HSBC 2003 Annual Report Download - page 353

Download and view the complete annual report

Please find page 353 of the 2003 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

343 -

344

344 -

345

345 -

346

346 -

347

347 -

348

348 -

349

349 -

350

350 -

351

351 -

352

352 -

353

353 -

354

354 -

355

355 -

356

356 -

357

357 -

358

358 -

359

359 -

360

360 -

361

361 -

362

362 -

363

363 -

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

|

|

351

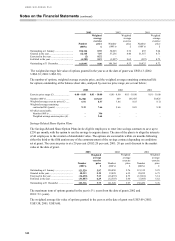

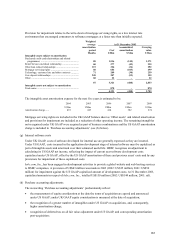

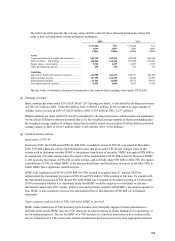

Provision for impairment relates to the write-down of mortgage servicing rights, as a low interest rate

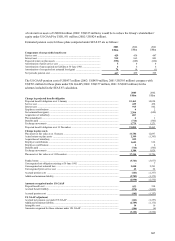

environment has encouraged consumers to refinance mortgages at a faster rate than initially expected.

Weighted

average At 31 December 2003

amortisation Accumulated Carrying

period Cost amortisation value

Months US$m US$m US$m

Intangible assets subject to amortisation

Purchased credit card relationships and related

programmes ............................................................. 80 1,516 (145) 1,371

Retail Services merchant relationship .......................... 60 277 (42) 235

Other loan related relationships .................................... 115 326 (34) 292

Mortgage servicing rights ............................................. 60 684 (185) 499

Technology, customer lists and other contracts ............ 71 289 (30) 259

Core deposit relationships ............................................ 240 207 (52) 155

Other ............................................................................ 60 22 – 22

87 3,321 (488) 2,833

Intangible assets not subject to amortisation

Trade name ................................................................... 870 – 870

4,191 (488) 3,703

The intangible asset amortisation expense for the next five years is estimated to be:

2004 2005 2006 2007 2008

US$m US$m US$m US$m US$m

Amortisation charge...... 491 445 414 382 274

Mortgage servicing rights are included in the UK GAAP balance sheet as ‘Other assets’ and related amortisation

and provisions for impairment are included as a reduction of other operating income. The remaining intangibles

not recognised under UK GAAP were acquired as part of business combinations and the US GAAP amortisation

charge is included in ‘Purchase accounting adjustments’ (see (h) below).

(g) Internal software costs

Under UK GAAP, costs of software developed for internal use are generally expensed as they are incurred.

Under US GAAP, costs incurred in the application development stage of internal software must be capitalised as

part of intangible assets and amortised over their estimated useful life. HSBC recognises an adjustment in

calculating its US GAAP net income, reflecting the impact of current year software development costs

capitalised under US GAAP, offset by the US GAAP amortisation of these and previous years’ costs and by any

provisions for impairment of these capitalised costs.

hsbc.com, Inc., has been engaged in development activities to provide a global website and web hosting services

to HSBC companies. A provision of US$43 million was made in 2003 (2002: US$35 million; 2001: US$50

million) for impairment against the US GAAP capitalised amount of development costs. At 31 December 2003,

capitalised amounts in respect of hsbc.com, Inc., totalled US$150 million (2002: US$144 million; 2001: nil).

(h) Purchase accounting adjustments

The reconciling ‘Purchase accounting adjustments’ predominantly reflect:

• the measurement of equity consideration at the date the terms of acquisition are agreed and announced

under US GAAP; under UK GAAP equity consideration is measured at the date of acquisition;

• the recognition of a greater number of intangibles under US GAAP on acquisitions, and, consequently,

higher amortisation charge;

• recognition of deferred tax on all fair value adjustment under US GAAP, and corresponding amortisation

post-acquisition;