Ryanair 2004 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 2004 Ryanair annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

|

|

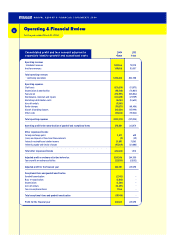

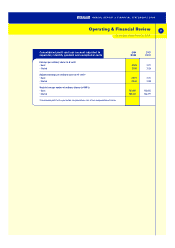

Operating Expenses (continued)

Maintenance costs increased by 46% to 43.4m reflecting an

increase in the size of the fleet operated, an increase in the

number of flight hours, and higher mainte n a n ce c h a rg es

relating to the “Buzz” aircraft, offset by maintenance savings

due to improved reliability arising from the higher proportion

of Boeing 737-800 “next generation” aircraft operated as a

percentage of the total fleet. In addition the entry into

operation of ten aircraft by way of operating lease has

resulted in the recognition of contractualprovisions forfuture

overhaul costs of 1.5mbeing recognised within maintenance

costs. This accounting policy contrasts with that adopted for

aircraft owned by the company where such maintenance costs

are capitalised and amortised.

Marketing and distribution costs increased by 10% to 16.1m

due to a higher spend on the promotion of 73 new routes, and

the launch of two new bases at Barcelonaand Rome in the last

quarter.

Ro u te charg es i n c rea sed by 61% to 1 1 0.3m due to an increa se

in the number of se c to rs fl own, an increa se in the ave ra g e

se c tor length and an increa se in the ave rage size of the airc ra ft

o p e ra ted which incur a higher ave rage charge, offset by t h e

impact of a wea ker sterling to euro exc hange ra te.

A i r p o rt and handling charg es i n c rea s ed by 36% to 1 4 7. 2 m

due to an increa se in the number of passe n g e rs fl own, and the

impact of increa sed airport and handling charg es on so m e

ex i sting rou t es, offset by lower charg e s on our new Eu ro p ea n

ro u tes.

Other expenses increased by 31% to 78.0m, which is less

than the growth in ancillary revenues due to improved margins

on some new and existing products, and cost reductions

achieved on other indirect overheads.

Adjusted Operating Profits

Adjusted operating profits have increased by 3% to 270.9m

during the year despite the decline in operating margins to

25% due to the reasons outlined above.

Interest Receivable

Interest receivable decreased by 7.5m to 23.9m reflecting

the strong growth in cash resources arising from the profitable

trading performance, offset by reductions in deposit interest

rates during the year. Interest payable increased by 16.7m

to 47.6m due to the increased level of debt arising from the

purchase of eight Boeing 737-800 ”nextgeneration” aircraft.

Foreign Exchange Gains

Fo r eign exchange gains a rose primarily from the co nve rsion of

sterling and US$ bank balances to euro at the year end, plus the

co nve rsion of fo re i g n cu r re n cy re ce i vable and paya b l e

b a l a n c es.

Taxation

Taxation adjusted for exceptional items has declined by 5%

during the year, in line with the decline in pre tax profits and a

decrease in the headlineIrish corporation tax rate.

Earning per Share (EPS)

Basic EPS (as adjusted for exceptional items and goodwill)

d e c rea sed by 6% to 29.91 euro ce n ts and is based on

757,446,873 shares which represents the weighted average

number of ordinary shares in issue during the year.

Balance Sheet

The group’s balance sheet continues to benefit from the strong

growth in profits generated. The group in turngenerated cash

from operating activities of 462.1m which partly funded the

acquisition of eight Boeing 737-800 “next generation” aircraft

and additionalaircraft deposits. Capital expenditure amounted

to 331.6m, primarily consisting of new aircraft additions

whilst debt funding increased to 953.0m during the same

period.

Capital Expenditure

During the year the group’s capital expenditure amounted to

331.6m. The majority of this related to the purchase of eight

Boeing 737-800 “next genera t i o n” airc ra ft and depos i ts

relating to the future acquisition of additional new Boeing 737-

800s. Ten new Boeing 737-800 “next generation” aircraft

were financed by way of operating lease during the year

bringing the total new aircraft operated to 18. Further details

are given in note 8.

Review of Cash Flow

Cash genera ted from operating activities was 4 62 .1 m ,

reflecting the overall profitability of the group. This has

enabled the group to increase its cash andliquid resources by

197.1m to 1,257.4m despite funding capital expenditure of

144.6m from internal cash resources. The group also made

total acq u i stion pay m e n ts of 32 .7m in respect of the

purchase of Buzz Stansted Limited including provision for

onerous leases.

(Continued)

Operating & Financial Review 11

A N N U A L R E P O RT & F I N A N C I A L S T A T E M E N T S 2 0 0 4