedandincluded

inG&Aexpenses.

Goodwill andIntangible Assets TheCompanyaccounts

foracquisitionsofrestaurantsfromfranchiseesandother

acquisitionsofbusinessthatmayoccurfromtimetotime

inaccordancewithSFASNo.141,“BusinessCombinations”

(“SFAS141”).Goodwillinsuchacquisitionsrepresentsthe

excessofthecostofabusinessacquiredoverthenetof

theamountsassignedtoassetsacquired,includingidenti-

fiableintangibleassets,andliabilitiesassumed.SFAS141

specifiescriteriatobeusedindeterminingwhetherintan-

gibleassetsacquiredinabusinesscombinationmustbe

recognizedandreportedseparatelyfromgoodwill.Webase

amountsassignedtogoodwillandotheridentifiableintangible

assetsonindependentappraisalsorinternalestimates.

TheCompanyaccountsforrecordedgoodwillandother

intangibleassetsinaccordancewithSFASNo.142,“Goodwill

andOtherIntangibleAssets”(“SFAS142”).Inaccordance

withSFAS142,wedonotamortizegoodwillandindefinite-

livedintangibleassets.Weevaluatetheremaininguseful

lifeofanintangibleassetthatisnotbeingamortizedeach

reportingperiodtodeterminewhethereventsandcircum-

stancescontinuetosupportanindefiniteusefullife.Ifan

intangibleassetthatisnotbeingamortizedissubsequently

determined to have a finite useful life, we amortize the

intangibleassetprospectivelyoveritsestimatedremaining

usefullife.Amortizableintangibleassetsareamortizedon

astraight-linebasis.Theweightedaverageusefullifeofour

amortizablefranchisecontractrightsandouramortizable

trademarks/brandsis33yearsand30years,respectively.

As discussed above, we suspend amortization on those

intangibleassets withadefinedlife thatareallocatedto

restaurantsthatareheldforsale.

In accordance with the requirements of SFAS 142,

goodwillhasbeenassignedtoreportingunitsforpurposes

of impairment testing. Our reporting units are our oper-

atingsegmentsintheU.S.(seeNote20)andourbusiness

managementunitsinternationally(typicallyindividualcoun-

tries).Goodwillimpairmenttestsconsistofacomparisonof

eachreportingunit’sfairvaluewithitscarryingvalue.The

fairvalueofareportingunitisanestimateoftheamountfor

whichtheunitasawholecouldbesoldinacurrenttrans-

actionbetweenwillingparties.Wegenerallyestimatefair

valuebasedondiscountedcashflows.Ifthecarryingvalue

ofareportingunitexceedsitsfairvalue,goodwilliswritten

downtoitsimpliedfairvalue.Wehaveselectedthebegin-

ningofourfourthquarterasthedateonwhichtoperform

ourongoingannualimpairmenttestforgoodwill.For2005,

2004and2003,therewasnoimpairmentofgoodwillidenti-

fiedduringourannualimpairmenttesting.

For indefinite-livedintangible assets,ourimpairment

testconsistsofacomparisonofthefairvalueofanintan-

gibleassetwithitscarryingamount.Fairvalueisanestimate

ofthepriceawillingbuyerwouldpayfortheintangibleasset

and is generally estimated by discounting the expected

futurecashflowsassociatedwiththeintangibleasset.We

alsoperformourannualtestforimpairmentofourindefi-

nite-livedintangibleassetsatthebeginningofourfourth

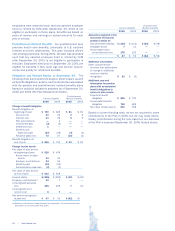

quarter.AsdiscussedinNote9,werecordeda$5million

chargein2003asaresultoftheimpairmentofanindefinite-

livedintangibleasset.Thischargewasrecordedinfacility

actions.Noimpairmentofindefinite-livedintangibleassets

wasrecordedin2005or2004.

Our amortizable intangible assets are evaluated for

impairmentwhenevereventsorchangesincircumstances

indicate thatthecarrying amountof the intangible asset

maynotberecoverable.Anintangibleassetthatisdeemed

impairediswrittendowntoitsestimatedfairvalue,whichis

basedondiscountedcashflows.Forpurposesofourimpair-

mentanalysis,weupdatethecashflowsthatwereinitially

usedtovaluetheamortizableintangibleassettoreflectour

currentestimatesandassumptionsovertheasset’sfuture

remaininglife.

Share-Based Employee Compensation In the four th

quarter 2005, the Company adopted SFAS No. 123

(Revised2004),“Share-BasedPayment”(“SFAS123R”),

which replaces SFASNo. 123 “Accounting for Stock-

BasedCompensation”(“SFAS123”),supersedesAPB25,

“Accountingfor StockIssued toEmployees”andrelated

interpretations and amends SFASNo.95, “Statement

ofCashFlows.”TheprovisionsofSFAS123Raresimilar

to those of SFAS123, however, SFAS123R requires all

new, modified and unvested share-based payments to

employees,includinggrantsofemployeestockoptionsand

restrictedstock,berecognizedinthefinancialstatements

as compensationcost overtheserviceperiod basedon

theirfairvalueonthedateofgrant.Compensationcostis

recognizedovertheserviceperiodonastraight-linebasis

forthefairvalueofawardsthatactuallyvest.

62. | Yum!Brands,Inc.