Amtrak 2014 Annual Report Download - page 3

Download and view the complete annual report

Please find page 3 of the 2014 Amtrak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

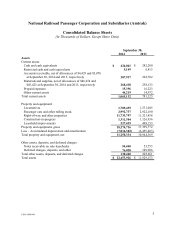

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

2

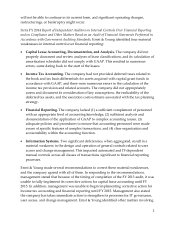

will not be able to continue in its current form, and significant operating changes,

restructurings, or bankruptcy might occur.

In its FY 2014 Report of Independent Auditors on Internal Controls Over Financial Reporting

and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in

Accordance with Government Auditing Standards, Ernst & Young identified four material

weaknesses in internal control over financial reporting:

Capital Lease Accounting, Documentation, and Analysis. The company did not

properly document and review analyses of lease classifications, and its calculation of

amortization schedules did not comply with GAAP. This resulted in numerous

errors, some dating back to the start of the leases.

Income Tax Accounting. The company had not provided deferred taxes related to

the book and tax basis differentials for assets acquired with capital grant funds in

accordance with GAAP, and there were numerous errors in the calculation of the

income tax provision and related accounts. The company did not appropriately

assess and document its consideration of key assumptions, the realizability of the

deferred tax assets, and the execution costs estimate associated with the tax planning

strategy.

Financial Reporting. The company lacked (1) a sufficient complement of personnel

with an appropriate level of accounting knowledge, (2) sufficient analysis and

documentation of the application of GAAP to complex accounting issues, (3)

adequate policies and procedures to ensure that accounting personnel were made

aware of specific features of complex transactions, and (4) clear organization and

accountability within the accounting function.

Information Systems. Two significant deficiencies, when aggregated, result in a

material weakness in the design and operation of general controls related to user

access and change management. This impacted automated and IT-dependent

manual controls across all classes of transactions significant to financial reporting

processes.

Ernst & Young made several recommendations to correct these material weaknesses,

and the company agreed with all of them. In responding to the recommendations,

management stated that because of the timing of completion of the FY 2013 audit, it was

unable to fully implement its corrective actions for capital lease accounting until FY

2015. In addition, management was unable to begin implementing corrective action for

income tax accounting and financial reporting until FY 2015. Management also stated

the company has taken immediate action to strengthen its processes for IT governance,

user access, and change management. Ernst & Young identified other matters involving