JP Morgan Chase 2014 Annual Report Download

Download and view the complete annual report

Please find the complete 2014 JP Morgan Chase annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

|

|

ANNUAL REPORT 2014

Table of contents

-

Page 1

A NNU A L REPORT 2014 -

Page 2

... Annual Report. JPMorgan Chase & Co. (NYSE: JPM) is a leading global financial services firm with assets of $2.6 trillion and operations worldwide. The firm is a leader in investment banking, financial services for consumers and small businesses, commercial banking, financial transaction processing... -

Page 3

communities clients customers employees veterans nonprofits business owners schools hospitals local governments -

Page 4

... - and it never stopped supporting clients, communities and the growth of economies around the world. I feel extraordinarily privileged to work for this great company with such talented people. Our management team and our employees do outstanding work every single day - sometimes under enormous... -

Page 5

... in the future. Our financial results reflected strong underlying performance across our businesses. Over the course of last year, our four franchises maintained - and even strengthened - our leadership positions and continued to gain market share, improve customer satisfaction and foster innovation... -

Page 6

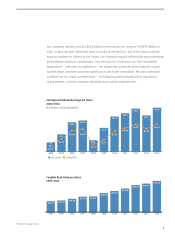

...(B) Performance since the Bank One and JPMorgan Chase & Co. merger (7/1/2004-12/31/2014): Compounded annual gain Overall gain 14.1% 300.5% 8.0% 124.5% 6.1% 176.0% Tangible book value over time captures the company's use of capital, balance sheet and profitability. In this chart, we are looking... -

Page 7

... our business by investing in infrastructure, systems, technology and new products and by adding bankers and branches around the world. New and Renewed Credit and Capital for Clients at December 31, Corporate clients ($ in trillions) Consumer and Commercial Banking ($ in billions) Year-over-year... -

Page 8

...Wholesale $861  Client assets(a) 10% 13% 3% $2,035 $2,244 $2,534 $2,609 2011 2012 2013 2014 (a) Represent assets under management as well as custody, brokerage, administration and deposit accounts Represents activities associated with the safekeeping and servicing of assets Assets... -

Page 9

... 55% WFC Returns Best-in-class peer ROTCE4 weighted by JPM equity mix 16% WFC JPM 2014 overhead ratios JPM target overhead ratios ~50% JPM 2014 ROE 18% JPM target ROE 20% Consumer & Community Banking Corporate & Investment Bank Commercial Banking Asset Management 58% 62%1 60% Citi 55%-60... -

Page 10

... States - 28 wholesale offices abroad - 2,498 Chase Private Client locations/ branches, supported by 594 new Private Client advisors - 20 Commercial Banking expansion cities, including approximately 350 Commercial Banking bankers - 205 small business bankers A good company always should be investing... -

Page 11

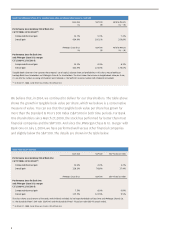

..., the capital we returned to shareholders through dividends and stock buybacks, our returns on tangible common equity and our high quality liquid assets (HQLA). High quality liquid assets essentially are deposits held at the Federal Reserve and central banks, agency mortgage-backed securities and... -

Page 12

... Gross Investment Banking revenue ($ in billions) % of North America Investment Banking fees Global active long-term open-end mutual fund AUM flows10 AUM market share10 Overall Global Private Bank (Euromoney) Client assets market share11 U.S. Hedge Fund Manager (Absolute Return)12 AUM market share12... -

Page 13

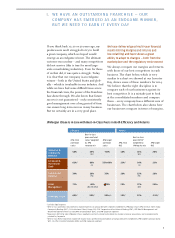

... Study; Big Banks defined as Chase, Bank of America, Wells Fargo, Citibank, U.S. Bank, PNC Bank Our mix of businesses works for clients - and for shareholders All companies, including banks, have a slightly different mix of businesses, products and services. The most critical question is... -

Page 14

...these types of institutions. On the average day, we raise or lend $6 billion for these institutions. On the average day, we buy or sell approximately $800 billion of securities to serve investors and issuers. In 2014, our Corporate & Investment Bank raised $61 billion for states, cities, governments... -

Page 15

... approximately $700 million a year on research so that we can educate investors, institutions and governments about economies, markets and companies. The needs of these clients will be met - one way or another - by large financial institutions that can bear the costs and risks involved. Simply put... -

Page 16

... Chase has contributed approximately $8 billion to the Federal Deposit Insurance Corporation to help pay for the resolution of those banks. And, yes, there are both costs and benefits to size and complexity The benefits of size are obvious: huge economies of scale, the ability to serve large clients... -

Page 17

...let businesses like Global Titanium expand jobs and residential development and new construction of apartment buildings in Detroit's urban core and neighborhoods. • We created the Detroit Service Corps to bring more than 50 of our top managers to work full time with Detroit nonprofits to help them... -

Page 18

... oil prices. Rest assured, we extensively manage our risks. The Federal Reserve's Comprehensive Capital Analysis and Review (CCAR) stress test is another tough measure of our survival capability. The protect this company - for the sake of our shareholders, clients, employees and communities. If... -

Page 19

... in a precarious capital position. • And last, our trading losses would unlikely be $20 billion as the stress test shows. The stress test assumes that dramatic market moves all take place on one day and that there is very little recovery of values. In the real world, prices drop over time, and the... -

Page 20

...functions, from finance and human resources to operations and controls. This kind of investing should not be done in a stop-start way to manage short-term profitability. Quarterly earnings - even annual earnings - frequently are the result of actions taken over the past five or 10 years. Our company... -

Page 21

... When normal interest rates return, we believe this will add $3 billion to revenue and improve our operating margin to more than 40%. Our long-term view means that we do not manage to temporary P/E ratios - the tail should not wag the dog Price/earnings (P/E) ratios, like stock prices, are temporary... -

Page 22

... our earnings than they otherwise might pay. Having said all this, the contours of all of the new regulations have emerged, and we believe that regulatory uncertainty will diminish over time. And, we hope, so will the drag on our P/E ratio. Think like a long-term investor, manage like an operator So... -

Page 23

... Plan Services unit ü E xited prepaid card and Order to Pay ü businesses Sold health savings account business ü S implified Mortgage Banking products ü from 37 to 18 products as of 2014, with a target of further reducing to 15 R ationalized Global Investment ü Management products... -

Page 24

... technology employees' time to improve our Mortgage Servicing business, including enhancing the loan modification application to improve the systems that track and manage customer complaints and responses. • Model review. More than 300 employees are working in Model Risk and Development. In 2014... -

Page 25

... Promoting use of electronic trading venues and central clearing  Bolstering capital and margin requirements  Restricting banks from undertaking certain types of market activities  Controlling risks associated with certain trading and funds-related activity  1,000+ people working across... -

Page 26

... look at just assets - it looks at products, services, assets, type of client (i.e., international and financial or corporate) and collateral type, among others in order to determine capital levels. G-SIB will have its highest impact on nonoperating deposits, gross derivatives, the clearing business... -

Page 27

... to some key regulators, will effectively end Too Big to Fail and will G-SIB capital surcharge, however calculated, is an important part of our capital needs. And since we are outsized, relative to our competitors (our capital surcharge currently is estimated as 4.5% of risk-weighted assets, yet... -

Page 28

..., the regulators have almost finished plans around total lossabsorbing capacity, which will require large banks to hold a lot of additional long-term debt, which could be converted to equity in the event of a failure and thereby enable the firm to remain open to serve customers and markets. Second... -

