Aarons 1997 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 1997 Aarons annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14

|

|

At December 31, 1997 and 1996, and for the Years Ended

December 31, 1997 and 1996, and the Nine Months Ended

December 31, 1995.

Note A: Summary of Significant

Accounting Policies

Principles of Consolidation —The consolidated financial

statements include the accounts of Aaron Rents, Inc. and its

wholly-owned subsidiary, Aaron Investment Company (the

Company). All significant intercompany accounts and trans-

actions have been eliminated. The preparation of the

Company’s consolidated financial statements in conformity

with generally accepted accounting principles requires man-

agement to make estimates and assumptions that affect the

amounts reported in these financial statements and accompa-

nying notes. Actual results could differ from those estimates.

Line of Business—The Company is engaged in the business

of renting and selling residential and office furniture and other

merchandise throughout the U.S. The Company manufac-

tures furniture principally for its rental and sales operations.

Rental Merchandise consists primarily of residential and

office furniture, consumer electronics and other merchandise

and is recorded at cost. Prior to January 1, 1996, depreciation

was provided using the straight-line method over the esti-

mated useful life of the merchandise, principally from 1 to 5

years, after allowing for a salvage value of 5% to 60%.

Effective January 1, 1996, the Company prospectively

changed its depreciation method on merchandise in the

rental purchase division acquired after December 31, 1995,

from generally 14 months straight-line with a 5% salvage

value to a method that depreciates the merchandise over the

agreement period, generally 12 months, when on rent, and

36 months, when not on rent, to a 0% salvage value. This new

method is similar to a method referred to as the income fore-

casting method in the rental purchase industry. The

Company adopted the new method because management

believes that it provides a more systematic and rational allo-

cation of the cost of rental purchase merchandise over its

useful life. The effect for the year ended December 31, 1996

of the change in the depreciation method on merchandise

purchased after December 31, 1995 was to decrease net

income by approximately $850,000 ($.04 per share). In

addition, based on an analysis of the average composite life of

the division’s rental purchase merchandise on rent or on

hand at December 31, 1995, the Company extended the

depreciable lives of that merchandise from generally 14

months to 18 months, and made other refinements to depre-

ciation rates on rental and rental purchase merchandise. The

effect of such change in depreciable lives and other refine-

ments was to increase net income for the year ended

December 31, 1996 by approximately $709,000 ($.04 per

share). The Company recognizes rental revenues over the

rental period and recognizes all costs of servicing and main-

taining merchandise on rent as incurred.

Property, Plant and Equipment are recorded at cost.

Depreciation and amortization are computed on a straight-

line basis over the estimated useful lives of the respective

assets, which are from 8 to 27 years for buildings and

improvements and from 2 to 5 years for other depreciable

property and equipment. Gains and losses related to disposi-

tions and retirements are included in income. Maintenance

and repairs are charged to income as incurred; renewals and

betterments are capitalized. The Company adopted

Statement of Financial Accounting Standards No. 121,

“Accounting for the Impairment of Long-Lived Assets and for

Long-Lived Assets to be Disposed Of”(SFAS 121), in the first

quarter of 1996. The effect of the adoption was not material.

Deferred Income Taxes are provided for temporary differ-

ences between the amounts of assets and liabilities for finan-

cial and tax reporting purposes. Such temporary differences

arise principally from the use of accelerated depreciation

methods on rental merchandise for tax purposes.

Cost of Sales includes the depreciated cost of rental return

residential and office merchandise sold and the cost of new

residential and office merchandise sold. It is not practicable

to allocate operating expenses between selling and rental

operations.

Advertising—The Company expenses advertising costs as

incurred. Such costs aggregated $9,530,000 in 1997,

$10,422,000 in 1996, and $6,258,000 for the nine months

ended December 31, 1995.

Stock Based Compensation —The Company has elected to

follow Accounting Principles Board Opinion No. 25,

“Accounting for Stock Issued to Employees”(APB 25) and

related Interpretations in accounting for its employee stock

options and adopted the disclosure-only provisions of

Statement of Financial Accounting Standards No. 123,

“Accounting for Stock Based Compensation”(FAS 123). The

Company grants stock options for a fixed number of shares

to employees with an exercise price equal to the fair value of

the shares at the date of grant and, accordingly, recognizes no

compensation expense for the stock option grants.

Excess Costs over Net Assets Acquired —Goodwill is amor-

tized on a straight-line basis over a period of twenty years.

Long-lived assets, including goodwill, are periodically

reviewed for impairment based on an assessment of future

operations. The Company records impairment losses on long-

lived assets used in operations when indicators of impair-

ment are present and the undiscounted cash flows estimated

to be generated by those assets are less than the assets’

carrying amount.

19

Notes to Consolidated

Financial Statements

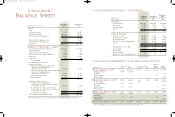

Nine

Year Ended Year Ended Months Ended

December 31, December 31, December 31,

(In Thousands) 1997 1996 1995

Operating Activities

Net Earnings $ 18,396 $ 15,393 $ 9,880

Depreciation & Amortization 77,487 70,693 45,798

Deferred Income Taxes 3,805 (899) (345)

Change in Accounts Payable &

Accrued Expenses 5,103 5,695 242

Change in Accounts Receivable (1,083) (2,339) 255

Other Changes, Net 1,587 982 (711)

Cash Provided by Operating Activities 105,295 89,525 55,119

Investing Activities

Additions to Property, Plant & Equipment (15,165) (17,534) (5,476)

Book Value of Property Retired or Sold 6,531 1,823 1,979

Additions to Rental Merchandise (145,262) (137,023) (72,926)

Book Value of Rental Merchandise Sold 58,436 48,352 30,892

Contracts & O ther Assets Acquired (21,665) (3,891) (533)

Cash Used by Investing Activities (117,125) (108,273) (46,064)

Financing Activities

Proceeds from Revolving Credit Agreement 118,545 85,299 51,933

Repayments on Revolving Credit Agreement (97,766) (67,434) (56,845)

Increase (Decrease) in Other Debt 342 21 (768)

Dividends Paid (761) (765) (367)

Acquisition of Treasury Stock (8,918) (2,889) (3,134)

Issuance of Stock Under Stock Option Plan 400 4,502 129

Cash Provided (Used) by Financing Activities 11,842 18,734 (9,052)

Increase (Decrease) in Cash 12 (14) 3

Cash at Beginning of Year 84 98 95

Cash at End of Year $ 96 $ 84 $ 98

Cash Paid During the Year:

Interest $ 3,713 $ 3,384 $ 2,642

Income Taxes 6,989 7,531 7,677

The accompanying notes are an integral part of the Consolidated Financial Statements.

18

Consolidated

Statements of Cash Flows

AR layout Final.wpc 4/24/98 8:24 AM Page 21