Motorola 2014 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2014 Motorola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

72

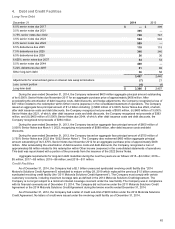

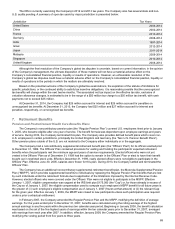

Actuarial Assumptions

Certain actuarial assumptions such as the discount rate and the long-term rate of return on plan assets have a significant

effect on the amounts reported for net periodic cost and benefit obligation. The assumed discount rates reflect the prevailing

market rates of a universe of high-quality, non-callable, corporate bonds currently available that, if the obligation were settled at

the measurement date, would provide the necessary future cash flows to pay the benefit obligation when due. The long-term

rates of return on plan assets represent an estimate of long-term returns on an investment portfolio consisting of a mixture of

equities, fixed income, cash and other investments similar to the actual investment mix. In determining the long-term return on

plan assets, the Company considers long-term rates of return on the asset classes (both historical and forecasted) in which the

Company expects the plan funds to be invested.

Weighted average actuarial assumptions used to determine costs for the plans at the beginning of the fiscal year were as

follows:

U.S. Pension Benefit

Plans Non U.S. Pension

Benefit Plans

Postretirement

Health Care Benefits

Plan

2014 2013 2014 2013 2014 2013

Discount rate 5.15% 4.35% 4.24% 4.20% 4.65% 3.80%

Investment return assumption 7.00% 7.00% 5.92% 6.13% 7.00% 7.00%

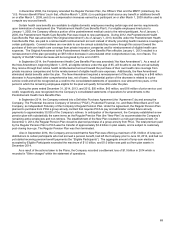

Weighted average actuarial assumptions used to determine benefit obligations for the plans were as follows:

U.S. Pension Benefit

Plans Non U.S. Pension

Benefit Plans

Postretirement

Health Care Benefits

Plan

2014 2013 2014 2013 2014 2013

Discount rate 4.30% 5.15% 3.19% 4.24% 3.90% 4.65%

Future compensation increase rate n/a n/a 2.54% 2.58% n/a n/a

The accumulated benefit obligations for the plans were as follows:

U.S. Pension Benefit

Plans Non U.S. Pension

Benefit Plans

December 31 2014 2013 2014 2013

Accumulated benefit obligation $ 4,536 $ 7,317 $ 2,059 $ 1,900

In September 2014, as a result of establishing the New Plan, the Company remeasured the Regular Pension Plan using a

weighted average discount rate and expected long-term rate of return on assets of 4.25%. The Regular Pension Plan was

subsequently terminated. The New Plan, which is the surviving plan, was measured using a discount rate and expected long-

term rate of return on assets of 4.70% and 7.00%, respectively.

In September 2014, as a result of retiree healthcare design plan changes, the company remeasured the retiree healthcare

plan using a weighted average discount rate and expected long-term rates of return on assets of 4.15% and 7.00%, respectively.

During 2014, the Company adopted the "RP 2014 White Collar" mortality table for purposes of calculating the projected

benefit obligation for the Company's New Plan.

The health care cost trend rate used to determine the December 31, 2014 accumulated postretirement benefit obligation

and 2015 net periodic benefit for the Postretirement Health Care Benefits Plan was 7.75%, grading down to a rate of 5.00% in

2021. The health care cost trend rate used to determine the December 31, 2013 accumulated postretirement benefit obligation

and 2014 net periodic benefit was 8.50%, remaining flat at 8.50% through 2015, then grading down to a rate of 5.00% in 2020.

The effect of changing the health care trend rate by one percentage point on the accumulated postretirement benefit

obligation and the net periodic cost of the Postretirement Health Care Benefits Plan is de minimis. The Company maintains a

lifetime cap on postretirement health care costs, which reduces the liability duration of the plan. A result of this lower duration, is

a decreased sensitivity to a change in the discount rate trend and health care cost assumptions with respect to the liability and

related expense.