Page 29

... Client started as a gleam in our eye back in 2010. Chase Private Client branches credit card), Paymentech, deposits and loans all at once. We believe that if we bundle the services that small businesses really want and also provide meaningful advice, we can dramatically grow this business. Looking... -

Page 30

..., small business and private banking to middle market and local coverage of large corporations. We particularly are excited about our payments business in total. The combination of Chase Erdoes' Investor Day presentation, she showed that while we have the best private bank in the United States, our... -

Page 31

... brains and money working on various alternatives to traditional banking. The ones you read about most are in the lending business, whereby the firms can lend to individuals and small businesses very quickly and - these entities believe - effectively by using Big Data to enhance credit underwriting... -

Page 32

... to be very aggressive in limiting and controlling how third parties can use JPMorgan Chase data. It is critical that government and business and regulators collaborate effectively and in real time. Cybersecurity is an area where government and business have been working well together, but there is... -

Page 33

... in the next crisis. Non-bank competitors are increasingly beginning to do basic lending in consumer, small business and middle market. In middle market syndicated lending, their share recently has increased from 3% a few years ago to 5% today, and many people estimate that it will continue to... -

Page 34

... "run-on-the-market" type of behavior by investors. So let's now turn to look at how a crisis might affect the markets in the new world. The money markets (deposits, repos, short-term Treasuries) will behave differently in the next crisis • Banks are required to hold liquid assets against 100% of... -

Page 35

...trillion is accounted for by foreign exchange reserve holdings for foreign countries that have a strong desire to hold Treasuries in order to manage their currencies. The Federal Reserve owns $2.5 trillion in Treasuries, which it has said it will not sell for now; and banks hold $0.5 trillion, which... -

Page 36

..., from hedge funds to long-term investors, including corporations and large money managers, will, at some point, step in and buy assets. The government, of course, always is able to step in and play an important role. In addition, regulators can improve the liquidity rules to allow banks to provide... -

Page 37

... Chase has served its shareholders, customers and communities with distinction for more than 200 years. Since we were founded, our company has been guided by a simple principle that perhaps was best articulated by J.P. Morgan, Jr., in 1933, when he said: "I should state that at all times, the... -

Page 38

... Code of Conduct for all employees to the Code of Ethics for Finance Professionals that applies to the CEO, Chief Financial Officer, Controller and all professionals of the firm worldwide serving in a finance, accounting, corporate treasury, tax or investor relations role. • We have enhanced our... -

Page 39

.... Then morale will improve, and employees will be proud of where they work every day. would like all our senior managers to have a large portion of their net worth in the company. We believe this fosters partnership. While some make the argument that it causes excessive risk taking - we disagree... -

Page 40

... income distribution. We invest a significant amount of time and money to ensure that all of our employees are properly compensated. We still have a defined benefit pension plan for most of our employees that provides a fixed income upon retirement to supplement Social Security and any other savings... -

Page 41

... performance and morale remain strong in this environment. C LOS I N G COMME N TS I feel enormously fortunate to be part of the remarkable 200-year journey of this exceptional company. I wish you all could see our employees and your management team at work, particularly in these challenging times... -

Page 42

...- shareholders, clients, customers and employees - given our significance to worldwide markets and the global economy. We continue to respond to the changing regulatory landscape, including requirements for G-SIBs, and we are evaluating the businesses we manage and the products and services we offer... -

Page 43

...regulatory requirements, we are driving a coordinated approach to management of the firm's balance sheet. 2014 featured final versions of important regulatory liquidity rules, notably the liquidity coverage ratio by U.S. banking regulators and Basel's final rule on the net stable funding ratio, with... -

Page 44

... of security threats. In addition, we will continue to innovate in 2015 by improving branch automation and efficiency, extending our electronic trading platforms, launching an advisor workstation platform for Asset Management and implementing a new commercial real estate loan originations... -

Page 45

..., including a new, global set of Know Your Customer standards. This year, Compliance will focus on enhancing standards for market conduct risk, fiduciary responsibilities, employee compliance and regulatory reporting. Ongoing strategic technology investments and process improvements will position us... -

Page 46

... and Credit Card businesses and felt the continued impact of lower deposit margins. While credit performance still is very strong, the rate of improvement compared with last year has slowed. Overall, we ended the year with a strong return on equity (ROE) of 18%, just under our long-term target of... -

Page 47

... our net new CPC deposits and investments, with 60% of new investments coming from customers who are investing with Chase for the first time. With 55% of affluent households living within two miles of a Chase branch or ATM, we feel well-positioned to continue that growth. Business Banking loan... -

Page 48

...our costs per deposit by ~50% in 2014 versus 2007. Our 5,600 branch network is one of our most important assets for acquiring and deepening relationships. Last year, our branches helped nearly 20,000 first-time homebuyers and 400,000 new small businesses and approved more than 1 million credit cards... -

Page 49

... deposit share in three of the largest deposit markets • #1 most visited banking portal in the United States - chase.com; #1 mobile banking functionality • #1 Small Business Administration lender for women and minorities in the United States for the third year in a row • #1 credit card issuer... -

Page 50

...the CIB to maintain its leading market share across all business lines and generate strong returns on $34.6 billion in net revenue - the highest among our corporate and investment bank peers. With an improving global economy in 2015, I am confident that many of the headwinds we encountered last year... -

Page 51

... efforts already undertaken in 2014. Serving clients = gaining share J.P. Morgan gained share and continued to hold top-tier positions across our lines of business, a testament to the firm's client focus and resiliency. In a difficult year, the CIB share of Investment Banking fee revenue led the... -

Page 52

... business lines most valuable to clients and the CIB. By selectively narrowing our business, we also improved our ability to invest in the technologies and services our clients will require and demand in the future while making us stronger for the long term. "How We Do Business - The Report" During... -

Page 53

...countries, serving 7,200 of the world's most significant corporates and financial institutions, governments and nonprofit organizations. • No other firm in 2014 placed so consistently among the top ranks of products across Investment Banking, Markets and Investor Services. • The CIB is targeting... -

Page 54

... uses nine of our products and services, and it is common to see our longer-term relationships use more than 20. When our clients seek to make more efficient payments, generate better reporting, and securely process transactions from their own customers, we leverage our market-leading commercial... -

Page 55

...total sales in the next few years. Our International Banking team is well-positioned to help these clients grow and operate in overseas markets. We've added dedicated resources in 14 key international locations and have access to JPMorgan Chase's international footprint in 60 countries. In our real... -

Page 56

... Morgan ACCESS Online ranked the #1 cash management portal in North America by Greenwich Associates 3 Thomson Reuters as of year-end 2014. Traditional middle market is defined as credit facilities of -

Page 57

... private equity, real assets and other longer-dated or closed-end investment strategies For footnoted information, refer to slides 23 and 24 in the 2015 Asset Management Investor Day presentation, which is available on JPMorgan Chase & Co.'s website at http://investor.shareholder.com/jpmorganchase... -

Page 58

... time, delivering first-rate financial performance to our shareholders. In 2014, we achieved revenue growth of 5%, pre-tax income growth of 5%, pre-tax margin of 29% and return on equity of 23%. Within the business, each of our client franchises - Global Investment Management (GIM) and Global Wealth... -

Page 59

... • #1 Global Active Long-Term Mutual Fund Flows, Strategic Insight • 2014 U.S. Allocation Fund Manager of the Year, Morningstar • Top European Buyside Firm, Thomson Reuters Extel • Best Asset Management Company for Asia, The Asset • Best Private Bank for Asia High-Net-Worth, The Asset... -

