Ingram Micro 2011 Annual Report Download - page 4

Download and view the complete annual report

Please find page 4 of the 2011 Ingram Micro annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

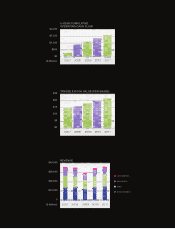

Our excellent balance-sheet management contin-

ued into 2011, and we once again increased our

asset base, exiting the year with a tangible book

value in excess of $21 per share. The year-end

cash balance was $891 million after investments in

multiple growth initiatives, a meaningful reduction

in our outstanding debt and repurchases of 12.5

million shares of stock for $226 million. We had solid

cash ow from operations of $296 million for the

year, bringing our ve-year cumulative cash genera-

tion from operations to more than $1.5 billion, while

collaborative efforts worldwide maintained work-

ing capital days at 22, at the low end of our target

range of 22–26 days. Full-year return on invested

capital was 10.4 percent, exceeding our estimated

weighted average cost of capital of approximately

9 percent.

THE INFRASTRUCTURE: LAYING THE FOUNDATION

As the company continues to evolve as a global

organization, the need for modern, consistent

systems becomes critical. For most of our history

we’ve operated on a semi-proprietary ERP system

with functionality that varied from country to coun-

try. This system is becoming costly to maintain

and incompatible with our future needs and stra-

tegic initiatives, so we are transitioning to a new

enterprise system that will improve our operations

through more nimble access to information, greater

scalability and automation and enhanced standard-

ization and productivity.

In February 2011, we began our system conversion

in Australia. While not our rst migration, it was the

rst to involve our proprietary warehouse manage-

ment system reserved for our largest and most

sophisticated distribution centers. During the imple-

mentation, we encountered dif culties connecting to

our warehouse system, which created order ful ll-

ment and inventory complications. Furthermore, the

ramp-up of effective customer interfaces and order

processing did not run as smoothly as planned in

Australia, which is a more complex and competitive

environment than the other countries we had previ-

ously migrated. As a result, the Australian opera-

tion experienced revenue and pro t declines that

affected the company’s overall performance. While

the connectivity issues have been resolved, into

early 2012 we are continuing to focus on improving

the customer service and order management func-

tionality to better meet our customers’ needs, which

in turn will help us regain market share and provide

the superior customer service for which

we are known.

In our efforts to embrace one world as one

company, we successfully pursued other technol-

ogy improvements that are expected to generate

long-term value. We consolidated and modernized

our data centers in three strategic locations—

Chicago, Singapore and Frankfurt—and have begun

to update our Web systems to improve the online

customer experience.

THE BUSINESS: ESSENTIAL ELEMENTS

Our investments in technology, as well as other

business enhancements, are designed with our

partners—both resellers and vendors—in mind.

During 2011, our commitment to partners was

evident through exclusive vendor agreements,

expanded portfolios of products and services,

and innovative capabilities to capture new

market opportunities.

We kicked off the year with two new exclusive

vendor agreements in the consumer electronics

space, setting the stage for similar agreements in

enterprise, software and services. The year ended

with our skilled management through the global

shortages of hard disk drive inventory. Devastating

ooding in Thailand constrained the supply of disk

drives, but we were able to provide a steady stream

to help serve the needs of our partners, which also

helped drive strong pro ts to close out the year.

Throughout 2011, our operations delivered achieve-

ments that lifted us above the economic and

geographic challenges of the year. In North America,

the region realigned resources into distinct business

units, fostering expertise within fast-growing, higher-

margin specialty areas. The region attracted dozens

of new vendors, signi cantly improved its customer

service statistics and delivered nancial results near

decade highs.

Our European region delivered solid results within a

challenging macro-economic environment plagued

with sovereign debt troubles and high unemployment.

The region proactively pursued small and midsize

business (SMB) accounts to spark further growth in

the commercial segment, which helped offset weak

consumer demand. Operations in the three anchor

countries—Germany, France and the United King-

dom—held up well. The region also continued to

build higher-margin specialty areas such as enterprise,

logistics and data capture/point of sale (DC/POS).