JP Morgan Chase 2014 Annual Report Download - page 9

Download and view the complete annual report

Please find page 9 of the 2014 JP Morgan Chase annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

|

|

77

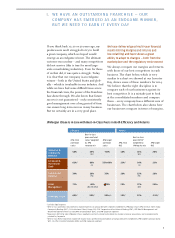

If you think back 10, 20 or 30 years ago, my

predecessors and I struggled to try to build

a great company, which we hoped would

emerge as an endgame winner. The ultimate

outcome was unclear – and many competitors

did not survive (this is true for most large-

scale consolidating industries). Even for those

of us that did, it was quite a struggle. Today,

it is clear that our company is an endgame

winner – both in the United States and glob-

ally – which is invaluable in any industry. And

while we have had some dicult times since

the financial crisis, the power of the franchise

has shone through. We also know that future

success is not guaranteed – only consistently

good management over a long period of time

can ensure long-term success in any business.

But we certainly are in a very good place.

We have delivered good multi-year financial

results (strong margins and returns and

low volatility) and have shown a great

ability to adapt to changes — both from the

marketplace and the regulatory environment

We always compare our margins and returns

with those of our best competitors in each

business. The chart below, which is very

similar to a chart we showed at our Investor

Day, shows some of these numbers for 2014.

We believe that the right discipline is to

compare each of our businesses against its

best competitor. It is a mistake just to look

at the consolidated numbers and compare

them – every company has a dierent mix of

businesses. The chart below also shows how

our businesses compare in terms of margins,

I. WE HAVE AN OUTSTANDING FRANCHISE — OUR

COMPANY HAS EMERGED AS AN ENDGAME WINNER,

BUT WE NEED TO EARN IT EVERY DAY

JPMorgan Chase Is in Line with Best-in-Class Peers in Both Eciency and Returns

Eciency Returns

JPM 2014

overhead

ratios

Best-in-class

peer overhead

ratios2 weighted

by JPM

revenue mix

JPM target

overhead

ratios

JPM 2014

ROE

Best-in-class

peer ROTCE4

weighted by

JPM equity mix

JPM target

ROE

Consumer &

Community

Banking

58% 55%

WFC

~50% 18% 16%

WFC

20%

Corporate &

Investment

Bank

62%160%

Citi

55%-60% 13%114%

Citi

13%

Commercial

Banking

39% 38%

PNC

35% 18% 13%

PNC

18%

Asset

Management

71% 69%

UBS WM & BLK

≤70% 23% 27%

BEN

25%+

JPMorgan Chase 60%159%155%+/- 13%313% ~15%3

1 Excludes legal expense

2 Best-in-class overhead ratio represents implied expenses of comparable peer segments weighted by JPMorgan Chase (JPM) revenue: Wells Fargo

Community Banking (WFC), Citi Institutional Clients Group (Citi), PNC Corporate and Institutional Banking (PNC), UBS Wealth Management and

Wealth Management Americas (UBS WM) and BlackRock (BLK), and JPM Corporate segment

3 Represents ROTCE for total JPMorgan Chase. Goodwill is primarily related to the Bank One merger and prior acquisitions and is predominantly

retained by Corporate

4 Best-in-class ROTCE represents implied net income minus preferred stock dividends of comparable peers weighted by JPM tangible common equity:

WFC, Citi, PNC, Franklin Templeton (BEN) and JPM Corporate segment