Stein Mart 2010 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2010 Stein Mart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

|

|

16

Net cash used in investing activities, solely for capital expenditures, was $(29.6) million in 2010, $(7.6) million in 2009 and $(19.3)

million in 2008. Capital expenditures for 2010 include approximately $19 million for systems improvements, with the largest portion

for our new merchandise information system. The remaining capital amounts are for improvements in our point-of-sale system,

upgrades to store fixtures and for new and relocated stores. Capital expenditures for 2009 compared to 2008 reflect a decrease in

the number of store openings.

Net cash (used in) provided by financing activities was $(20.9) million in 2010, $(98.7) million in 2009 and $73.7 million in 2008. We

paid $22.2 million in dividends in 2010 and had no activity on our revolving credit agreement. More cash was used in 2009 for the

repayment of all direct borrowings under our credit agreement while 2008 had cash provided by net borrowings on the credit

agreement.

We expect to invest approximately $25 to $30 million in capital expenditures in 2011. The cost of opening a new store ranges from

$550,000 to $600,000 for fixtures, equipment, leasehold improvements and pre-opening costs (primarily advertising, stocking and

training). Pre-opening costs are expensed at the time of opening. Initial inventory investment for a new store is approximately

$800,000.

We have a $150 million senior revolving secured credit agreement (the “Agreement”) with a group of lenders which extends through

January 2012. We expect to enter into a new credit agreement before the end of 2011. The amount available for borrowing was

$139.2 million at January 29, 2011 and is based on a percentage of eligible inventories less reserves, as defined in the Agreement.

Availability was further reduced to $130.6 million after deducting outstanding letters of credit of $8.6 million. We had no direct

borrowings at January 29, 2011 and are in compliance with the terms of the Agreement.

We believe that we will continue to generate positive cash flow from operations, which, along with our available cash and borrowing

capacity under the revolving credit agreement, will provide the means needed to fund our operations for the foreseeable future.

Contractual Obligations

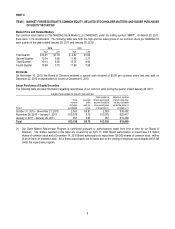

The following table sets forth our contractual obligations at January 29, 2011 (in thousands):

Total

Less than

1 Yea

r

1 – 2

Years

3 – 5

Years

After 5

Years

Operating leases $316,446 $ 72,477 $61,885 $125,760 $56,324

Purchase obligations (a) 210,559 210,559 - - -

Total $527,005 $283,036 $61,885 $125,760 $56,324

(a) Represent open purchase orders with vendors for merchandise not yet received and recorded on our Consolidated Balance Sheet.

The above table does not include long-term debt as we did not have any direct borrowings under our senior revolving credit facility at

January 29, 2011. Other long-term liabilities on the balance sheet include the liability for unrecognized tax benefits, deferred

compensation, deferred rent liability, postretirement benefit liability and other long-term liabilities that do not have specific due dates,

so are excluded from the preceding table. Other long-term liabilities also include long-term store closing reserves, a component of

which is future minimum payments under non-cancelable leases for closed stores. These future minimum lease payments for these

closed stores total $5.0 million and are included in the above table.

Off-Balance Sheet Arrangements

We have outstanding standby letters of credit totaling $8.6 million securing certain insurance programs at January 29, 2011. If certain

conditions were to occur under these arrangements, we would be required to satisfy the obligations in cash. Due to the nature of

these arrangements and based on historical experience, we do not expect to make any payments; therefore, the letters of credit are

excluded from the preceding table. There are no other off-balance sheet arrangements that could affect our financial condition.

Critical Accounting Policies and Estimates

The preparation of our consolidated financial statements requires management to make estimates and assumptions that affect the

reported amounts of assets, liabilities, expenses and related disclosure of contingent assets and liabilities. Management bases its

estimates and judgments on historical experience and other relevant factors, the results of which form the basis for making judgments

about the carrying values of assets and liabilities that are not readily apparent from other sources. While we believe that the historical

experience and other factors considered provide a meaningful basis for the accounting policies applied in the preparation of the

financial statements, we cannot guarantee that our estimates and assumptions will be accurate, which could require adjustments of

these estimates in future periods. A summary of the more significant accounting policies follows.