Huntington National Bank 2004 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2004 Huntington National Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

|

|

18

During 2004, we also developed a new banking office general manager program, which provides additional career and compensation

opportunities for our best-performing managers. This is structured to improve banking office performance by sharing the

banking office’s profitability with the manager. The program was implemented January 1, 2005, with 10% of our managers

participating initially.

Our people make the difference, whether that is a drive-in teller cashing a check, a mortgage sales representative helping a customer

purchase his or her first home, or a business banker working with small business owners to finance their building. We will continue

to hire, train, and retain the best people. We have good competitive products, with many convenient ways for our customers to do

their banking with us, and we plan to enhance continually the tools we provide our associates, allowing every customer to experience

“Simply the Best” service.

Commercial Banking

Our Commercial Banking strategy is to build long-term profitable partnerships with ideal Huntington clients. These are companies

in our markets that have annual sales of $10 – $500 million and need financial relationships with partners who can provide

innovative advice and ideas, not just a loan. Ideal clients have a preference for a primary bank that aligns with our value proposition,

which is to support our clients’ total cash flow needs whether they have money to invest, transactions to complete, or need money

to finance growth. As partners, we understand our purpose is to help them build ownership value through good investment returns,

efficient cash collection and disbursement, and access to flexible borrowings or capital markets.

Our structure allows our local bankers to deliver all of this with ease. We provide current and prospective customers with

knowledgeable commercial bankers who focus on providing innovative ideas and solutions. Key to this process has been the

development of the ideal Huntington client profile system that permits us to focus on the customers with the highest potential

for a long-term relationship.

Our “local bank with national resources” model ensures that we make decisions “close to the customer” while utilizing sophisticated

financing and servicing options to develop customized financial solutions. These options include treasury and cash management,

interest rate risk management, loan syndications, trade financing, foreign exchange, leasing, 401(k) plan services, investment

management, custody services, and private banking services.

Huntington commercial bankers have embraced a standard sales process that includes system-wide relationship and business

banking models and formal sales training for commercial associates. We continually redesign workflows for customer service and

administrative support to improve productivity and make it easier to sell a range of new products.

We have the size and reputation to attract the best commercial bankers available. They receive the education and support necessary

to provide a complete array of services to customers. Each commercial banker’s skill is improved as we measure performance and

provide feedback based on common reporting across all of our regions.

Having a solid credit culture to deliver excellent risk management is critical. To ensure all regions follow the same “blueprint”in

evaluating credit, we have established guiding principles delivered through a uniform credit training program across all regions.

It starts with formal credit training and ends with a program of continuing education for commercial credit officers. All commercial

bankers are required to complete the training.

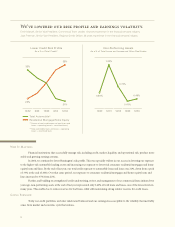

The combination of our focus on ideal Huntington clients and the discipline of our credit culture has permitted us to reduce credit

risk while growing our customer base. Year-end non-performing assets were near the lowest level in many years, and the number

of ideal Huntington clients has grown.

Now our objective is to become more efficient in the way we execute our sales, service, and credit strategies. During 2004, a number

of end-to-end process improvements were installed. As a result of these changes, our relationship managers have increased the

time spent each day on business development activities from 30% to 50%. This significant increase in productivity is paying off

for our customers.

We are confident about our ability to grow our commercial business. We know there is ample opportunity to develop commercial

banking relationships in our markets with ideal Huntington clients. Our strategy is to position Huntington as their partner.