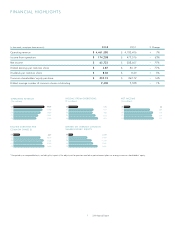

Washington Post 2008 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2008 Washington Post annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

out as planned. But these charges can have curi-

ous results: in early 2006, we purchased $43

million in a publicly traded stock. The stock fell

during the year; the accountants required a $14

million write-down charge in the fourth quarter.

The stock subsequently recovered to its purchase

price and beyond. We sold it in the fourth quarter

of 2008 for a gain of “$21 million.” I put the sum

in quotation marks because that gain includes the

$14 million recovery of the write-down in the

stock — in other words, the Company received

(pre-tax) $7 million more than we paid for the

stock, but recorded a $21 million gain because of

the earlier write-down. It is a curious feature of

these non-cash charges that they only go one

way: if the value of an asset recovers, you don’t

write it back up through earnings.

Still, you won’t record write-downs if your acqui-

sitions and investments are all home runs.

Many CEOs’ annual reports will say more about

their balance sheets than they have for years;

this one is no exception. Our Company for many

years has had $400 million of notes outstand-

ing; unfortunately, these came due in February.

The Post has an A1 credit rating from Moody’s;

we are told that ranks us in the top 10% of non-

financial S&P 500 companies. Nonetheless, the

coupon rate when we refinanced our debt was

much higher: 7.25% in 2009, compared to

5.5% in 1999. We still have enough cash and

marketable securities to cover the debt.

The Company can handle the added interest

cost. But to have no debt at all — unless for a very

compelling reason — seems wiser than ever. It

should not have taken the 2008 financial crisis

to make me tighten my definition of “very com-

pelling” acquisitions — but it did.

Our Businesses

Education: Kaplan is a very strong business.

It has stronger and weaker businesses among

its components. Its largest businesses, higher

education and test prep, should be our most

countercyclical (and higher education is by far

Kaplan’s strongest business).

Our professional training business includes some

wonderful assets, but we also have a consider-

able exposure to the U.S. real estate training

market and the worldwide finance training mar-

kets. Long run, we believe the Company will make

money in those markets; in the U.S., we certainly

did not in 2008 and won’t in 2009. Score also

struggles, and its losses continue.

Despite these losses and investments, Kaplan

recorded higher revenue and profit in 2008.

The biggest change at Kaplan in 2008 was in

management: Jonathan Grayer resigned after

17 outstanding years at Kaplan, 14 as CEO.

Jonathan led Kaplan from a money-losing test

prep business to a $2 billion-plus multidisciplinary,

multinational company (and a highly profitable

52008 Annual Report