US Bank 2013 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2013 US Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

|

|

constraints. We continue to enjoy the benefits of the “flight

to quality” as customers recognize our exceptional products

and services, our superior financial performance and industry-

leading debt ratings — all signs of an outstanding banking

franchise. Our prudent management culture, a disciplined

attention to measuring every aspect of our business and a

commitment to aligning expenses with revenue have resulted

in a balance sheet that is strong and growing, along with

a mix of business that is well diversified and a franchise

performance that is consistent, predictable and repeatable.

We resist the temptation to enter businesses we don’t

understand; we don’t follow irrational players in the market

and we remain steadfastly diligent in evaluating potential

acquisitions that could only extend our success.

2014 is beginning much like 2013 with corporations and

consumers husbanding cash and foregoing discretionary

spending and investments. Soon we will see consumers

begin to spend rather than accumulate. We will also see

corporations begin to invest, rather than stockpile. Eventually,

we will expect to see spending and credit line utilization

increase and deposits decrease as the recovery takes hold.

However, for this current stage, deposits are still growing, an

indication that a robust recovery has yet to begin. We’re not

at the inflection point yet, but dialogue with our customers

leads us to believe that the recovery will accelerate in the

second half of this year. As I have said before, we are well-

positioned to capitalize on the upturn. Until then, we will

continue to prudently manage our Company — watching our

expenses and keeping them aligned with revenue, maintaining

and growing our market share and investing for the future.

Opportunity to grow

We are asked regularly about our interest in acquisitions —

and our answer is always the same. We are interested in

deepening our market share where we already have a branch

network. Our recent agreement to acquire branches in

Chicago, which doubles our presence in that great city, is

a perfect example. We expect to be a net branch grower

in the coming years. We like branches. Some of them might

not be traditional branches but, rather, in-store or on-site

branches in partnership with supermarkets, corporations,

hospitals, colleges or other high-traffic locations. We are

not interested in leap-frogging across states or acquiring a

few branches in a state where we have no critical mass or

presence. Additionally, we would like to continue to acquire

corporate trust and payments-related portfolios and companies;

acquisitions that increase competitive and operational scale in

these high value businesses. I have referred to our acquisition

focus as “one-offs.” By that I mean discreet, strategic acquisi-

tions which are smaller, rather than transformational, that are

priced correctly and enhance our franchise, capabilities and

product set and, ultimately, make sense for our shareholders.

A strong team and a strong future

I am very proud of our record full year 2013 earnings and

results. Our Company’s results are directly tied to the hard

work and dedication of our 67,000 employees, and I want to

take this opportunity to thank them for their contribution to

our success.

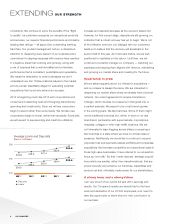

Average Loans and Deposits

(Dollars in Billions)

260

230

200

243.8 245.0 247.4

252.4 256.9

220.3

222.4 225.2 229.4 232.8

Deposits

Loans

4Q12 1Q13 2Q13 3Q13 4Q13

EXTENDING OUR STRENGTH

6 U.S. BANCORP