Freeport-McMoRan 2009 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 2009 Freeport-McMoRan annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

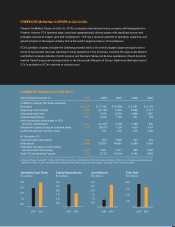

For 2010, FCX expects South America sales to approximate 1.3 billion pounds of copper and

100,000 ounces of gold. South America unit net cash costs, including by-product credits (gold and

molybdenum) averaged $1.12 per pound in 2009 and $1.14 per pound in 2008. South America

unit net cash costs were slightly lower in 2009 because of lower input costs, primarily for energy.

Assuming achievement of current sales estimates and estimates for commodity-based input

costs, FCX estimates that average unit net cash costs, including gold and molybdenum credits,

for its South America copper mines would approximate $1.20 per pound of copper in 2010.

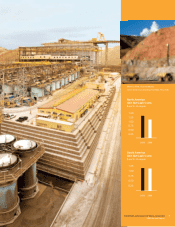

FCX has resumed construction activities associated with the development of a large sulde

ore deposit at El Abra. The project, which was deferred in late 2008 as a result of market

conditions, will extend El Abra’s mine life by over 10 years. FCX has also commenced a

project to optimize throughput at the existing Cerro Verde concentrator, which is designed

to add 30 million pounds of additional copper production per year by increasing mill

throughput from 108,000 metric tons of ore per day to 120,000 metric tons of ore per day.

Indonesia

FCX operates the world’s largest single reserve of both copper and gold through its subsidiary,

PT Freeport Indonesia, in the Grasberg minerals district in Papua, Indonesia. For 2009,

consolidated sales from FCX’s Indonesia operations totaled 1.4 billion pounds of copper at

an average realized price of $2.65 per pound and 2.5 million ounces of gold at an average

realized price of $994 per ounce. For 2008, consolidated sales totaled 1.1 billion pounds of

copper at an average realized price of $2.36 per pound and 1.2 million ounces of gold at an

average realized price of $861 per ounce. Production and sales volumes were signicantly

higher in 2009 because of sequencing in mining areas with varying ore grades, which

resulted in mining higher grade sections of the Grasberg open pit during 2009. FCX expects

Indonesia sales to approximate 1.2 billion pounds of copper and 1.7 million ounces of gold

in 2010, as production transitions to a lower grade section of the Grasberg open pit.

PT Freeport Indonesia unit net cash costs, including gold and silver credits, averaged a

net credit of $0.49 per pound of copper in 2009, compared with a net cost of $0.96 per

pound in 2008. The lower unit net cash costs in 2009 primarily reected higher gold credits

resulting from higher gold sales volumes and prices, as well as signicantly higher copper

sales volumes and lower commodity-based input costs. Assuming achievement of current

2010 sales volumes estimates, average gold prices of $1,100 per ounce in 2010 and current

estimates for energy costs, currency exchange rates and other cost factors, FCX estimates

that average unit net costs for PT Freeport Indonesia would approximate $0.21 per pound

of copper in 2010. Unit net cash costs are expected to be higher in 2010 than the prior year

primarily because of lower projected sales volumes and higher commodity-based input costs.

PT Freeport Indonesia is pursuing several capital projects in the Grasberg minerals district,

including development of the large-scale, high-grade underground ore bodies located beneath

and adjacent to the Grasberg open pit. These projects include continued development of the

Common Infrastructure project, the Grasberg Block Cave and the Big Gossan underground

mines, and future development of the Deep Mill Level Zone underground mine.

9

FREEPORT-McMoRan COPPER & GOLD INC.

2009 Annual Report