Page 60

... develop strategies for increasing international trade and investment ties. Second, we are helping cities around the world address one of their biggest challenges: the need for a better trained workforce to fill the millions of jobs left open due to a shortage of applicants with the right skills... -

Page 61

.... 59 New Skills at Work In December 2013, we launched New Skills at Work, a $250 million, five-year workforce readiness initiative to close skills gaps in sectors where employers struggle to fill vacancies and to help job seekers access the education and training required for these positions. A key... -

Page 62

...000 students, create nearly 2,200 manufacturing jobs and serve 380,000 patients at healthcare facilities. • Implemented year one of the firm's New Skills at Work program, a $250 million, five-year initiative to strengthen local workforce systems by providing real-time data and supporting partners... -

Page 63

...Management Capital Management Liquidity Risk Management Critical Accounting Estimates Used by the Firm Accounting and Reporting Developments Nonexchange-Traded Commodity Derivative Contracts at Fair Value Forward-Looking Statements Supplementary information: 307 309 Selected Quarterly Financial Data... -

Page 64

...deposits ratio High quality liquid assets ("HQLA") (in billions)(c) Common equity tier 1 ("CET1") capital ratio(d) Tier 1 capital ratio (d) Total capital ratio(d) Tier 1 leverage ratio(d) Selected balance sheet data (period-end) Trading assets Securities(e) Loans Total assets Deposits Long-term debt... -

Page 65

... five-year cumulative total return for JPMorgan Chase & Co. ("JPMorgan Chase" or the "Firm") common stock with the cumulative return of the S&P 500 Index, the KBW Bank Index and the S&P Financial Index. The S&P 500 Index is a commonly referenced U.S. equity benchmark consisting of leading companies... -

Page 66

... services for consumers and small businesses, commercial banking, financial transaction processing and asset management. Under the J.P. Morgan and Chase brands, the Firm serves millions of customers in the U.S. and many of the world's most prominent corporate, institutional and government clients... -

Page 67

... enterprise risks and critical accounting estimates affecting the Firm and its various lines of business, this Annual Report should be read in its entirety. Financial performance of JPMorgan Chase Year ended December 31, (in millions, except per share data and ratios) portfolio and credit card, was... -

Page 68

... ceased originating student loans, exited certain high risk customers and became more selective about on-boarding certain customers. Following on these initiatives, in 2014, the Firm exited several non-core credit card co-branded relationships, sold the Retirement Plan Services business within AM... -

Page 69

... card relationships, expansion into new markets, and hiring additional sales staff and client advisors, are expected to generate significant revenue growth over the next several years. At the same time, the Firm intends to leverage its scale and improve its operating efficiencies so that it can fund... -

Page 70

...amortization of new account origination costs. For additional information on credit card income, see CCB segment results on pages 81-91. Revenue Year ended December 31, (in millions) Investment banking fees Principal transactions(a) Lending- and deposit-related fees Asset management, administration... -

Page 71

... the impact of the runoff of higher yielding loans and originations of lower yielding loans, and lower trading-related net interest income. The decrease in net interest income was partially offset by lower long-term debt and other funding costs. The Firm's average interest-earning assets were... -

Page 72

..., including front office sales and support staff, and costs related to the Firm's control agenda; these were partially offset by lower compensation expense in CIB and in CCB's Mortgage Banking business, reflecting the effect of lower servicing headcount. 70 JPMorgan Chase & Co./2014 Annual Report -

Page 73

... income and expense subject to U.S. federal, state and local taxes, business tax credits, tax benefits associated with prior year tax adjustments and audit resolutions. Income tax expense Year ended December 31, (in millions, except rate) Income tax expense Effective tax rate 2014 8,030 27.0% 2013... -

Page 74

... Mortgage servicing rights Other intangible assets Other assets Total assets Liabilities Deposits Federal funds purchased and securities loaned or sold under repurchase agreements Commercial paper Other borrowed funds Trading liabilities: Debt and equity instruments Derivative payables Accounts... -

Page 75

... funds purchased and securities loaned or sold under repurchase agreements was predominantly attributable to higher financing of the Firm's trading assets-debt and equity instruments. The increase was partially offset by client activity in CIB. For additional information on the Firm's Liquidity Risk... -

Page 76

... involves a company selling assets to the SPE; the SPE funds the purchase of those assets by issuing securities to investors. JPMorgan Chase uses SPEs as a source of liquidity for itself and its clients by securitizing financial assets, and by creating investment products for clients. The Firm is... -

Page 77

...) On-balance sheet obligations Deposits(a) Federal funds purchased and securities loaned or sold under repurchase agreements Commercial paper Other borrowed funds(a) Beneficial interests issued by consolidated VIEs(a) Long-term debt Other(b) Total on-balance sheet obligations Off-balance sheet... -

Page 78

... and other short-term interest-earning assets. Cash used in investing activities during 2014, 2013, and 2012 resulted from increases in deposits with banks, attributable to higher levels of excess funds; in 2014, cash was used for growth in wholesale and consumer loans, while in 2013 and 2012 cash... -

Page 79

...-GAAP financial measures used by other companies. The following summary table provides a reconciliation from the Firm's reported U.S. GAAP results to managed basis. 2014 Year ended December 31, (in millions, except ratios) Other income Total noninterest revenue Net interest income Total net revenue... -

Page 80

... management also reviews core net interest income to assess the performance of its core lending, investing (including asset-liability management) and deposit-raising activities. These activities exclude the impact of CIB's market-based activities. The core data presented below are non-GAAP financial... -

Page 81

..., Corporate & Investment Bank, Commercial Banking and Asset Management. In addition, there is a Corporate segment. The business segments are determined based on the products and services provided, or the type of customer served, and they reflect the manner in which financial information is currently... -

Page 82

..., except ratios) Consumer & Community Banking Corporate & Investment Bank Commercial Banking Asset Management Corporate Total $ $ Provision for credit losses 2014 3,520 $ (161) (189) 4 (35) 3,139 $ 2013 335 $ (232) 85 65 (28) 225 $ 2012 3,774 (479) 41 86 (37) 3,385 $ Net income/(loss) 2014 6,925... -

Page 83

...transaction. Card issues credit cards to consumers and small businesses, provides payment services to corporate and public sector clients through its commercial card products, offers payment processing services to merchants, and provides auto and student loan services. Selected income statement data... -

Page 84

...and costs related to the control agenda. Selected metrics As of or for the year ended December 31, (in millions, except headcount) Selected balance sheet data (period-end) Total assets Trading assets - loans(a) Loans: Loans retained Loans held-for-sale Total loans Deposits Equity(b) Selected balance... -

Page 85

...2014 Annual Report Selected metrics As of or for the year ended December 31, (in millions, except ratios and where otherwise noted) Credit data and quality statistics Net charge-offs Net charge-off rate Allowance for loan losses Nonperforming assets Retail branch business metrics Net new investment... -

Page 86

... Banking Selected Financial statement data As of or for the year ended December 31, (in millions, except ratios) Revenue Mortgage fees and related income All other income Noninterest revenue Net interest income Total net revenue Provision for credit losses Noninterest expense Income before income... -

Page 87

... Banking net income Overhead ratios Mortgage Production Mortgage Servicing Real Estate Portfolios 85% 85 43 $ 1,668 78% 113 42 43% 132 39 (a) Prior periods were revised to conform with the current presentation. (b) Includes provision for credit losses. JPMorgan Chase & Co./2014 Annual Report... -

