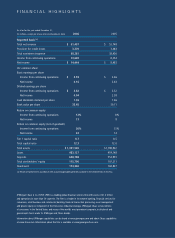

JP Morgan Chase 2006 Annual Report Download - page 9

Download and view the complete annual report

Please find page 9 of the 2006 JP Morgan Chase annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

7

II. LOOKING AHEAD: KEY INITIATIVES

AND ISSUES

There are six important initiatives or issues we are tack-

ling to help us become what we truly want to be – a

consistently high-performing, highly respected financial

services company.

Improving quality and service

Now that our merger work and consolidations are

mainly done, we are turning more attention to improv-

ing quality and service – from front to back. We mean

this in an all-encompassing way, whether it’s a customer’s

experience with a teller, straight-through processing,

improved operations, call center performance, better

automated cross-selling or dozens of other areas. This

applies to anything that affects the customer – and

anything that makes it easier or better for our people

servicing the customer. It includes cutting down on

errors, which cost our company money, slow us down

and annoy the customer.

The outcome, we are convinced, will be happier cus-

tomers and lower attrition, more cross-selling and lower

costs associated with more automation and fewer prob-

lems. The good news is that we have the focus, the will

and the people to do this. They’re the same ones who

already have delivered so much throughout our merger

work and consolidations.

Raising productivity

While over the past few years we have devoted signifi-

cant attention to waste-cutting and cost reduction, we

are now focusing more broadly on productivity overall.

An example would be how we assess the effectiveness of

a sales force. A sales force might have the right number

of salespeople and the right products, but productivity

could still be enhanced in multiple ways: more sales

per salesperson; more sales from new products or old

products; same sales but higher profitability per sale; or

same sales and same profits, but deeper relationships

with customers.

To achieve consistently high margins and returns relative

to the competition, we need to achieve high levels of

productivity everywhere and every step of the way –

at every business unit, in every branch, with every

sales force, in all of our systems programming units

and across all our product marketing. Any company,

including ours, can lose focus or be sloppy in managing

productivity at these levels. Here are a few examples

of how we have improved productivity:

•Investment Bank: We determined that our bankers in

the United States were covering too many clients, and

it is expensive simply to cover a client. While revenue

per banker was adequate, our product penetration per

client was too low. So we reduced the number of

clients each banker covers, and the results should be

very positive: the client should end up getting more

attention, the banker should do more business with the

client, and our revenue should go up. Since we already

had a complete product set for bankers to sell, and

because there are increasingly more companies that

need our services, it was a no-brainer to add bankers.

The Investment Bank this year is also intensifying

its focus on reducing middle-office and back-office

support costs. Our non-compensation expenses are too

high, and as the Investment Bank has developed better

financial management tools, we’re better equipped to

attack these excessive support costs. We believe that

these excess costs could be as much as $500 million.

•Credit card marketing: Last year we did a good job

reducing our costs of attracting, opening and servicing

new credit card accounts. But to maximize opportuni-

ties, we need to become better at matching products to

customers; differentiating between the profitability of