Goldman Sachs 2003 Annual Report Download - page 9

Download and view the complete annual report

Please find page 9 of the 2003 Goldman Sachs annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

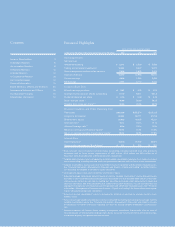

GOLDMAN SACHS 2003 ANNUAL REPORT 7

Letter to Shareholders

ability to generate attractive investment performance

and the ability to raise new assets.

During 2003, our investment performance, together

with our distribution strength, allowed us to generate

$15 billion of net client inflows across non-money

market asset classes. These increases were offset by

$19 billion of outflows in money market assets, as

economic prospects improved and higher returns were

being generated in other asset classes.

Within our Securities Services business, net revenues

were $1.01 billion, up 17% from 2002. This business

continues to benefit from the creation and growth of

new and existing hedge funds. In addition, the rally in

equity markets helped to increase customer balances.

We believe our Asset Management and Securities

Services business represents one of our best opportuni-

ties for substantial growth.

EXPENSES

Managing expenses in this challenging environment

has been one of our highest priorities. During 2003,

excluding the impact of acquisitions, we reduced our

headcount by 7%. While painful, these reductions

were necessary to scale our operations to the available

opportunities and were a key factor in our ability to

generate an attractive return in 2003.

Our largest expense—in a people business —is

compensation, and we track this expense as a percent-

age of the net revenues we generate in our businesses

overall. For 2003, the ratio of compensation to net

revenues was 46% versus 48% in 2002.

We remain focused on controlling our non-compen-

sation expenses. However, there are some areas that

remain difficult to forecast. For instance, in 2003 we

took provisions of $159 million for a number of litiga-

tion and regulatory proceedings. Given the range of

litigation and investigations underway, these expenses

may remain high.

STRATEGY AND COMPETITIVE DYNAMICS

Goldman Sachs is not a financial services conglomerate

but an integrated investment bank, securities firm and

asset manager. This focused strategy has allowed us

to build a strong global franchise—we take pride in

being a market leader in Europe and Asia as well as

the United States. It has also allowed us to benefit

from the long-term growth of the global capital mar-

kets which we believe will continue to provide us with

excellent growth opportunities over the cycle.

We aspire to be the preeminent global provider of

advisory, financing, investment and risk management

services to corporations, institutions, governments and

high-net-worth individuals. To succeed in this mission,

the firm has always placed great reliance on attracting

and retaining outstanding people. And we work hard

to foster teamwork and encourage creativity, client

focus and innovation. We believe that our unique cul-

ture, coupled with the quality of our people, is

Goldman Sachs’ most important competitive strength.

Our business has always been highly competitive

and cyclical. We face strong competition today, as in

the past, from larger competitors, but we don’t view

our size as a competitive disadvantage because we

have never been constrained by a lack of capital. We

believe our biggest challenge is to strengthen our culture

of teamwork and excellence in the face of the growing

size and scope of our business. We are determined to

meet this challenge because we believe our ability to

do so is critical to our continued success in executing

our global strategy and serving our clients.

STRATEGIC TRANSACTIONS

In 2003, we completed a number of strategic transac-

tions. Our first announcement involved our $1.25

billion investment in SMFG, which we mentioned

above. We are pleased with the performance of our

investment as well as the other aspects of our relation-

ship with SMFG.

With the credit loss protection provided by SMFG,

we initiated our William Street credit extension pro-

gram. This capability has given us an innovative way

to extend credit selectively to our investment-grade

clients, while reducing our credit and liquidity risks.

By the end of fiscal 2003, $4.32 billion of credit com-

mitments had been made under the program. In addi-

tion, our business cooperation agreement with SMFG

has already resulted in a number of initiatives. In

October, we announced the formation of a joint venture

to facilitate the corporate recovery of certain SMFG

borrowing clients and to accelerate SMFG’s plans to

improve its asset quality.

In September, we combined our Australian opera-

tions with JBWere to create a new venture called

Goldman Sachs JBWere. We own 45% of the new entity,

one of the leading investment banking and securities

firms in Australia.

We also made several acquisitions in 2003. Our

approach to acquisitions is to strengthen our business

and build shareholder value, principally through empha-

sizing bolt-on deals where we can add new clients or

acquire new products to provide to our existing clients.

2003 offered us a number of such opportunities.

In July, we acquired The Ayco Company, a leading

provider of sophisticated, fee-based financial counsel-