Page 88

... FDIC-related expense. 86 Mortgage Production and Mortgage Servicing Selected metrics As of or for the year ended December 31, (in millions, except ratios) Selected balance sheet data (Period-end) Trading assets - loans(a) Loans: Prime mortgage, including option ARMs(b) Loans held-for-sale Selected... -

Page 89

... 31, 2014, 2013 and 2012, respectively. (c) Represents the ratio of MSR carrying value (period-end) to thirdparty mortgage loans serviced (period-end) divided by the ratio of loan servicing-related revenue to third-party mortgage loans serviced (average). JPMorgan Chase & Co./2014 Annual Report 87 -

Page 90

Management's discussion and analysis Mortgage servicing-related matters The financial crisis resulted in unprecedented levels of delinquencies and defaults of 1-4 family residential real estate loans. Such loans required varying degrees of loss mitigation activities. Foreclosure is usually a last ... -

Page 91

...impairment estimates and lower balances related to credit card loans modified in TDRs, runoff in the student loan portfolio, and lower estimated losses in auto loans. The prior-year provision included a $1.7 billion reduction in the allowance for loan losses. JPMorgan Chase & Co./2014 Annual Report... -

Page 92

... Selected balance sheet data (average) Total assets Loans: Credit Card Auto Student Total loans Business metrics Credit Card, excluding Commercial Card Sales volume (in billions) New accounts opened Open accounts Accounts with sales activity % of accounts acquired online Merchant Services (Chase... -

Page 93

Card Services supplemental information Year ended December 31, (in millions, except ratios) Revenue Noninterest revenue Net interest income Total net revenue Provision for credit losses Noninterest expense Income before income tax expense Net income Percentage of average loans: Noninterest revenue ... -

Page 94

...the Securities Services business, a leading global custodian which includes custody, fund accounting and administration, and securities lending products sold principally to asset managers, insurance companies and public and private investment funds. Selected income statement data Year ended December... -

Page 95

... across high grade, high yield and loan products. The Firm maintained its #2 ranking for M&A, and improved share of fees both globally and in the U.S. compared to the prior year. Treasury Services revenue was $4.1 billion, down 1% compared with the prior year, primarily driven by lower trade finance... -

Page 96

...,107 2014 2013 2012 Selected metrics As of or for the year ended December 31, (in millions, except ratios and where otherwise noted) Credit data and quality statistics Net charge-offs/ (recoveries) Nonperforming assets: Nonaccrual loans: Nonaccrual loans retained(a)(b) Nonaccrual loans heldfor-sale... -

Page 97

... ratios and where otherwise noted) Market risk-related revenue - trading loss days(a) Assets under custody ("AUC") by asset class (period-end) in billions: Fixed Income Equity Other(b) Total AUC Client deposits and other third party liabilities (average)(c) Trade finance loans (period-end) 2014... -

Page 98

...533 16,448 18,314 $ 34,762 2014 2013 2012 (a) Total net revenue is based predominantly on the domicile of the client or location of the trading desk, as applicable. Loans outstanding (excluding loans held-for-sale and loans at fair value), client deposits and other third-party liabilities, and AUC... -

Page 99

... real estate investors and owners. Partnering with the Firm's other businesses, CB provides comprehensive financial solutions, including lending, treasury services, investment banking and asset management to meet its clients' domestic and international financial needs. Selected income statement data... -

Page 100

...end loans by client segment Middle Market Banking Corporate Client Banking Commercial Term Lending Real Estate Banking Other Total Commercial Banking loans Selected balance sheet data (average) Total assets Loans: Loans retained Loans held-for-sale and loans at fair value Total loans Client deposits... -

Page 101

...sale and loans at fair value Total nonaccrual loans Assets acquired in loan satisfactions Total nonperforming assets Allowance for credit losses: Allowance for loan losses Allowance for lending-related commitments Total allowance for credit losses Net charge-off/(recovery) rate(b) Allowance for loan... -

Page 102

... Global Wealth Management clients, AM also provides retirement products and services, brokerage and banking services including trusts and estates, loans, mortgages and deposits. The majority of AM's client assets are in actively managed portfolios. Selected income statement data Year ended December... -

Page 103

..., including investment management, capital markets and risk management, tax and estate planning, banking, lending and specialty-wealth advisory services. Selected metrics As of or for the year ended December 31, (in millions, except ranking data and ratios) % of JPM mutual fund assets rated as... -

Page 104

... asset class Liquidity Fixed income Equity Multi-asset and alternatives Total assets under management Custody/brokerage/administration/ deposits Total client assets Memo: Alternatives client assets(a) Assets by client segment Private Banking Institutional Retail Total assets under management Private... -

Page 105

..., Internal Audit, Risk Management, Oversight & Control, Corporate Responsibility and various Other Corporate groups. Other centrally managed expense includes the Firm's occupancy and pension-related expenses that are subject to allocation to the businesses. Selected income statement data Year ended... -

Page 106

...rate and foreign exchange risks, as well as executing the Firm's capital plan. The risks managed by Treasury and CIO arise from the activities undertaken by the Firm's four major reportable business segments to serve their respective client bases, which generate both on- and off-balance sheet assets... -

Page 107

... Chase's business activities. When the Firm extends a consumer or wholesale loan, advises customers on their investment decisions, makes markets in securities, or conducts any number of other services or activities, the Firm takes on some degree of risk. The Firm's overall objective in managing risk... -

Page 108

... rates, foreign exchange rates, equity prices, commodity prices, implied volatilities or credit spreads. The risk of the potential for adverse consequences from decisions based on incorrect or misused model outputs and reports. Model Status, Model Tier FX Net Open Position ("NOP") 156-160 Market... -

Page 109

...and manage: (i) credit risk, market risk, liquidity risk, model risk, structural interest rate risk, principal risk and country risk; (ii) the governance frameworks or policies for operational, fiduciary, reputational risks and the New Business Initiative Approval ("NBIA") process; and (iii) capital... -

Page 110

...risk. ALCO is responsible for reviewing and approving the Firm's funds transfer pricing policy (through which lines of business "transfer" interest rate and foreign exchange risk to Treasury). ALCO is responsible for reviewing the Firm's Liquidity Risk Management and JPMorgan Chase & Co./2014 Annual... -

Page 111

... CIB, Consumer & Community Banking, Commercial Banking, Asset Management and certain corporate functions, including Treasury and CIO. In addition to the committees, forums and groups listed above, the Firm has other management committees and forums at the LOB and regional levels, where risk-related... -

Page 112

...credit to a variety of customers, ranging from large corporate and institutional clients to individual consumers and small businesses. In its consumer businesses, the Firm is exposed to credit risk primarily through its residential real estate, credit card, auto, business banking and student lending... -

Page 113

... on an annual basis. Industry and counterparty limits, as measured in terms of exposure and economic credit risk capital, are subject to stress-based loss constraints. Management of the Firm's wholesale credit risk exposure is accomplished through a number of means, including Loan underwriting and... -

Page 114

... in loan satisfactions Real estate owned Other Total assets acquired in loan satisfactions Total assets Lending-related commitments Total credit portfolio Credit Portfolio Management derivatives notional, net(a) Liquid securities and other cash collateral held against derivatives Year ended December... -

Page 115

...business banking loans, and student loans. The Firm's focus is on serving the prime segment of the consumer credit market. For further information on consumer loans, see Note 14. The credit performance of the consumer portfolio continues to benefit from the improvement in the economy and home prices... -

