JP Morgan Chase 2003 Annual Report Download - page 6

Download and view the complete annual report

Please find page 6 of the 2003 JP Morgan Chase annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

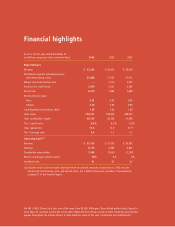

4J.P. Morgan Chase & Co. / 2003 Annual Report

I believe that a high-performance culture is the critical differentiator

that separates the great enterprises from those that are merely good,

and that separates enduring success from transitory achievement.

We remain committed to extending those leadership positions. Two

recent acquisitions – an electronic payments subsidiary of Citigroup and

Bank One’s corporate trust business – are expected to enhance consid-

erably TSS’s revenue growth rate in 2004. (It is important to note that

Bank One sold its trust business because it lacked the scale and global

scope that JPMorgan Chase has in this business.) TSS will continue

to drive for greater scale, productivity gains and higher service quality

levels to maintain its market leadership.

Investment M anagement & Private Banking (IMPB) showed

strong momentum in 2003, generating earnings of $268 million. Pre-tax

margins improved significantly throughout the year and assets under

supervision increased 18% to $758 billion. During the year, IMPB made

substantial progress in its execution on three key goals. Investment

performance improved, particularly in key U.S. institutional equity and

fixed income products. The Private Bank successfully executed its

growth strategy as client assets and product usage increased year over

year. Additionally, credit costs were lowered by nearly 60% compared

to 2002. And lastly, IMPB advanced its U.S. retail strategy by acquiring

full ownership of J.P. Morgan | American Century Retirement Plan

Services with $41 billion in 401(k) plan assets. Aligning Retirement Plan

Services and BrownCo, our online brokerage service, to build an IRA

roll-over capability positions IMPB well to benefit from the growing

individual retirement market.

JPMorgan Partners (JPMP), our private equity business, has invested

in a wide range of companies in diverse sectors, stages and locations.

JPMP’s primary investment vehicle is its $6.5 billion Global Fund, which

invests on behalf of the firm and third-party investors. JPMP’s financial

performance improved substantially over the year. In 2004 and beyond,

JPMP should benefit from a continued recovery in equity financing

and M&A activities.

Chase Financial Services (CFS), our retail and middle market

businesses, improved upon their very strong 2002 results with record

revenues and earnings in 2003, producing an ROE of 28% .

As the result of its focus on national consumer credit businesses, CFS

has established a unique franchise that has enabled it to deliver strong

results. It is a market leader in all three major national consumer credit

businesses – the only top-five performer across mortgage origination

and servicing, credit cards and auto finance.

Chase Home Finance had a record year in 2003, coming off excellent

results in 2002. On all fronts, Home Finance took advantage of the

mortgage boom, resulting in an increase in revenues of 38% over

2002. The quality of execution was key to its success, as the business

managed record volumes while maintaining high customer service

standards. Chase Cardmember Services grew outstandings despite

balance paydowns due to consumer liquidity resulting from the mortgage

refinancing boom. Chase Auto Finance also had a record number of

originations and increased its market share.

In addition to our national consumer credit businesses, our other CFS

businesses – Chase Regional Banking and Chase Middle Market – have

shown significant growth in deposits, up 8% and 17% respectively,

despite the low interest rate environment, which compressed spreads,

reducing revenue for the year.

In the still fragmented retail banking industry, CFS’s businesses focused

on competitive differentiators, such as productivity and marketing

enhancements. We have seen gains from disciplined expense manage-

ment and from greater efficiency. CFS has also boosted the quality of

its marketing efforts, resulting in progress in cross-selling products

and services. We invested in businesses such as home equity, where we

achieved significant increases in outstandings. Personal Financial

Services, our branch-based business offering banking and investing services

to upper-tier retail customers, continues to gain momentum, having

increased new investment fee-based sales by 63% and bringing assets

under management to a total of $10.7 billion.

In 2004, CFS expects to operate at lower but still robust ROE levels,

caused by our expectation that the mortgage business will return to

more normal conditions. CFS will focus on stable credit quality,

productivity gains, innovative marketing and cross-selling initiatives,

and continued investment in growth opportunities to improve its

competitive position.

Disciplined risk management

The improvement in our performance was enhanced by better execution

in risk management.

In the two years following the merger that created JPMorgan Chase

(that is, in 2001 and 2002), our performance suffered from three main

challenges, none of them principally related to the merger: excessive

capital committed to private equity; over-concentration of loans to

telecommunications companies; and large exposure to Enron.

We dealt decisively with each issue in 2003. We reduced our exposure

to private equity to 15% of the firm’s common stockholders’ equity

at the end of 2003 (down from a peak of 29% in 2000). We moved

to put Enron behind us through the settlement that our firm and

others reached in 2003 with the Securities and Exchange Commission

and other regulatory and governmental entities. We reduced commercial

credit exposure and drove substantial reductions in single-name and

industry concentrations.