3M 2012 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2012 3M annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

57

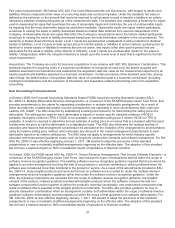

Fair value measurements: 3M follows ASC 820, Fair Value Measurements and Disclosures, with respect to assets and

liabilities that are measured at fair value on a recurring basis and nonrecurring basis. Under the standard, fair value is

defined as the exit price, or the amount that would be received to sell an asset or paid to transfer a liability in an orderly

transaction between market participants as of the measurement date. The standard also establishes a hierarchy for inputs

used in measuring fair value that maximizes the use of observable inputs and minimizes the use of unobservable inputs

by requiring that the most observable inputs be used when available. Observable inputs are inputs market participants

would use in valuing the asset or liability developed based on market data obtained from sources independent of the

Company. Unobservable inputs are inputs that reflect the Company’s assumptions about the factors market participants

would use in valuing the asset or liability developed based upon the best information available in the circumstances. The

hierarchy is broken down into three levels. Level 1 inputs are quoted prices (unadjusted) in active markets for identical

assets or liabilities. Level 2 inputs include quoted prices for similar assets or liabilities in active markets, quoted prices for

identical or similar assets or liabilities in markets that are not active, and inputs (other than quoted prices) that are

observable for the asset or liability, either directly or indirectly. Level 3 inputs are unobservable inputs for the asset or

liability. Categorization within the valuation hierarchy is based upon the lowest level of input that is significant to the fair

value measurement.

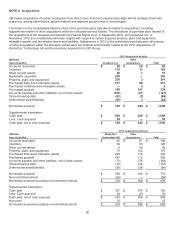

Acquisitions: The Company accounts for business acquisitions in accordance with ASC 805, Business Combinations. This

standard requires the acquiring entity in a business combination to recognize all (and only) the assets acquired and

liabilities assumed in the transaction and establishes the acquisition-date fair value as the measurement objective for all

assets acquired and liabilities assumed in a business combination. Certain provisions of this standard prescribe, among

other things, the determination of acquisition-date fair value of consideration paid in a business combination (including

contingent consideration) and the exclusion of transaction and acquisition-related restructuring costs from acquisition

accounting.

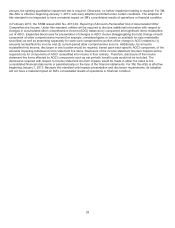

New Accounting Pronouncements

In October 2009, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU)

No. 2009-13, Multiple-Deliverable Revenue Arrangements—a consensus of the FASB Emerging Issues Task Force, that

provides amendments to the criteria for separating consideration in multiple-deliverable arrangements. As a result of

these amendments, multiple-deliverable revenue arrangements are separated in more circumstances than under pre-

existing U.S. GAAP. The ASU does this by establishing a selling price hierarchy for determining the selling price of a

deliverable. The selling price used for each deliverable is based on vendor-specific objective evidence (VSOE) if

available, third-party evidence (TPE) if VSOE is not available, or estimated selling price if neither VSOE nor TPE is

available. A vendor is required to determine its best estimate of selling price in a manner that is consistent with that used

to determine the price to sell the deliverable on a standalone basis. This ASU also eliminates the residual method of

allocation and requires that arrangement consideration be allocated at the inception of the arrangement to all deliverables

using the relative selling price method, which allocates any discount in the overall arrangement proportionally to each

deliverable based on its relative selling price. The ASU does not apply to arrangements for which industry specific

allocation and measurement guidance exists, such as long-term construction contracts and software transactions. For 3M,

ASU No. 2009-13 was effective beginning January 1, 2011. 3M elected to adopt the provisions of this standard

prospectively to new or materially modified arrangements beginning on the effective date. The adoption of this standard

did not have a material impact on 3M’s consolidated results of operations or financial condition.

In October 2009, the FASB issued ASU No. 2009-14, Certain Revenue Arrangements That Include Software Elements—a

consensus of the FASB Emerging Issues Task Force, that reduces the types of transactions that fall within the scope of

software revenue recognition guidance. Pre-existing software revenue recognition guidance required that its provisions be

applied to an entire arrangement involving the sale of any products or services containing or utilizing software when the

software was considered more than incidental to the product or service. As a result of the amendments included in ASU

No. 2009-14, many tangible products and services that rely on software are accounted for under the multiple-element

arrangements revenue recognition guidance rather than under the software revenue recognition guidance. Under the

ASU, the following components are excluded from the scope of software revenue recognition guidance: the tangible

element of the product, software products bundled with tangible products where the software components and non-

software components function together to deliver the product’s essential functionality, and undelivered components that

relate to software that is essential to the tangible product’s functionality. The ASU also provides guidance on how to

allocate transaction consideration when an arrangement contains both deliverables within the scope of software revenue

guidance (software deliverables) and deliverables not within the scope of that guidance (non-software deliverables). For

3M, ASU No. 2009-14 was effective beginning January 1, 2011. 3M elected to adopt the provisions of this standard

prospectively to new or materially modified arrangements beginning on the effective date. The adoption of this standard

did not have a material impact on 3M’s consolidated results of operations or financial condition.