Page 116

... in home prices and delinquencies. Approximately 15% of the Firm's home equity portfolio consists of home equity loans ("HELOANs") and the remainder consists of home equity lines of credit ("HELOCs"). HELOANs are generally fixed-rate, closed-end, amortizing loans, with terms ranging from 3-30 years... -

Page 117

... loan portfolio reflects a high concentration of prime-quality credits. Business banking: Business banking loans increased from December 31, 2013 due to an increase in loan originations. Nonaccrual loans improved compared with December 31, 2013. Net charge-offs for the year ended December 31, 2014... -

Page 118

... residential real estate loans The current estimated average loan-to-value ("LTV") ratio for residential real estate loans retained, excluding mortgage loans insured by U.S. government agencies and PCI loans, was 71% at December 31, 2014, compared with 75% at December 31, 2013. Although home prices... -

Page 119

...estimated collateral values - PCI loans 2014 December 31, (in millions, except ratios) Home equity Prime mortgage Subprime mortgage Option ARMs $ Unpaid principal balance 17,740 10,249 4,652 16,496 Current estimated LTV ratio(a) 83% 76 82 74 (b) 2013 Ratio of net carrying value to current estimated... -

Page 120

...loans are generally accounted for and reported as troubled debt restructurings ("TDRs"). For further information on modifications for the years ended December 31, 2014 and 2013, see Note 14. Modified residential real estate loans 2014 On- balance sheet loans Nonaccrual on-balance sheet loans(d) 2013... -

Page 121

... Card Total credit card loans increased from December 31, 2013 due to higher new account originations and increased credit card sales volume. The 30+ day delinquency rate decreased to 1.44% at December 31, 2014, from 1.67% at December 31, 2013. For the years ended December 31, 2014 and 2013, the net... -

Page 122

... WHOLESALE CREDIT PORTFOLIO The Firm's wholesale businesses are exposed to credit risk through underwriting, lending and trading activities with and for clients and counterparties, as well as through various operating services such as cash management and clearing activities. A portion of the loans... -

Page 123

... Lending-related commitments Subtotal Loans held-for-sale and loans at fair value(a) Receivables from customers and other Total exposure - net of liquid securities and other cash collateral held against derivatives Credit Portfolio Management derivatives net notional by reference entity ratings... -

Page 124

... 30 days or more past due and accruing loans Liquid securities and other cash collateral held against derivative receivables As of or for the year ended December 31, 2014 (in millions) Top 25 industries(a) Real Estate Banks & Finance Cos Healthcare Oil & Gas Consumer Products Asset Managers State... -

Page 125

... 30 days or more past due and accruing loans Liquid securities and other cash collateral held against derivative receivables As of or for the year ended December 31, 2013 (in millions) Top 25 industries(a) Real Estate Banks & Finance Cos Healthcare Oil & Gas Consumer Products Asset Managers State... -

Page 126

... clients to high-net-worth individuals. For further discussion on loans, including information on credit quality indicators, see Note 14. The Firm actively manages its wholesale credit exposure. One way of managing credit risk is through secondary market sales of loans and lending-related... -

Page 127

... and settlement types, see Note 6. The following table summarizes the net derivative receivables for the periods presented. Derivative receivables December 31, (in millions) Interest rate Credit derivatives Foreign exchange Equity Commodity Total, net of cash collateral Liquid securities and other... -

Page 128

... Firm risk manages exposure to changes in CVA by entering into credit derivative transactions, as well as interest rate, foreign exchange, equity and commodity derivative transactions. The accompanying graph shows exposure profiles to the Firm's current derivatives portfolio over the next 10 years... -

Page 129

... Note 6. Credit portfolio management activities Included in the Firm's end-user activities are credit derivatives used to mitigate the credit risk associated with traditional lending activities (loans and unfunded commitments) and derivatives counterparty exposure in the Firm's wholesale businesses... -

Page 130

... of the allowance for credit losses and related management judgments, see Critical Accounting Estimates Used by the Firm on pages 161-165 and Note 15. At least quarterly, the allowance for credit losses is reviewed by the Chief Risk Officer, the Chief Financial Officer and the Controller of... -

Page 131

... The allowance for lending-related commitments is reported in other liabilities on the Consolidated balance sheets. (d) The Firm's policy is generally to exempt credit card loans from being placed on nonaccrual status as permitted by regulatory guidance. JPMorgan Chase & Co./2014 Annual Report 129 -

Page 132

...Year ended December 31, (in millions) Consumer, excluding credit card Credit card Total consumer Wholesale Total $ $ Provision for loan losses 2014 3,079 3,493 (269) 3,224 $ 2013 2,179 307 (119) 188 $ 2012 302 3,444 3,746 (359) 3,387 $ $ 414 $ (1,872) $ Provision for lending-related commitments 2014... -

Page 133

... in the value of the Firm's assets and liabilities resulting from changes in market variables such as interest rates, foreign exchange rates, equity prices, commodity prices, implied volatilities or credit spreads. Market risk management Market Risk is an independent risk management function that... -

Page 134

... activities and related market risks • Makes markets and services clients across fixed income, foreign exchange, equities and commodities • Market risk arising from a potential decline in net income as a result of changes in market prices; e.g. rates and credit spreads Positions included in Risk... -

Page 135

... daily market values may be different across product types or risk management systems. The VaR model results across all portfolios are aggregated at the Firm level. Data sources used in VaR models may be the same as those used for financial statement valuations. However, in cases where market prices... -

Page 136

... (http:// investor.shareholder.com/jpmorganchase/basel.cfm). The table below shows the results of the Firm's Risk Management VaR measure using a 95% confidence level. Total VaR As of or for the year ended December 31, (in millions) CIB trading VaR by risk type Fixed income Foreign exchange Equities... -

Page 137

...markets. The Firm runs weekly stress tests on market-related risks across the lines of business using multiple scenarios that assume significant changes in risk factors such as credit spreads, equity prices, interest rates, currency rates or commodity prices. The framework uses a grid-based approach... -

Page 138

... levels - results in a 12-month pretax core net interest income benefit of $566 million. The increase in core net interest income under this scenario reflects the Firm reinvesting at the higher long-term rates, with funding costs remaining unchanged. 136 JPMorgan Chase & Co./2014 Annual Report -

Page 139

... of reported country exposure. Under the Firm's internal country risk measurement framework: • Lending exposures are measured at the total committed amount (funded and unfunded), net of the allowance for credit losses and cash and marketable securities collateral received. • Securities financing... -

Page 140

...business through the Firm's credit, market, and operational risk governance, rather than through Country Risk Management. The Firm's internal country risk reporting differs from the reporting provided under the Federal Financial Institutions Examination Council ("FFIEC") bank regulatory requirements... -

Page 141

... risk management, valuation and regulatory capital models used by the Firm. The Model Risk review and governance functions are part of the Firm's Model Risk and Development unit, and the Firmwide Model Risk and Development Executive reports to the Firm's CRO. Models are tiered based on an internal... -

Page 142

...risk events. The Firm has taken steps to reduce its exposure to principal investments, selling portions of Corporate's One Equity Partners private equity portfolio and the CIB's Global Special Opportunities Group equity and mezzanine financing portfolio. 140 JPMorgan Chase & Co./2014 Annual Report -

