JP Morgan Chase 2006 Annual Report Download - page 10

Download and view the complete annual report

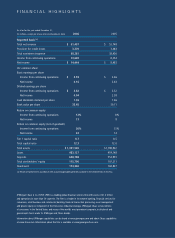

Please find page 10 of the 2006 JP Morgan Chase annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

8

new branch-generated accounts versus those generated

across other channels, such as the Internet; determin-

ing what other business we should be doing with the

new card holder; and ensuring that our current card

holders have the right products and rewards programs.

We already have made good strides: Cards with

rewards programs are now 53% of our card outstand-

ings, up from 32% in 2003. And accounts generated

from direct-mail solicitations, which often come with

low introductory rates (and higher attrition rates), are

down to 32% from 55% in 2003. We have much

more work to do to continue this progress.

•Commercial Banking sales force management: Now

Commercial Banking rigorously tracks results

and profitability by banker and by client. We have

our bankers work with their clients to ensure that all

clients are profitable to the firm and that all clients

benefit from their relationship with the firm.

•New products in Commercial Banking: This past year

Commercial Banking continued to expand its product

offering. It added subordinated debt, mezzanine financ-

ing and even equity investing. We already had the clients.

They just were going elsewhere for these products.

•Private Bank: We’re making it easier for qualified indi-

viduals to do business with us, beginning with how

they open new Private Bank accounts. In the past, they

had to review at least six different documents and sign

multiple times just to start working with us. Now, a

new customer usually fills out only a one-page form

and signs it only once. Everyone’s happier, and we save

some trees.

Increasing marketing creativity and focus

Our company needs to become better at marketing.

And by marketing we don’t mean more television ads or

direct mail solicitations. We mean taking a sophisticated

approach to identifying a group of customers, figuring

out what they need and then delivering it to them better

than anyone else. The opportunities are significant. We

have multiple efforts under way, and we want to give

you a few examples of them.

Develop a better offering for affluent clients

We believe we do a very good job serving our ultra-

high-net-worth clients – those with more than $25

million of investable assets. But we can do a lot more

for the hundreds of thousands of affluent households

that fall below that ultra-high threshold.

Whether through our retail branches, our card business

or our Private Client Services unit, we interact with tens

of thousands of very wealthy individuals every day. But

in many cases, we haven’t identified them as affluent, or

we haven’t focused on providing them with the right set

of products that is tailored to meet their unique needs.

In 2007, we intend to do a comprehensive analysis of

this affluent market, and then develop and begin to exe-

cute a game plan. The likely result will be better identifi-

cation of affluent clients, solutions and rewards pro-

grams that cut across multiple products, more tailored

products, and specialized marketing and servicing.

Use customer knowledge to refine products, upgrade service

Our customers trust us and give us a lot of information

so we can know them better. While respecting a cus-

tomer’s privacy, we can use this information to make

better-informed decisions about what to offer customers

and how to evaluate them.

We’ve already mentioned how we can instantaneously

offer an approved credit card to customers while they are

opening a checking account. We can also underwrite the