Bank of the West 2006 Annual Report Download - page 4

Download and view the complete annual report

Please find page 4 of the 2006 Bank of the West annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

|

|

Letter from the

C H A I R M A N

2

Relationship banking is the focus of our report this year,

and it has been at the core of our successful growth since

our founding as a community bank over 130 years ago.

In 2006, we completed the migration of our relationship

model into the 200-plus branches of the former

Commercial Federal Bank acquired in December, 2005.

That successful integration, and customer growth across

our network, served to increase earnings 9% over 2005,

despite narrowing interest rate margins and intense

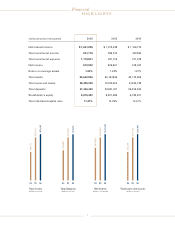

competition for deposits. Bank of the West had net income

of $572.0 million for the year, up from the 2005 net of

$525.7 million. Our deposits at December 31, 2006 were

$37.4 billion, and loans and leases totaled $39.5 billion.

Year end assets for the bank were $55.6 billion.

Now among the largest commercial banks in the U.S., Bank

of the West faces complexities of scale that could present

an obstacle to our highly successful customer-focused

strategy. We offer high-touch, community-bank service

with the full product set customers expect from a large

financial institution. But we don’t want to risk becoming

yet another huge, impersonal organization. To keep our

strategy viable, we began last year to make structural and

organizational changes, to make relationship banking

truly scalable across a footprint of 19 states and more than

700 branch and commercial locations.

A N E W A P P R O A C H

Our challenge is to leverage the value of a much larger

franchise and more comprehensive product line, while

ensuring that size and scope don’t disrupt our personalized

style of customer service. To do this, we launched a new

bank-wide operating model last June that enables us to

offer a uniform set of products to our entire customer base.

We call it, not too surprisingly, the B.E.A.R. Plan, an

acronym for Business Empowerment to Achieve Results.

The B.E.A.R. model brings decision-making closer to our

customers through decentralization, with geographic

division executives exercising a substantial degree of

local operational and credit autonomy in eight regional

centers: Albuquerque, Denver, Fargo, Los Angeles, Omaha,

Portland, Sacramento, and San Francisco. We have also

located representatives of our major product lines in

each regional center, working closely with relationship

managers to provide SBA credit, cash management,

equipment financing, foreign exchange, trade finance and

other services.

Our larger scale allows us to be a more effective

commercial competitor. By deploying commercial banking

employees regionally, segmented in accord with the size

and scope of our 164,000 business clients, we can provide

faster, better-tailored decisions and counsel. A newly-

created National Banking Division is opening new offices to