Page 143

...109. JPMorgan Chase & Co./2014 Annual Report Risk self-assessment In order to evaluate and monitor operational risk, the lines of business and functions utilize the Firm's standard risk and control self-assessment ("RCSA") process and supporting architecture. The RCSA process requires management to... -

Page 144

...ensure that the Firm has the ability to recover its critical business functions and supporting assets (i.e., staff, technology and facilities) in the event of a business interruption, and to remain in compliance with global laws and regulations as they relate to resiliency risk. The program includes... -

Page 145

..., providing technological capabilities to support remote work capacity for displaced staff and accommodation of employees at alternate locations. JPMorgan Chase continues to coordinate its global resiliency program across the Firm and mitigate business continuity risks by reviewing and testing... -

Page 146

... risk, the Firm's Compliance teams work closely with the Operating Committee and senior management to provide independent review and oversight of the lines of business operations, with a focus on compliance with applicable global, regional and local laws and regulations. In recent years, the Firm... -

Page 147

... risk is the risk of a failure to exercise the applicable high standard of care, to act in the best interests of clients or to treat clients fairly, as required under applicable law or regulation. Depending on the fiduciary activity and capacity in which the Firm is acting, federal and state... -

Page 148

... of business equity Regulatory capital The Federal Reserve establishes capital requirements, including well-capitalized standards, for the consolidated financial holding company. The Office of the Comptroller of the Currency ("OCC") establishes similar capital requirements and standards for the Firm... -

Page 149

... related to debt and equity securities classified as AFS as well as for defined benefit pension and other postretirement employee benefit ("OPEB") plans), less certain deductions for goodwill, MSRs and deferred tax assets that arise from net operating loss ("NOL") and tax credit carryforwards. Tier... -

Page 150

... other intangible assets, investments in certain subsidiaries, and the total adjusted carrying value of nonfinancial equity investments that are subject to deductions from Tier 1 capital. Risk-based capital regulatory minimums The Basel III rules include minimum capital ratio requirements that are... -

Page 151

...rules and JPMorgan Chase & Co./2014 Annual Report on the application of such rules to the Firm's businesses as currently conducted. The actual impact on the Firm's capital ratios and SLR as of the effective date of the rules may differ from the Firm's current estimates depending on changes the Firm... -

Page 152

... represents Tier 1 common capital. Year ended December 31, (in millions) Basel I CET1 capital at December 31, 2013 Effect of rule changes(a) Basel III Advanced Fully Phased-In CET1 capital at December 31, 2013 Net income applicable to common equity Dividends declared on common stock Net purchases of... -

Page 153

... driver of the change. Year ended December 31, (in millions) Credit risk RWA $1,223 (168) Market risk RWA $ 165 (4) Operational risk RWA NA 375 Total RWA $1,388 203 Basel III Transitional Basel III Transitional capital requirements became effective on January 1, 2014, and will become fully... -

Page 154

...Reserve uses the CCAR and Dodd-Frank Act stress test processes to ensure that large bank holding companies have sufficient capital during periods of economic and financial stress, and have robust, forward-looking capital assessment and planning processes in place that address each BHC's unique risks... -

Page 155

...is measured and internal targets for expected returns are established as key measures of a business segment's performance. Line of business equity Year ended December 31, (in billions) Consumer & Community Banking Corporate & Investment Bank Commercial Banking Asset Management Corporate Total common... -

Page 156

...internal capital generation; and alternative investment opportunities. The repurchase program does not include specific price targets or timetables; may be executed through open market purchases or privately negotiated transactions, or utilizing Rule 10b5-1 programs; and may be suspended at any time... -

Page 157

... required to notify the Securities and Exchange Commission ("SEC") in the event that tentative net capital is less than $5.0 billion, in accordance with the market and credit risk standards of Appendix E of the Net Capital Rule. As of December 31, 2014, JPMorgan Securities had tentative net capital... -

Page 158

... access to wholesale funding markets. LCR and NSFR In December 2010, the Basel Committee introduced two new measures of liquidity risk: the liquidity coverage ratio ("LCR"), which is intended to measure the amount of "highquality liquid assets" ("HQLA") held by the Firm in relation to estimated net... -

Page 159

... to fund loans are primarily invested in the Firm's investment securities portfolio or deployed in cash or other short-term liquid investments based on their interest rate and liquidity risk characteristics. Capital markets secured financing assets and trading assets are primarily funded by the Firm... -

Page 160

... line of business, the period-end and average deposit balances as of and for the years ended December 31, 2014 and 2013. Deposits As of or for the period ended December 31, (in millions) Consumer & Community Banking Corporate & Investment Bank Commercial Banking Asset Management Corporate Total Firm... -

Page 161

... and student loans. The Firm's wholesale businesses also securitize loans for clientdriven transactions; those client-driven loan securitizations are not considered to be a source of funding for the Firm and are not included in the table. (f) Includes long-term structured notes which are secured... -

Page 162

... changes in the Firm's credit ratings, financial ratios, earnings, or stock price. Critical factors in maintaining high credit ratings include a stable and diverse earnings stream, strong capital ratios, strong credit quality and risk management controls, diverse funding sources, and disciplined... -

Page 163

... for credit losses JPMorgan Chase's allowance for credit losses covers the retained consumer and wholesale loan portfolios, as well as the Firm's consumer and wholesale lending-related commitments. The allowance for loan losses is intended to adjust the carrying value of the Firm's loan assets to... -

Page 164

... Firm uses a risk rating system to determine the credit quality of its wholesale loans and lending-related commitments. In assessing the risk rating of a particular loan or lending-related commitment, among the factors considered are the obligor's debt capacity and financial flexibility, the level... -

Page 165

... level 3 of the valuation hierarchy. For further information, see Note 3. December 31, 2014 (in billions, except ratio data) Trading debt and equity instruments Derivative receivables Trading assets AFS securities Loans MSRs Private equity investments(a) Other Total assets measured at fair value... -

Page 166

... decreases in home prices that result in increased credit losses. Declines in business performance, increases in equity capital requirements, or increases in the estimated cost of equity, could cause the estimated fair values of the Firm's reporting units or their associated goodwill to decline... -

Page 167

... certain NOLs. The Firm performs regular reviews to ascertain whether deferred tax assets are realizable. These reviews include management's estimates and assumptions regarding future taxable income, which also incorporates various tax planning strategies, including strategies that may be available... -

Page 168

... 2010 of the accounting guidance for VIEs for certain investment funds, including mutual funds, private equity funds and hedge funds. In addition, the guidance amends the evaluation of fees paid to a decision maker or a service provider, and exempts certain money market funds from consolidation. The... -

Page 169

... period depends on the size and characteristics of the Firm's portfolio of affordable housing investments; the estimated increase for 2014 is approximately $900 million. The effect of this guidance on the Firm's net income is not expected to be material. JPMorgan Chase & Co./2014 Annual Report 167 -

Page 170

...The Firm's nonexchange-traded commodity derivative contracts are primarily energy-related. The following table summarizes the changes in fair value for nonexchange-traded commodity derivative contracts for the year ended December 31, 2014. Year ended December 31, 2014 (in millions) Net fair value of... -

Page 171

... security of its financial, accounting, technology, data processing and other operating systems and facilities; • The other risks and uncertainties detailed in Part I, Item 1A: Risk Factors in the Firm's Annual Report on Form 10K for the year ended December 31, 2014. Any forward-looking statements... -

Page 172

... LLP, an independent registered public accounting firm, as stated in their report which appears herein. James Dimon Chairman and Chief Executive Officer Marianne Lake Executive Vice President and Chief Financial Officer February 24, 2015 170 JPMorgan Chase & Co./2014 Annual Report -

