Trend Micro 2009 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2009 Trend Micro annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

|

|

16

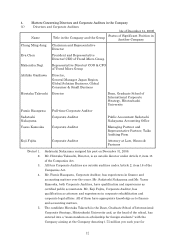

5. Status of Accounting Auditor

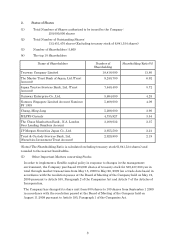

(1) Name of accounting auditor of the Company

KPMG AZSA & Co.

(2) Remuneration, Etc. Paid to Accounting Auditor

(Millions of yen)

(i) Amount of fees and charges paid to accounting auditors for the

term under review 98

(ii) Total amount of cash and other financial benefits payable by

the Company and its subsidiaries 105

(Notes) 1. As the audit fees under the Companies Act and those under the Financial

Instruments and Exchange Act are not separated for the purpose of the audit

contract executed between the Company and the accounting auditors and are

impractical to separate, the amount specified in (i) above is indicated as the total

amount of audit fees payable under both laws.

2. The amount specified in (ii) above includes 7 million yen as compensation for

advisory services concerning internal controls relating to financial reporting, which

are services other than the services stipulated under Article 2, Paragraph 1 of the

Certified Public Accountant Law (Non-audit services).

3. Three of the important subsidiaries of the Company are audited by certified public

accountants or audit corporations other than the accounting auditor of the Company

(including qualified persons equivalent thereto in foreign countries) .

(3) The policy regarding decisions on the dismissal or discontinuance of reelection an

accounting auditor

If the Accounting Auditor is deemed to fall under any of the items prescribed in Article

340, Paragraph 1 of the Companies Act, the Accounting Auditor will be dismissed by the

Board of Corporate Auditors pursuant to an unanimous consent of the Corporate

Auditors.

In addition to the above, if it is deemed difficult for the Accounting Auditor to carry out

their proper execution of the duties and / or in consideration of the length of their

continuous services years of the audit, and of other factors, The Board of Directors will

submit a proposal for dismissal or discontinuance of reelection of the Accounting Auditor

as the Agenda of the Shareholders Meeting upon agreement or request of the Board of

Corporate Auditors.