JP Morgan Chase 2014 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2014 JP Morgan Chase annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

|

|

1313

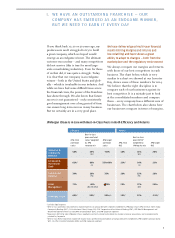

I. AN OUTSTANDING FRANCHISE

bonds to assist municipalities and hospitals,

and green bonds to finance environmentally

beneficial projects such as green buildings,

clean water and renewable energy. As a firm,

we spend approximately $700 million a year

on research so that we can educate investors,

institutions and governments about econo-

mies, markets and companies. The needs of

these clients will be met – one way or another

– by large financial institutions that can bear

the costs and risks involved. Simply put, if

it is not done by a large American financial

institution, it will be done by a large non-

American financial institution.

Regional and community banks are critical

to their communities — in fact, we are a huge

supporter and their largest banking partner.

These banks are deeply embedded in their

communities, many of which are not served

by larger banks. They have an intimate

knowledge of the local economy and local

small businesses, which allows them to cost-

eectively serve those clients. JPMorgan

Chase, as a traditional “money center bank”

and “bankers’ bank,” in fact, is the largest

banker in America to regional and commu-

nity banks. We provide them with many

services so they can continue to serve their

clients. For example, we directly lend to

them, we process payments for them, we

finance some of their mortgage activities, we

raise capital for them (both debt and equity),

we advise them on acquisitions, and we buy

and sell securities for them. We also provide

them with interest rate swaps and foreign

exchange both for themselves – to help them

hedge some of their exposures – and for

their clients.

However, large does not necessarily mean

complex (and things should be complex only

for a good reason)

Many of the activities we do that are consid-

ered large are easy to understand. All of our

5,600 Chase consumer branches do essen-

tially the same thing, and many of our large

global transactions are not any more compli-

cated than a loan for a middle market client.

While we agree with the concept that you

should keep things as simple as possible,

some things, by their very nature, are more

complex. And that complexity cannot be

reduced by wishful thinking. In fact, basic

lending, whether to a large company or

a midsized company, is one of the more

complex things we do because one must

understand the economy, the nature of

the business and often the types of collat-

eral involved. There are many judgmental

factors to consider as well, which might

include the character of the borrower, the

growth prospects of the business, and an

understanding of the products and services

and technology of the business.

There are understandable questions about

the role that large financial institutions

play. Some of these questions make people

nervous, in part because they do not under-

stand the larger picture. These are important

questions, and we always are willing to help

explain what we do and why we do it. Taken

in small component pieces, these activities

generally are easier to understand. While

some may criticize a bank’s activities instead

of taking the time to understand them, this

does not contribute to a genuinely construc-

tive dialogue around the role of banks.

People also should ask themselves one

basic question: Why do banks oer these

services? The fact is, almost everything we

do is because clients want and need our

various and sometimes complex services.

(We do many activities that are ancillary to

clients’ direct needs, but we must do these

things to provide clients with what they

need. For example, in order to support our

operation, we run global data centers, we

hedge our own exposures and we maintain

liquid pools of investments.)

I would venture to say that banking is not

as complex as making airplanes, discovering

eective pharmaceuticals, building safe

cars, developing innovative electronics and,

of course, understanding nuclear physics.

There are huge benefits to the complexity

involved in those other industries – but there

also are sometimes negative consequences.

The question for society is: Are we, in total,