Page 173

... on these financial statements and on the Firm's internal control over financial reporting based on our integrated audits. We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the... -

Page 174

Consolidated statements of income Year ended December 31, (in millions, except per share data) Revenue Investment banking fees Principal transactions Lending- and deposit-related fees Asset management, administration and commissions Securities gains(a) Mortgage fees and related income Card income ... -

Page 175

Consolidated statements of comprehensive income Year ended December 31, (in millions) Net income Other comprehensive income/(loss), after-tax Unrealized gains/(losses) on investment securities Translation adjustments, net of hedges Cash flow hedges Defined benefit pension and OPEB plans Total other ... -

Page 176

... Total assets(a) $ Liabilities Deposits (included $8,807 and $6,624 at fair value) $ Federal funds purchased and securities loaned or sold under repurchase agreements (included $2,979 and $5,426 at fair value) Commercial paper Other borrowed funds (included $14,739 and $13,306 at fair value) Trading... -

Page 177

...at cost Balance at January 1 Reissuance from RSU Trust Balance at December 31 Treasury stock, at cost Balance at January 1 Purchase of treasury stock Reissuance from treasury stock Share repurchases related to employee stock-based compensation awards Balance at December 31 Total stockholders' equity... -

Page 178

... cash used in investing activities Financing activities Net change in: Deposits Federal funds purchased and securities loaned or sold under repurchase agreements Commercial paper and other borrowed funds Beneficial interests issued by consolidated variable interest entities Proceeds from long-term... -

Page 179

...with operations worldwide. The Firm is a leader in investment banking, financial services for consumers and small business, commercial banking, financial transaction processing and asset management. For a discussion of the Firm's business segments, see Note 33. The accounting and financial reporting... -

Page 180

... using applicable exchange rates. Gains and losses relating to translating functional currency financial statements for U.S. reporting are included in other comprehensive income/(loss) ("OCI") within stockholders' equity. Gains and losses relating to nonfunctional currency transactions, including... -

Page 181

... management services to the acquirer of the investments sold in the Private Equity sale and for the portion of private equity investments retained by the Firm. Upon closing, this transaction did not have a material impact on the Firm's Consolidated balance sheets or its results of operations. Note... -

Page 182

... not limited to yield curves, interest rates, volatilities, equity or debt prices, foreign exchange rates and credit curves. Valuation adjustments may be made to ensure that financial instruments are recorded at fair value, as described below. The level of precision in estimating unobservable market... -

Page 183

... be made when positions are valued using prices or input parameters to valuation models that are unobservable due to a lack of market activity or because they cannot be implied from observable market data. Such prices or parameters must be estimated and are, therefore, subject to management judgment... -

Page 184

... value, see Note 14. Loans - consumer Held for investment consumer loans, excluding credit card Level 2 or 3 Predominantly level 3 Valuations are based on discounted cash flows, which consider: Predominantly level 3 • Discount rates (derived from primary origination rates and market activity... -

Page 185

...Credit spreads • Credit rating data Valued using observable market prices or data Exchange-traded derivatives that are actively traded and valued using the exchange price, and over-the-counter contracts where quoted prices are available in an active market. Derivatives that are valued using models... -

Page 186

... using observable market prices less adjustments for relevant restrictions, where applicable Fund investments (i.e., mutual/ Net asset value ("NAV") collective investment funds, • NAV is validated by sufficient level of observable activity (i.e., private equity funds, hedge purchases and sales... -

Page 187

... deposit, bankers' acceptances and commercial paper Non-U.S. government debt securities Corporate debt securities Loans(b) Asset-backed securities Total debt instruments Equity securities Physical commodities(c) Other Total debt and equity instruments(d) Derivative receivables: Interest rate Credit... -

Page 188

... other assets Total assets measured at fair value on a recurring basis Deposits Federal funds purchased and securities loaned or sold under repurchase agreements Other borrowed funds Trading liabilities: Debt and equity instruments(d) Derivative payables: Interest rate Credit Foreign exchange Equity... -

Page 189

...2013, respectively; this is exclusive of the netting benefit associated with cash collateral, which would further reduce the level 3 balances. (f) Private equity instruments represent investments within the Corporate line of business. The cost basis of the private equity investment portfolio totaled... -

Page 190

... by the Firm at each balance sheet date. For the Firm's derivatives and structured notes positions classified within level 3, the equity and interest rate correlation inputs used in estimating fair value were concentrated at the upper end of the range presented, while the credit correlation inputs... -

Page 191

... cash flows 393 Mortgage servicing rights Private equity direct investments Private equity fund investments Long-term debt, other borrowed funds, and deposits(d) 7,436 2,054 421 15,069 Market comparables Discounted cash flows Market comparables Net asset value Option pricing 15% - 65% 50 - $90... -

Page 192

... of an asset is the interest rate used to discount future cash flows in a discounted cash flow calculation. An increase in the yield, in isolation, would result in a decrease in a fair value measurement. Credit spread - The credit spread is the amount of additional annualized return over the market... -

Page 193

...the fair value hierarchy; as these level 1 and level 2 risk management instruments are not included below, the gains or losses in the following tables do not reflect the effect of the Firm's risk management activities related to such level 3 instruments. JPMorgan Chase & Co./2014 Annual Report 191 -

Page 194

...rate Credit Foreign exchange Equity Commodity Total net derivative receivables Available-for-sale securities: Asset-backed securities Other Total available-for-sale securities Loans Mortgage servicing rights Other assets: Private equity investments All other Fair value at January 1, 2014 Purchases... -

Page 195

... Credit Foreign exchange Equity Commodity Total net derivative receivables Available-for-sale securities: Asset-backed securities Other Total available-for-sale securities Loans Mortgage servicing rights Other assets: Private equity investments All other (a) Fair value at January 1, 2013 Purchases... -

Page 196

... of U.S. states and municipalities Non-U.S. government debt securities Corporate debt securities Loans Asset-backed securities Total debt instruments Equity securities Other Total trading assets - debt and equity instruments Net derivative receivables:(a) Interest rate Credit Foreign exchange Equity... -

Page 197

... billion of net gains on trading assets - debt and equity instruments, largely driven by market making and credit spread tightening in nonagency mortgage-backed securities and trading loans, and the impact of market movements on client-driven financing transactions; • $1.6 billion of net gains on... -

Page 198

... JPMorgan Chase & Co./2014 Annual Report the-counter ("OTC") derivatives and structured notes. The Firm's FVA framework leverages its existing CVA and DVA calculation methodologies, and considers the fact that the Firm's own credit risk is a significant component of funding costs. The key inputs... -

Page 199

...fair value of JPMorgan Chase's assets and liabilities. For example, the Firm has developed long-term relationships with its customers through its deposit base and credit card accounts, commonly referred to as core deposit intangibles and credit card relationships. In the opinion of management, these... -

Page 200

...Total estimated fair value - $ - 0.3 39.8 316.1 65.2 (in billions) Financial assets Cash and due from banks Deposits with banks Accrued interest and accounts receivable Federal funds sold and securities purchased under resale agreements Securities borrowed Securities, held-to-maturity(a) Loans, net... -

Page 201

... this Note. Trading assets and liabilities Trading assets include debt and equity instruments owned by JPMorgan Chase ("long" positions) that are held for client market-making and client-driven activities, as well as for certain risk management activities, certain loans managed on a fair value basis... -

