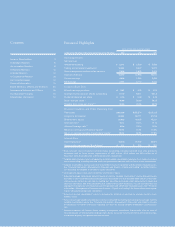

Goldman Sachs 2003 Annual Report Download - page 6

Download and view the complete annual report

Please find page 6 of the 2003 Goldman Sachs annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

4GOLDMAN SACHS 2003 ANNUAL REPORT

Letter to Shareholders

INVESTMENT BANKING

Investment banking activity continued to suffer from

diminished corporate and investor confidence in a

tough business environment. Industry volumes for

completed mergers decreased again in 2003 and equity

underwriting volumes remained low. Global completed

mergers decreased 17% from 2002, and were 70%

below volumes in 2000, the prior peak. Our results

reflected this difficult industry environment. Investment

Banking net revenues were $2.71 billion, down 4%

from 2002, and pre-tax earnings were $207 million,

down from $376 million the year before.

However, despite this difficult environment, we

maintained our focus on serving clients and continued

as the market leader in our core franchise businesses,

including mergers and acquisitions, and IPO, equity,

and equity-linked underwriting. In addition, we devel-

oped a prominent position in the issuance of high-yield

securities. We think the strength of our franchise and

the quality of our client relationships are evident in this

performance. We do not, however, seek to be number

one in all areas. Pursuing market share in some prod-

ucts makes no sense to us when the profitability is too

small or non-existent.

We believe that our role as a core advisor to clients

has never been stronger. Our investment banking pro-

fessionals continue to play a vital role in advising senior

executives and a broad range of clients throughout the

world. Through these relationships, our people are able

to identify the needs of our clients and offer solutions

by providing advice, products and services from across

our firm.

TRADING AND PRINCIPAL INVESTMENTS

Once again in 2003, Trading and Principal Investments

produced excellent results. Net revenues were $10.44

billion, a 21% increase from 2002. Pre-tax earnings

were $3.51 billion, a 64% increase from 2002.

We measure the effectiveness of our trading busi-

nesses by evaluating overall profitability relative to the

risk we assume and the opportunities available. While

there is no perfect measure of market risk, a topic

we’ll discuss later in this letter, our risk levels were

higher in 2003 than in 2002. We were very pleased

with the results our businesses were able to produce by

effectively deploying incremental capital.

Fixed Income, Currency and Commodities (FICC)

had another record year, with net revenues of $5.60

billion, a 20% increase from 2002. During 2003, FICC

operated in a generally favorable environment charac-

terized by tightening corporate credit spreads, low

interest rates, a steep yield curve and strong customer

demand. As we look forward to 2004, we do not see

clear signs that FICC activity levels will slow.

However, we know that there is no such thing as a

trading backlog and our business opportunities will

always depend on the overall environment.

One important aspect of our FICC business that is

often overlooked is the range and diversity of activities

it comprises. Within the five major areas of FICC—

interest rates, credit, mortgages, currencies and com-

modities—are a wide range of individual operations

around the globe. While there can be no guarantee

about performance in any of our businesses, we believe

that this diversity is an important strength.

Our Equities business continued to face a very chal-

lenging environment. Equities net revenues of $4.28

billion increased 7% compared with 2002, primarily

due to higher net revenues in principal strategies. While

equity markets certainly improved in 2003 relative to

the previous few years, conditions remained tough.

Commission rates and spreads have continued to

decline, the need to commit capital in a variety of cir-

cumstances is rising and volume growth is low.

At Goldman Sachs, we have focused on the optimal

size and structure for our Equities business in this dif-

ficult environment. We are pleased with the results of

this effort, which we believe will be an important driver

of future performance.

Beginning with the appointment in 2002 of com-

mon management for our securities businesses, we

have been more closely coordinating the activities of

our FICC and Equities businesses to share best prac-

tices, capture synergies and drive efficiencies. In 2003,

we continued this work, combining our Equities cash

and derivatives client businesses under one leadership

team. This builds on the experience of a similar combi-

nation in FICC in 2000 and will position us well to

capture a range of opportunities.

RESEARCH

Research remains a critically important part of the

Goldman Sachs franchise. We believe that a strong,

differentiated research effort that is firmly aligned with

the interests of our investing clients will be an important

part of our Equities business for many years to come.

Of course, 2003 began with the brokerage industry’s

global settlement with various regulators on equities

research-related matters. As we have said before, in

hindsight we and others could have done a better job.

However, we had already begun implementing changes

in our research business long before the final settle-

ment, and we have been working diligently to comply

in every respect with the new ground rules.