John Deere 2009 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2009 John Deere annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

16

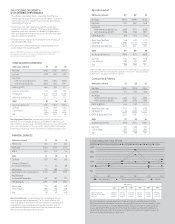

Worldwide Equipment Operations had an operating

profi t of $2,927 million in 2008, compared with $2,318 million

in 2007. Higher operating profi t was primarily due to the

favorable impact of higher shipment volumes and improved

price realization. Partially offsetting these factors were increased

raw material costs, higher selling, administrative and general

expenses, increased research and development costs and

expenses to close a facility in Canada (see Note 5).

The Equipment Operations’ net income was $1,676 million

in 2008, compared with $1,429 million in 2007. The same

operating factors mentioned above as well as a higher effective

tax rate in 2008 affected these results.

Net income of the company’s Financial Services operations

in 2008 decreased to $337 million, compared with $364 million

in 2007. The decrease was primarily a result of increased selling,

administrative and general expenses, an increase in average

leverage and a higher provision for credit losses, partially offset

by growth in the average credit portfolio. Additional information

is presented in the following discussion of the credit operations.

The cost of sales to net sales ratio for 2008 was 75.9 percent,

compared with 75.6 percent in 2007. The increase was primarily

due to higher raw material costs, partially offset by higher sales

and production volumes and improved price realization.

Other income increased in 2008 primarily from increased

crop insurance commissions. Research and development costs

increased in 2008 primarily due to increased spending in support

of new products, Tier 4 emission requirements and the effect of

currency translation. Selling, administrative and general expenses

increased in 2008 primarily due to growth and acquisitions, the

effect of currency translation and the provision for credit losses.

Other operating expenses were higher in 2008 primarily as a

result of higher expenses related to wind energy entities, expenses

from crop insurance, depreciation on operating lease equipment

and foreign exchange losses.

The company has several defi ned benefi t pension plans

and defi ned benefi t health care and life insurance plans.

The company’s postretirement benefi t costs for these plans in

2008 were $277 million, compared with $415 million in 2007.

The long-term expected return on plan assets, which is refl ected

in these costs, was an expected gain of 8.2 percent in 2008 and

8.3 percent in 2007, or $920 million in 2008 and $838 million

in 2007. The actual return was a loss of $2,158 million in 2008

and a gain of $1,503 million in 2007. Total company contribu-

tions to the plans were $431 million in 2008 and $646 million

in 2007, which include direct benefi t payments for unfunded

plans. These contributions also included voluntary contributions

to total plan assets of approximately $297 million in 2008 and

$520 million in 2007.

BUSINESS SEGMENT AND GEOGRAPHIC AREA RESULTS

Worldwide Agriculture and Turf Operations

The agriculture and turf segment had an operating profi t of

$2,461 million in 2008, compared with $1,747 million in 2007.

Net sales increased 28 percent in 2008 due to higher shipment

volumes, the favorable effects of currency translation and

improved price realization. The increase in operating profi t in

2008 was primarily due to higher shipment volumes and

improved price realization, partially offset by higher raw material

costs, increased selling, administrative and general expenses,

higher research and development costs and expenses to close a

facility in Canada.

Worldwide Construction and Forestry Operations

The construction and forestry segment had an operating profi t

of $466 million in 2008, compared with $571 million in 2007.

Net sales decreased 4 percent in 2008 refl ecting the pressure

from U.S. market conditions. The operating profi t was lower in

2008 primarily due to lower shipment volumes and higher raw

material costs, partially offset by improved price realization.

Worldwide Credit Operations

The operating profi t of the credit operations was $478 million

in 2008, compared with $548 million in 2007. The decrease in

operating profi t in 2008 was primarily due to higher selling,

administrative and general expenses, an increase in average

leverage, a higher provision for credit losses and foreign exchange

losses, partially offset by growth in the average credit portfolio

and increased commissions from crop insurance. Total revenues

of the credit operations, including intercompany revenues,

increased 3 percent in 2008, primarily refl ecting the larger

portfolio. The average balance of receivables and leases fi nanced

was 6 percent higher in 2008, compared with 2007. An increase

in average borrowings, offset by lower average interest rates,

resulted in approximately the same interest expense in both

2008 and 2007. The credit operations’ ratio of earnings to fi xed

charges was 1.45 to 1 in 2008, compared with 1.55 to 1 in 2007.

Equipment Operations in U.S. and Canada

The equipment operations in the U.S. and Canada had an

operating profi t of $1,831 million in 2008, compared with

$1,539 million in 2007. The increase was primarily due to

higher shipment volumes and improved price realization,

partially offset by higher raw material costs, increased selling,

administrative and general expenses, higher research and

development costs and expenses to close the previously

mentioned Canadian facility. Net sales increased 9 percent in

2008 due to higher volumes, improved price realization and

the favorable effects of currency translation. The physical

volume increased 4 percent in 2008 excluding acquisitions,

compared with 2007.

15