Page 202

... credit risk (DVA) related to structured notes were $20 million, $(337) million and $(340) million for the years ended December 31, 2014, 2013 and 2012, respectively. These totals include such changes for structured notes classified within deposits and other borrowed funds, as well as long-term debt... -

Page 203

...,858 $ 4,023 2,150 12,348 710 December 31, 2013 Other Long-term borrowed debt funds $ 9,516 $ 4,248 2,321 11,082 1,260 (in millions) Risk exposure Interest rate Credit Foreign exchange Equity Commodity Total structured notes Deposits Total Deposits Total 460 $ 2,119 $ 13,437 450 211 12,412 644... -

Page 204

... credit card Total credit card Total consumer Wholesale-related Real Estate Banks & Finance Cos Healthcare Oil & Gas Consumer Products Asset Managers State & Municipal Govt Retail & Consumer Services Utilities Central Govt Technology Machinery & Equipment Mfg Transportation Business Services... -

Page 205

.... Customers use derivatives to mitigate or modify interest rate, credit, foreign exchange, equity and commodity risks. The Firm actively manages the risks from its exposure to these derivatives by entering into other derivative transactions or by purchasing or selling other financial instruments... -

Page 206

...There are three types of hedge accounting designations: fair value hedges, cash flow hedges and net investment hedges. JPMorgan Chase uses fair value hedges primarily to hedge fixed-rate long-term debt, AFS securities and certain commodities inventories. For qualifying fair value hedges, the changes... -

Page 207

... relationships: Interest rate Credit Commodity Interest rate and foreign exchange • Various • Various Manage the risk of the mortgage pipeline, warehouse loans and MSRs Specified risk management Manage the credit risk of wholesale lending exposures Manage the risk of certain commodities-related... -

Page 208

... rate contracts Credit derivatives(a)(b) Foreign exchange contracts Cross-currency swaps Spot, futures and forwards Written options Purchased options Total foreign exchange contracts Equity contracts Swaps(a) Futures and forwards(a) Written options Purchased options Total equity contracts Commodity... -

Page 209

... hedge accounting relationships or not) and contract type. Free-standing derivative receivables and payables(a) Gross derivative receivables December 31, 2014 (in millions) Trading assets and liabilities Interest rate Credit Foreign exchange Equity Commodity Total fair value of trading assets and... -

Page 210

... 78,975 $ 15,734 1,180,467 $ 15,734 65,759 (a) Exchange-traded derivative amounts that relate to futures contracts are settled daily. (b) Included cash collateral netted of $74.0 billion and $63.9 billion at December 31, 2014, and 2013, respectively. 208 JPMorgan Chase & Co./2014 Annual Report -

Page 211

... payables 2013 Amounts netted on the Consolidated balance sheets December 31, (in millions) U.S. GAAP nettable derivative payables Interest rate contracts: OTC OTC-cleared Exchange-traded(a) Total interest rate contracts Credit contracts: OTC OTC-cleared Total credit contracts Foreign exchange... -

Page 212

... The following table shows the impact of a single-notch and two-notch downgrade of the long-term issuer ratings of JPMorgan Chase & Co. and its subsidiaries, predominantly JPMorgan Chase Bank, National Association ("JPMorgan Chase Bank, N.A."), at December 31, 2014 and 2013, related to OTC and OTC... -

Page 213

... in income Total income statement impact $ 1,305 (253) 194 $ 1,246 $ Income statement impact due to: Hedge ineffectiveness(d) $ 131 - 42 173 $ Excluded components(e) $ 1,174 (253) 152 1,073 Year ended December 31, 2014 (in millions) Contract type Interest rate(a) Foreign exchange Commodity(c) Total... -

Page 214

Notes to consolidated financial statements Cash flow hedge gains and losses The following tables present derivative instruments, by contract type, used in cash flow hedge accounting relationships, and the pretax gains/(losses) recorded on such derivatives, for the years ended December 31, 2014, 2013... -

Page 215

... Firm actively manages a portfolio of credit derivatives by purchasing and selling credit protection, predominantly on corporate debt obligations, to meet the needs of customers. Second, as an end-user, the Firm uses credit derivatives to manage credit risk associated with lending exposures (loans... -

Page 216

... notional amount of net protection sold, as the amount actually required to be paid on the contracts takes into account the recovery value of the reference obligation at the time of settlement. The Firm manages the credit risk on contracts to sell protection by purchasing protection with identical... -

Page 217

.... This revision had no impact on the Firm's Consolidated balance sheets or its results of operations. (c) Amounts are shown on a gross basis, before the benefit of legally enforceable master netting agreements and cash collateral received by the Firm. JPMorgan Chase & Co./2014 Annual Report 215 -

Page 218

... Total underwriting Advisory Total investment banking fees $ 1,571 3,340 4,911 1,631 $ 6,542 $ 1,499 3,537 5,036 1,318 $ 6,354 $ $ 1,026 3,290 4,316 1,492 5,808 Year ended December 31, (in millions) Trading revenue by instrument type (a) Interest rate(b) Credit (c) 2014 2013 2012 purchase, sale... -

Page 219

... of credit, financial guarantees, deposit-related fees in lieu of compensating balances, cash management-related activities or transactions, deposit accounts and other loan-servicing activities. These fees are recognized over the period in which the related service is provided. Asset management... -

Page 220

... follows. Year ended December 31, (in millions) Interest income Loans Taxable securities Non-taxable securities(a) Total securities Trading assets(b) Federal funds sold and securities purchased under resale agreements Securities borrowed (c) Deposits with banks Other assets(d) Total interest income... -

Page 221

... exchange impact and other Benefit obligation, end of year Change in plan assets Fair value of plan assets, beginning of year Actual return on plan assets Firm contributions Employee contributions Benefits paid Foreign exchange impact and other Fair value of plan assets, end of year Net funded... -

Page 222

Notes to consolidated financial statements Gains and losses For the Firm's defined benefit pension plans, fair value is used to determine the expected return on plan assets. Amortization of net gains and losses is included in annual net periodic benefit cost if, as of the beginning of the year, the ... -

Page 223

...-term rate of return for U.S. defined benefit pension and OPEB plan assets is a blended average of the investment advisor's projected long-term (10 years or more) returns for the various asset classes, weighted by the asset allocation. Returns on asset classes are developed using a forward-looking... -

Page 224

... 2.75 - 4.60 2014 2013 Non-U.S. 2014 2013 Weighted-average assumptions used to determine net periodic benefit costs U.S. Year ended December 31, Discount rate: Defined benefit pension plans OPEB plans Expected long-term rate of return on plan assets: Defined benefit pension plans OPEB plans Rate of... -

Page 225

... strategy and asset allocation The Firm's U.S. defined benefit pension plan assets are held in trust and are invested in a well-diversified portfolio of equity and fixed income securities, cash and cash equivalents, and alternative investments (e.g., hedge funds, private equity, real estate and real... -

Page 226

... goods Banks and finance companies Business services Energy Materials Real Estate Other Total equity securities Common/collective trust funds(a) Limited partnerships:(b) Hedge funds Private equity Real estate Real assets(c) Total limited partnerships Corporate debt securities(d) U.S. federal, state... -

Page 227

... Consumer goods Banks and finance companies Business services Energy Materials Real estate Other Total equity securities Common/collective trust funds(a) Limited partnerships: Hedge funds Private equity Real estate Real assets (c) (b) Non-U.S. defined benefit pension plans(i) Level 1 $ 221 86... -

Page 228