SunTrust 2011 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

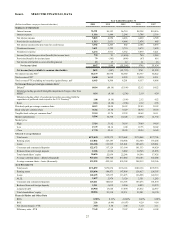

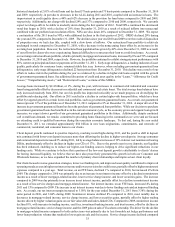

36

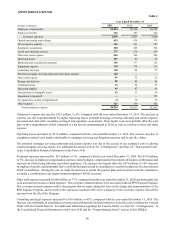

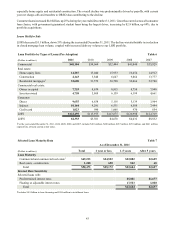

Analysis of Changes in Net Interest Income 1

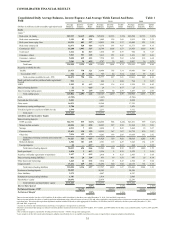

(Dollars in millions on a taxable-

equivalent basis)

Interest Income

Loans:

Real estate 1-4 family

Real estate construction

Real estate home equity lines

Real estate commercial

Commercial - FTE2

Credit card

Consumer - direct

Consumer - indirect

Nonaccrual

Securities available for sale:

Taxable

Tax-exempt 2

Funds sold and securities purchased under

agreements to resell

LHFS

Interest-bearing deposits

Interest earning trading assets

Total interest income

Interest Expense

NOW accounts

Money market accounts

Savings

Consumer time

Other time

Brokered time deposits

Foreign deposits

Funds purchased

Securities sold under agreements to

repurchase

Interest-bearing trading liabilities

Other short-term borrowings

Long-term debt

Total interest expense

Net change in net interest income

2011 Compared to 2010

Increase (Decrease) Due to

Volume

$9

(50)

(21)

(69)

185

(4)

64

107

(11)

(32)

(15)

—

(43)

—

14

134

—

20

1

(31)

(40)

(11)

(1)

(1)

(1)

—

2

(89)

(151)

$285

Rate

($143)

8

—

(4)

(68)

(3)

6

(92)

6

17

1

(1)

(1)

—

(24)

(298)

(23)

(87)

(3)

(37)

(27)

2

1

—

—

(5)

(2)

(41)

(222)

($76)

Net

($134)

(42)

(21)

(73)

117

(7)

70

15

(5)

(15)

(14)

(1)

(44)

—

(10)

(164)

(23)

(67)

(2)

(68)

(67)

(9)

—

(1)

(1)

(5)

—

(130)

(373)

$209

2010 Compared to 2009 Increase

(Decrease) Due to

Volume

($31)

(93)

(25)

(40)

(193)

6

30

56

(2)

217

(12)

1

(81)

—

(19)

(186)

4

61

1

(63)

(97)

(108)

—

(1)

—

13

1

(147)

(336)

$150

Rate

($138)

21

4

(6)

201

9

14

(51)

5

(222)

(1)

(2)

(15)

—

(7)

(188)

(45)

(148)

(2)

(149)

(97)

64

—

—

(1)

(3)

(3)

(35)

(419)

$231

Table 2

Net

($169)

(72)

(21)

(46)

8

15

44

5

3

(5)

(13)

(1)

(96)

—

(26)

(374)

(41)

(87)

(1)

(212)

(194)

(44)

—

(1)

(1)

10

(2)

(182)

(755)

$381

1Changes in net interest income are attributed to either changes in average balances (volume change) or changes in average rates (rate change) for earning assets

and sources of funds on which interest is received or paid. Volume change is calculated as change in volume times the previous rate, while rate change is change

in rate times the previous volume. The rate/volume change, change in rate times change in volume, is allocated between volume change and rate change at the

ratio each component bears to the absolute value of their total.

2Interest income includes the effects of the taxable-equivalent adjustments to increase tax-exempt interest income to a taxable-equivalent basis.

Net Interest Income/Margin

Net interest income, on an FTE basis, was $5.2 billion during 2011, an increase of $209 million, up 4%, from 2010. This

increase was predominantly driven by a continued positive trend in net interest margin, which increased by 12 basis points

to 3.50% in 2011 from 3.38% in 2010. Earning asset yields declined by 13 basis points to 4.26%, compared with 4.39%

during 2010, while the cost of interest-bearing liabilities decreased by 30 basis points over the same period. Net interest

margin increased, predominantly due to the growth in lower-cost deposits, specifically DDA and money market accounts,

along with a decrease in higher-cost time deposits and long-term debt. We expect the net interest margin to decline modestly

in the first quarter of 2012, as earning asset yield compression is expected as a result of the continued low rate environment.

Average earning assets increased by $0.6 billion, or less than 1%, compared with 2010. The increase was predominantly due

to an increase in average loans, which was up by $2.4 billion, or 2%. The increase in loans was primarily attributable to

increases of $3.5 billion, or 11%, in commercial loans, primarily driven by our large corporate borrowers, $2.2 billion, or

29%, in consumer-indirect loans, driven by purchases of high quality auto loan portfolios, and $1.4 billion, or 25%, of

consumer-direct loans related to an increase in government-guaranteed student loans. These increases were partially offset