John Deere 2009 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2009 John Deere annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

FINANCIAL SERVICES

The Financial Services’ credit operations rely on their ability to

raise substantial amounts of funds to fi nance their receivable and

lease portfolios. Their primary sources of funds for this purpose

are a combination of commercial paper, term debt, securitization

of retail notes and equity capital.

Cash fl ows from the Financial Services’ operating activities,

including intercompany cash fl ows, were $897 million in 2009.

The cash provided by operating activities was used primarily for

investing and fi nancing activities. Cash used by investing activities

totaled $331 million in 2009, primarily due to the cost of

receivables and equipment on operating leases exceeding

collections of receivables and the proceeds from sales of equip-

ment on operating leases by $265 million and purchases of

property and equipment of $119 million, partially offset by

proceeds from sales of fi nancing receivables of $34 million.

Cash used for fi nancing activities totaled $796 million in 2009,

representing primarily a decrease in borrowings from Deere &

Company of $551 million and a $189 million decrease in external

borrowings. Cash and cash equivalents decreased $215 million.

Over the last three years, the Financial Services’

operating activities, including intercompany cash fl ows, have

provided $2,687 million in cash. In addition, an increase in

total borrowings of $2,488 million, capital investment from

Deere & Company of $663 million and proceeds from sales

of fi nancing receivables of $353 million provided cash infl ows.

These amounts have been used mainly to fund receivable and

equipment on operating lease acquisitions, which exceeded

collections and the proceeds from sales of equipment on operating

leases by $3,268 million, pay dividends to Deere & Company of

$1,153 million and fund purchases of property and equipment

of $923 million. Cash and cash equivalents also increased $751

million over the three-year period.

Receivables and equipment on operating leases increased by

$482 million in 2009, compared with 2008. Acquisition volumes

of receivables and equipment on operating leases decreased

7 percent in 2009, compared with 2008. The volumes of whole-

sale notes and revolving charge accounts increased approxi-

mately 34 percent and 1 percent, respectively. The volumes

of operating loans, fi nancing leases, retail notes, operating leases

and trade receivables decreased approximately 54 percent,

31 percent, 15 percent, 8 percent and 8 percent, respectively.

At October 31, 2009 and 2008, net receivables and leases

administered, which include receivables administered but not

owned, were $22,729 million and $22,281 million, respectively.

Total external interest-bearing debt of the credit operations

was $20,988 million at the end of 2009, compared with $20,210

million at the end of 2008 and $19,665 million at the end of

2007. Included in this debt are secured borrowings of $3,132

million at the end of 2009, $1,682 million at the end of 2008

and $2,344 million at the end of 2007. Total external borrowings

have increased generally corresponding with the level of the

receivable and lease portfolio, the level of cash and cash equiva-

lents and the change in payables owed to Deere & Company.

The credit operations’ ratio of total interest-bearing debt to total

stockholder’s equity was 7.4 to 1 at the end of 2009, 8.3 to 1 at

the end of 2008 and 8.2 to 1 at the end of 2007.

During 2009, the credit operations issued $4,898 million

and retired $3,755 million of long-term borrowings.

The retirements included $300 million of 6% Notes due 2009

and the remainder consisted primarily of medium-term notes.

Property and equipment cash expenditures for Financial

Services in 2009 were $119 million, compared with $339 million

in 2008, primarily related to investments in wind energy

generation in both years. Capital expenditures for 2010 are

estimated to be approximately $200 million, also primarily

related to investments in wind energy generation.

OFF-BALANCE-SHEET ARRANGEMENTS

The company’s credit operations offer crop insurance products

through managing general agency agreements (Agreements)

with insurance companies (Insurance Carriers) rated “Excellent”

by A.M. Best Company. The credit operations have guaranteed

certain obligations under the Agreements, including the

obligation to pay the Insurance Carriers for any uncollected

premiums. At October 31, 2009, the maximum exposure for

uncollected premiums was approximately $60 million.

Substantially all of the crop insurance risk under the Agreements

have been mitigated by a syndicate of private reinsurance

companies. In the event of a widespread catastrophic crop

failure throughout the U.S. and the default of all the reinsurance

companies on their obligations, the company would be required

to reimburse the Insurance Carriers approximately $981 million

at October 31, 2009. The company believes the likelihood of

this event is substantially remote.

At October 31, 2009, the company had approximately

$170 million of guarantees issued primarily to banks outside the

U.S. related to third-party receivables for the retail fi nancing

of John Deere equipment. The company may recover a portion

of any required payments incurred under these agreements from

repossession of the equipment collateralizing the receivables.

The maximum remaining term of the receivables guaranteed at

October 31, 2009 was approximately six years.

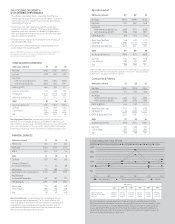

AGGREGATE CONTRACTUAL OBLIGATIONS

The payment schedule for the company’s contractual obligations

at October 31, 2009 in millions of dollars is as follows:

Less More

than 2&3 4&5 than

Total 1 year years years 5 years

Debt*

Equipment Operations ....

$ 3,469 $ 490 $ 173 $ 700 $ 2,106

Financial Services** ....... 20,578 5,090 9,626 3,823 2,039

Total ......................... 24,047 5,580 9,799 4,523 4,145

Interest on debt ................. 4,468 803 1,285 561 1,819

Accounts payable .............. 1,784 1,668 81 31 4

Purchase obligations .......... 2,270 2,242 21 6 1

Operating leases ................ 544 128 180 95 141

Capital leases .................... 56 19 19 4 14

Total ................................ $ 33,169 $ 10,440 $ 11,385 $ 5,220 $ 6,124

* Principal payments.

** Notes payable of $3,132 million classifi ed as short-term on the balance sheet

related to the securitization of retail notes are included in this table based on the

expected payment schedule (see Note 18).

19

18