Visa 2014 Annual Report Download - page 6

Download and view the complete annual report

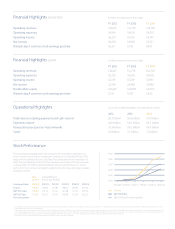

Please find page 6 of the 2014 Visa annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

|

|

We sit between two groups

of business partners, issuers

and acquirers, who maintain

relationships with the end

users of our products. The

issuers maintain and believe

they own the relationship

with the consumer, and the

acquirers maintain and believe

they own the relationship

with the merchants – who

ultimately have a direct

relationship with those same

consumers. Our success is

parallel to their success. They

need to grow for us to be

successful.

Visa’s current B2B model enjoys

many benefi ts. It is signifi cantly

easier and faster to scale than

direct to end user models. It

limits our exposure to credit

and fraud risk, and reduces

the need for us to build

capabilities such as large scale

customer support. As a result,

we have built a network that

provides reliability, ubiquity

and a consistent experience

for consumers and merchants

across the globe. Our fi nancial

institution partners, on the

other hand, have focused on

building strong relationships

with end users (consumers

and merchants), developing

the underlying infrastructure

and operations to support

those relationships, and

diff erentiating themselves

based on value-added services

over and above the network

off ering.

Financial Institutions

I have talked of our rich history

of building strong relationships

with our fi nancial institution

clients, but we know that they

no longer control Visa and

expect much more from us

than ever before. They also

have choices and are always

evaluating our value versus

our competitors. When we

compete for their business,

they will make the decision

based upon the quality of our

brand and the price of our

services, but they also evaluate

who will be the best payments

partner to help them achieve

their strategic objectives –

which usually revolve around

growth. They ask who

provides the best analysis, who

has marketing ideas, who has

the best product ideas, who

has the best technology and

who can they learn the most

from as the world evolves. It

is these interactions - acting

as an extension of our clients

inside of their organizations

- which will embed us inside

the fi nancial institutions

and provide the most

diff erentiation between our

competitors and us.

In 2014, we continued to have

great success strengthening

our partnerships with issuers

and acquirers, signing

numerous multi-year

agreements.