Dollar General 2010 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2010 Dollar General annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

10-K

The Dollar General Store

The average Dollar General store has approximately 7,200 square feet of selling space and is

typically operated by a manager, an assistant manager and three or more sales clerks. Approximately

58% of our stores are in freestanding buildings, 41% in strip shopping centers and 1% are in

downtown buildings. Most of our customers live within three to five miles, or a 10 minute drive, of our

stores. Our store strategy features low initial capital expenditures, limited maintenance capital, low

occupancy and operating costs, and a focused merchandise offering within a broad range of categories,

allowing us to deliver low retail prices while generating strong cash flows and investment returns. In

2010, the average cost of equipment and fixtures in our leased stores was approximately $165,000.

Initial inventory, net of payables, increases the investment in a new store by approximately $75,000.

We generally have not encountered difficulty locating suitable store sites in the past. Given the size

of the communities that we target, we believe that there is ample opportunity for new store growth in

existing and new markets. In addition, the current real estate market is providing an opportunity for us

to access higher quality sites at lower rates than in recent years. Also, we believe we have significant

opportunities available for our relocation and remodel programs. We spend approximately $75,000 for

equipment and fixtures to remodel a store and approximately $140,000 to relocate one. We remodeled

or relocated 504 stores in 2010, 450 in 2009 and 404 in 2008.

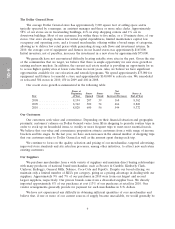

Our recent store growth is summarized in the following table:

Stores at Net

Beginning Stores Stores Store Stores at

Year of Year Opened Closed Increase/(Decrease) End of Year

2008 ................. 8,194 207 39 168 8,362

2009 ................. 8,362 500 34 466 8,828

2010 ................. 8,828 600 56 544 9,372

Our Customers

Our customers seek value and convenience. Depending on their financial situation and geographic

proximity, customers’ reliance on Dollar General varies from fill-in shopping to periodic routine trips in

order to stock up on household items, to weekly or more frequent trips to meet most essential needs.

We believe that our value and convenience proposition attracts customers from a wide range of income

brackets and life stages. In the last year, we have seen increases in the annual number of shopping trips

that our customers make to Dollar General as well as the amount spent during each trip.

We continue to focus on the quality, selection and pricing of our merchandise, targeted advertising,

improved store standards and site selection processes, among other initiatives, to attract new and retain

existing customers.

Our Suppliers

We purchase merchandise from a wide variety of suppliers and maintain direct buying relationships

with many producers of national brand merchandise, such as Procter & Gamble, Kimberly Clark,

Unilever, Kellogg’s, General Mills, Nabisco, Coca-Cola and PepsiCo. Despite our broad offering, we

maintain only a limited number of SKUs per category, giving us a pricing advantage in dealing with our

suppliers. Approximately 9% and 7% of our purchases in 2010 were from our largest and second

largest suppliers, respectively. Our private brands come from a diversified supplier base. We directly

imported approximately 8% of our purchases at cost (13% of our purchases at retail) in 2010. Our

vendor arrangements generally provide for payment for such merchandise in U.S. dollars.

We have not experienced any difficulty in obtaining sufficient quantities of core merchandise and

believe that, if one or more of our current sources of supply became unavailable, we would generally be

6