ING Direct 2007 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2007 ING Direct annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

|

|

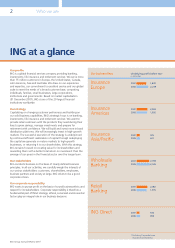

Insurance Europe 19

Insurance Americas 22

Insurance Asia/Pacific 6

Wholesale Banking 25

Retail Banking 22

ING Direct 6

Total 100

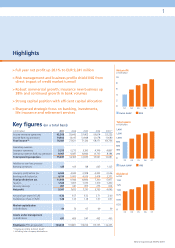

business, notably at ING Direct, ING Real

Estate and Retail Banking activities in

developing markets. Recurring underlying

operating expenses in mature businesses

increased 2.6%. The underlying cost/

income ratio deteriorated to 65.2% from

63.5% in 2006 as a result of the

investments in growth businesses.

Returns remained high with the underlying

RAROC after tax at 22.3%, up from 20.5%

in 2006, reflecting lower tax charges.

ASSET MANAGEMENT

Assets under management increased

EUR 36.9 billion (6.1%) to EUR 636.9 billion

in 2007. Growth was driven by a net inflow

of EUR 40.4 billion. For more detail see the

Asset management section (page 26).

LOOKING FORWARD

ING’s capital position is strong, particularly

after the introduction of Basel II, and ING

is entering 2008 in a position of strength

with strong business fundamentals driving

commercial growth. The operating

environment is likely to remain challenging

going forward, as the economic uncertainty

and market volatility has not come to an

end yet. Creating value for shareholder

remains paramount, and ING has proven

its commitment to enhance shareholder

returns through an attractive increase in

dividends and the ongoing EUR 5.0 billion

share buy-back.

For a full report on the financial highlights,

see the 2007 ING Group Annual Report

and Annual Accounts.

CAPITAL MANAGEMENT

In 2007, we enhanced our strong capital

position thanks to the robust profitability

of the business and good capital

management measures. We used excess

capital to fund significant organic growth,

make acquisitions, buy back shares, and

pay attractive dividends to shareholders.

On balance, ING widened its spare leverage

by a third, further securing our capital base

and providing maximum financial flexibility

to pursue strategic objectives.

Strong capital position

The capital position of ING Group remained

robust during 2007, with all major capital

ratios by year-end within targets consistent

with the Group’s AA– rating target.

We worked to finalise preparations for

Basel II, guidelines that determine the

minimum capital a bank must put aside

to offset unexpected losses. Our Basel II

indicative Tier-1 ratio of approximately

9.9% and total BIS ratio of 13.8% compare

very favourably to our capital ratios under

Basel I, reflecting the moderate risk in ING

Bank’s balance sheet, mainly thanks to our

large mortgage portfolio. We intend, over

the coming years, to bring the capital ratios

back down to their existing targets. The

additional Tier-1 capital available under

Basel II is approximately EUR 7 billion.

Capital adequacy

The main task of the Group Capital

Management function is to monitor,

manage and plan the capital adequacy of

ING Group, ING Bank and ING Insurance,

and to execute all related capital market

transactions. A centralised capital

management is vital to create maximum

financial flexibility to pursue strategic

objectives and withstand financial stress,

and ensure the various requirements of

shareholders, regulators, rating agencies

and internal economic capital models can

be properly balanced.

ING endeavours to employ its capital in the

most optimal way. It is therefore important

that business units are incentivised to

hold only the capital they need to support

the risks in their business and can count

on capital injections so their business can

grow profitably.

Many ING insurance businesses need to

hold more capital than their economic

capital due to regulatory and/or rating

agency constraints. However, free surplus

(capital not being employed as economic

capital) not so constrained can be used

elsewhere to deliver further profitable

growth. During 2007, EUR 5.8 billion of

dividends were paid by ING Insurance

Netherlands back up to Group level, where

it can be strategically deployed to where it

can help deliver further growth.

Share buy-back

We foresaw that, without further

intervention, significant excess capital

would continue to build during 2007.

We therefore decided to carry out a

EUR 5 billion share buy-back, spread

over a year from June 2007. By year-end,

90.7 million shares had been repurchased

for EUR 2.8 billion. Once completed,

the share buy-back will improve EPS by

around 7%.

Capital Management was also involved

in the repurchase of the ING preference

shares of both Fortis and ABN AMRO

during 2007, following repurchase of

Aegon’s preference shares in 2006. All

three major holders have now sold their

ING preference shares back to ING Group.

Acquisitions and divestments

For the first time in many years, 2007 saw

significant acquisition and divestment

activity, including two major acquisitions:

Oyak Bank in Turkey and pension fund

businesses in Latin America for a total

cost of EUR 2.5 billion.

Contribution business lines 2007 underlying profit before tax

in percentages

11

ING Group Annual Review 2007