First Data 2007 Annual Report Download - page 10

Download and view the complete annual report

Please find page 10 of the 2007 First Data annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

|

|

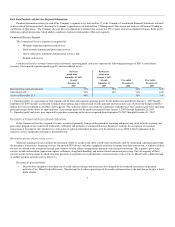

Financial Institution Services revenues from external customers, operating profit, and assets represent the following percentages of FDC's consolidated

revenues, total reported segment operating profit and consolidated assets:

Successor

period from

September 25, 2007

through

December 31,

2007

Predecessor

period from

January 1, 2007

through

September 24,

2007

Year ended

December 31,

2006

Year ended

December 31,

2005

Revenue from external customers 23% 25% 25% 28%

Operating profit 1, 2 27% 32% 24% 27%

Assets (at December 31)2 11% 7% 7%

1 – Operating profit, as a percentage of total segment and all other and corporate operating profit, for the predecessor period from January 1, 2007 through

September 24, 2007 includes accelerated vesting of stock options and restricted stock awards and units and transaction costs related to the merger of $265.2

million that were recognized in All Other and Corporate. The exclusion of these costs from the calculation would decrease Financial Institution Services

operating profit percentage shown above by approximately 8 percentage points for the predecessor period from January 1, 2007 through September 24, 2007.

2 – Operating profit and assets were impacted by purchase accounting in the successor period from September 25, 2007 through December 31, 2007.

Description of Financial Institution Services Segment Operations

Financial Institution Services provides financial institutions and other third parties with various services including credit and retail card processing;

debit card processing and network services; output services, such as statement and letter printing, embossing and mailing services; and remittance and other

processing services. Revenue and profit growth in these businesses is derived from growing the core business, expanding product offerings, and improving the

overall cost structure. Growing the core business comes primarily from an increase in debit and credit card usage, growth from existing clients and sales to

new clients and the related account conversions.

Growth from expanded product offerings is driven by the development or acquisition of new products as well as expansion into adjacent markets. The

Company will enter adjacent markets where it can leverage its existing infrastructure and core competencies around high volume transaction processing and

management of customer account information.

The Company has relationships and many long-term customer contracts with card issuers providing credit and retail card processing, output services for

printing and embossing items, as well as debit card processing services and the STAR Network. These contracts generally require a notice period prior to the

end of the contract if a client chooses not to renew and some contracts may allow for early termination upon the occurrence of certain events such as a change

in control. The termination fees paid upon the occurrence of such events are designed primarily to cover balance sheet exposure related to items such as

capitalized conversion costs or signing bonuses associated with the contract; and in some cases, may cover a portion of lost future revenue and profit.

Although these contracts may be terminated upon certain occurrences, the contracts provide the segment with a steady revenue stream since a vast majority of

the contracts are honored through the contracted expiration date.

Credit and retail card issuing and processing services

Credit and retail card issuing and processing services provide outsourcing services to financial institutions and other issuers of cards, such as consumer

finance companies. Financial institution clients include a wide variety of banks, savings and loan associations, group service providers and credit unions.

Services provided include, among other things, account maintenance, transaction authorizing and posting, fraud and risk management services and settlement.

The Company provides a full array of services throughout the period of each card's use, starting from the moment a card-issuing client processes an

application for a card. The basic services may include processing the card application, initiating service for the cardholder, processing each card transaction

for the issuing retailer or financial institution and accumulating the card's transactions. The Company's fraud management services monitor the unauthorized

use of cards which have been reported to be lost, stolen, or which exceed credit limits. The Company's fraud detection systems help identify fraudulent

transactions by monitoring each cardholder's purchasing patterns and flagging unusual purchases. Other services provided include customized

communications to cardholders, information verification associated with granting credit, debt collection, and customer service.

Revenues for credit and retail card issuing and processing services are derived from fees payable under contracts that depend primarily on the number

of cardholder accounts on file. More revenue is derived from active accounts (those accounts on file that had a balance or any monetary posting or

authorization activity during the month) than inactive accounts.

9