Progressive 2005 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 2005 Progressive annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

|

|

.11

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

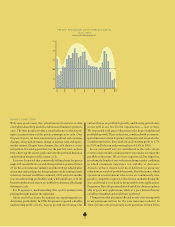

4.2% from the prior three-year average of 8%. For 2005, we

estimate the year-over-year increase in net premiums written

for the auto insurance industry will be about 1%. Our knowl-

edge of the calculus combining price, growth and profit,

while increasing, remains a challenge and something we want to

be smart about.

Reviewing Progressive’s and the industry’s results through 2005

and noting the possible analogue to past cycles, we would make a

few important observations. Operating margins, while historically

strong, are starting to deteriorate. Modestly increasing severity,

notably in physical damage coverages, combined with price

reductions, will likely reduce current margins. Prior period bod-

ily injury severities, which have the highest sensitivity to carried

reserves, have generally been overestimated resulting in favorable

calendar-period adjustments. In Progressive’s case, the overall

favorable calendar-year adjustment was 2.6 points for 2005.

Calendar-period reporting has a way of disguising the run rate and

perhaps delaying appropriate reactions. We have for some time

forecast that Progressive would slowly return to more normal

operating margins by allowing expected increases in severity, and

potentially frequency, to absorb the margin in excess of our target

rather than immediately price it away. We continue to believe this

is the right way for us to address these market conditions.

We see 2006 as a year when accident-year results both for

Progressive and the industry may begin producing smaller mar-

gins and trending toward more historical norms. As with any out-

look there are unknowns. The level of price activity and the

degree of severity and frequency change will be critical as we play

our hand during this phase of the cycle.

History has been an influential teacher and as we work through

this phase of the cycle many things are different and, we think, bet-

ter for us. Our personal auto policy periods are shorter, providing

greater flexibility to price correctly and our controls and analytic

review of profitability by subsegments of our book are more rigor-

ous. We are clearer about our expected outcomes. Loss cost and

expense management are all considerably tighter and our technol-

ogy and operational performance are considerably improved.

While accepting that current market conditions will likely

continue to influence our growth during 2006, and that growth

will be less than we believe we are ready to handle, we have

embraced this time and opportunity as one of “maximum

preparedness” for the future we anticipate.