JP Morgan Chase 2014 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2014 JP Morgan Chase annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

|

|

1717

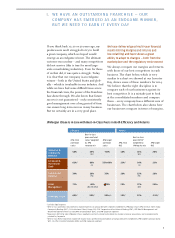

II. BUILT FOR THE LONG TERM

To make sure the test is severe enough, the

Fed essentially built into every bank’s results

some of the insucient and poor decisions

that some banks made during the crisis.

While I don’t explicitly know, I believe that

the Fed makes the following assumptions:

• The stress test essentially assumes that

certain models don’t work properly, partic-

ularly in credit (this clearly happened with

mortgages in 2009).

• The stress test assumes all of the negatives

of market moves but none of the positives.

• The stress test assumes that all banks’ risk-

weighted assets would grow fairly signifi-

cantly. (The Fed wants to make sure that

a bank can continue to lend into a crisis

and still pass the test.) This could clearly

happen to any one bank though it couldn’t

happen to all banks at the same time.

• The stress test does not allow a reduction

for stock buybacks and dividends. Again,

many banks did not do this until late in

the last crisis.

I believe the Fed is appropriately conserva-

tively measuring the above-mentioned aspects

and wants to make sure that each and every

bank has adequate capital in a crisis without

having to rely on good management decisions,

perfect models and rapid responses.

We believe that we would perform far better

under the Fed’s stress scenario than the Fed’s

stress test implies. Let me be perfectly clear

– I support the Fed’s stress test, and we at

JPMorgan Chase think that it is important

that the Fed stress test each bank the way it

does. But it also is important for our share-

holders to understand the dierence between

the Fed’s stress test and what we think actu-

ally would happen. Here are a few examples

of where we are fairly sure we would do

better than the stress test would imply:

• We would be far more aggressive on

cutting expenses, particularly compensa-

tion, than the stress test allows.

• We would quickly cut our dividend and

stock buyback programs to conserve

capital. In fact, we reduced our dividend

dramatically in the first quarter of 2009

and stopped all stock buybacks in the first

quarter of 2008.

• We would not let our balance sheet grow

quickly. And if we made an acquisition,

we would make sure we were properly

capitalized for it. When we bought Wash-

ington Mutual (WaMu) in September of

2008, we immediately raised $11.5 billion

in common equity to protect our capital

position. There is no way we would make

an acquisition that would leave us in a

precarious capital position.

• And last, our trading losses would unlikely

be $20 billion as the stress test shows. The

stress test assumes that dramatic market

moves all take place on one day and that

there is very little recovery of values. In

the real world, prices drop over time,

and the volatility of prices causes bid/ask

spreads to widen – which helps market-

makers. In a real-world example, in the six

months after the Lehman Brothers crisis,

J.P. Morgan’s actual trading results were

$4 billion of losses – a significant portion

of which related to the Bear Stearns acqui-

sition – which would not be repeated. We

also believe that our trading exposures are

much more conservative today than they

were during the crisis.

Finally, and this should give our shareholders

a strong measure of comfort: During the

actual financial crisis of 2008 and 2009, we

never lost money in any quarter.

We hope that, over time, capital planning

becomes more predictable. We do not believe

that banks are trying to “game” the system.

What we are trying to do is understand the

regulatory goals and objectives so we can

properly embed them in our decision-making

process. It is critical for the banking system

that the treatment of capital is coherent and