National Grid 2007 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2007 National Grid annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

|

|

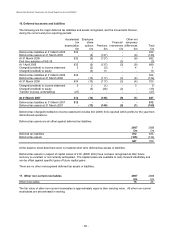

National Grid Electricity Transmission plc Annual Report and Accounts 2006/07

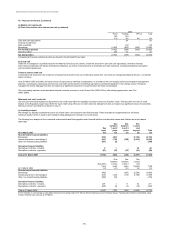

18. Derivative financial instruments

Derivatives are financial instruments that derive their value from the price of an underlying item such as interest rates, foreign

exchange, credit spreads and equity or other indices. Derivatives enable their users to alter exposure to market or credit risks. We

use derivatives to manage our treasury risks.

Derivatives are carried at fair value and are shown in the balance sheet as separate totals of assets and liabilities. Asset values

represent the cost of replacing all transactions with a fair value in our favour assuming that all relevant counterparties default at

the same time, and that the transactions can be replaced immediately in the market. Liability values represent the cost to

counterparties of replacing all their transactions with a fair value in their favour in the case of default. Derivative assets and liabilities

on different transactions are only netted off if the transactions are with the same counterparty, a legal right of set-off exists and the

cash flows are intended to be settled on a net basis.

Treasury financial instruments

Derivatives are used for hedging purposes in the management of exposure to market risks. This enables the optimisation of the

overall cost of accessing debt capital markets, and to mitigate the market risk which would otherwise arise from the maturity and

other profiles of its assets and liabilities.

Hedging policies using derivative financial instruments are further explained in note 19. Derivatives that are held as hedging

instruments are formally designated as hedges as defined in IAS 39. Derivatives may qualify as hedges for accounting purposes if

they are fair value hedges or net investment hedges. These are described as follows:

Fair value hedges

Fair value hedges principally consist of interest rate and cross-currency swaps that are used to protect against changes in the fair

value of fixed-rate, long-term financial instruments due to movements in market interest rates. For qualifying fair value hedges, all

changes in the fair value of the derivative and changes in the fair value of the item in relation to the risk being hedged are recognised

in the income statement. If the hedge relationship is terminated, the fair value adjustment to the hedged item continues to be reported

as part of the basis of the item and is amortised to the income statement as a yield adjustment over the remainder of the hedging period.

Cash flow hedges

Exposure arises from the variability in future interest and currency cash flows on assets and liabilities which bear interest at variable

rates. Interest rate and cross-currency swaps are maintained, and designated as cash flow hedges, where they qualify, to manage

this exposure. Fair value changes on designated cash flow hedges are initially recognised directly in the cash flow hedge

reserve, as gains or losses recognised in equity. Amounts are transferred from equity and recognised in the income statement as

the income or expense is recognised on the hedged asset or liability.

Forward foreign currency contracts are used to hedge anticipated and committed future cash flows. Where these contracts qualify

for hedge accounting they are designated as cash flow hedges. On recognition of the underlying transaction in the financial statements,

the associated hedge gains and losses deferred in equity are transferred and included with the recognition of the underlying transaction.

The gains and losses on ineffective portions of such derivatives are recognised immediately in the income statement.

When a hedging instrument expires or is sold, or when a hedge no longer meets the criteria for hedge accounting, any cumulative

gain or loss existing in equity at that time remains in equity and is recognised when the forecast transaction is ultimately recognised

in the income statement or on the balance sheet. When a forecast transaction is no longer expected to occur, the cumulative gain or

loss that was reported in equity is immediately transferred to the income statement.

Derivatives not in a formal hedge relationship

Our policy is not to use derivatives for trading purposes, however due to the complex nature of hedge accounting under IAS 39,

some derivatives may not qualify for hedge acccounting, or are specifically not designated as a hedge where natural offset is more

appropriate.

Changes in the fair value of any derivative instruments that do not qualify for hedge accounting are recognised immediately in the

income statement within interest expense and other finance costs.

Operational financial instruments

Commodity derivatives are used to manage commodity prices associated with our electricity transmission operations. As these contracts

are for normal usage in our operations and are not settled net, they are carried at cost and are recognised within trade receivables

or payables as appropriate.

- 56 -