Comfort Inn 2003 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2003 Comfort Inn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

|

|

or which declined to formalize a franchise relationship following the Company’s acquisition of a controlling

interest in Flag Choice Hotels during 2002. As of December 31, 2002, the Company had 310 franchised hotels

with 23,766 rooms either in design or under construction in its domestic system. The Company had an additional

164 franchised hotels with 17,799 rooms under development in its international system as of December 31, 2002.

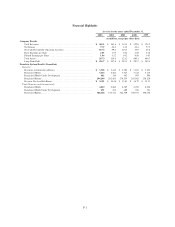

Franchise Expenses. The cost to operate the franchising business is reflected in selling, general and

administrative expenses. Selling, general and administrative expenses were $56.5 million (including restructuring

charges of $1.6 million) for the year ended December 31, 2002, a decrease of $5.5 million from the year ended

December 31, 2001 total of $62.0 million (including restructuring charges of $5.9 million). As a percentage of

net franchise revenues, selling, general and administrative expenses declined to 32.8% in 2002 from 36.5% in

2001. This decline, which increased franchising margins from 63.5% to 67.2%, was largely due to a $4.3 million

reduction in restructuring charges incurred in 2002 compared to 2001.

Marketing and Reservations. Total marketing and reservation revenues were $190.1 million and $168.2

million for the years ended December 31, 2002 and 2001, respectively. Depreciation and amortization

attributable to marketing and reservation activities was $13.0 million and $11.8 million for the years ended

December 31, 2002 and 2001, respectively. Interest expense attributable to reservation activities was $1.4 million

and $2.0 million for the years ended December 31, 2002 and 2001, respectively. Marketing and reservation

activities provided a positive cash flow of $17.2 million and $20.3 million for the years ended December 31,

2002 and 2001, respectively. As of December 31, 2002 and 2001, the Company’s balance sheet included a

receivable of $44.9 million and $49.4 million, respectively, for marketing and reservation fees. The Company has

the contractual authority to require that the franchisees in the system at any given point repay the Company for

any deficits related to marketing and reservation activities. The Company’s current franchisees are legally

obliged to pay any assessment the Company imposes on its franchisees to obtain reimbursement of such deficit

regardless of whether those constituents continue to generate gross room revenue. The Company has no present

intention to accelerate repayment of the deficit from current franchisees.

Depreciation and Amortization. Depreciation and amortization decreased to $11.3 million in the year ended

December 31, 2002 from $12.5 million in the year ended December 31, 2001. This decrease is primarily

attributable to the Company’s adoption of Statement of Financial Accounting Standards No. 142, “Goodwill and

Other Intangible Assets,” pursuant to which the Company stopped amortizing goodwill effective January 1, 2002.

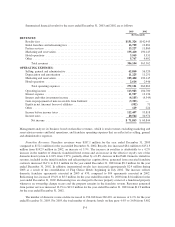

Friendly. The Company’s entire investment in Friendly was written off in 2001; accordingly, the

Company’s 2002 results of operations do not include any equity method losses or other amounts related to

Friendly. In addition to the $22.7 million impairment described below, the Company recorded equity method

losses associated with its investment in Friendly totaling $10.3 million (net of taxes) for the year ended

December 31, 2001.

On February 21, 2002, Friendly announced that it had been unable to find an acceptable buyer for its

business and would terminate such efforts to sell its business. Given this termination and the adverse economic

conditions of Friendly, the Company disposed of its entire investment in Friendly on March 20, 2002. The

Company wrote-off its entire investment in Friendly through a $22.7 million charge to reflect the permanent

impairment of this asset as of December 31, 2001.

Interest and Other. Interest expense of $13.1 million in the year ended December 31, 2002 is down $2.3

million from $15.4 million in the year ended December 31, 2001 due primarily to lower effective interest rates.

The Company’s weighted average interest rate as of December 31, 2002 was 4.39% compared to 4.52% as of

December 31, 2001. Included in the results for 2002 and 2001 is approximately $4.6 million and $4.2 million,

respectively, of interest income earned on the note receivable from Sunburst. The note from Sunburst accrued

interest up until June 2002, at which point interest became payable semi-annually in arrears. As of December 31,

2002, the Company’s balance sheet included an interest receivable from Sunburst of $2.3 million which is

included in other current assets in the accompanying consolidated balance sheets and was paid to the Company

by Sunburst in January 2003.

F-7