Sallie Mae 2011 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2011 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

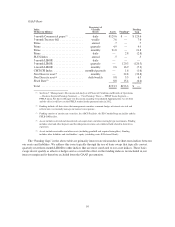

|

|

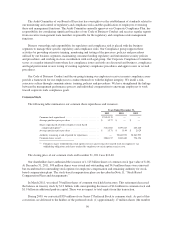

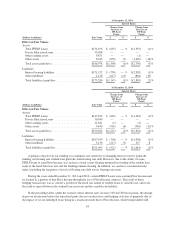

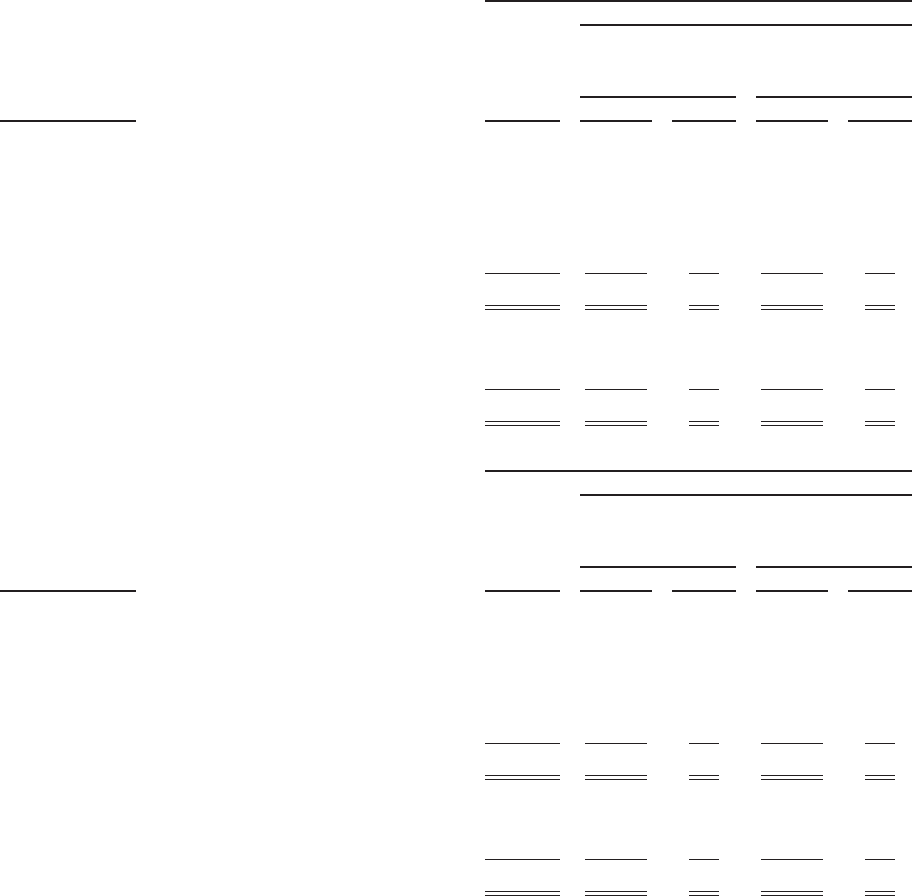

At December 31, 2011

Interest Rates:

Change from

Increase of

100 Basis

Points

Change from

Increase of

300 Basis

Points

(Dollars in millions) Fair Value $ % $ %

Effect on Fair Values

Assets

Total FFELP Loans ............................ $134,196 $ (665) — % $(1,335) (1)%

Private Education Loans ........................ 33,968 — — — —

Other earning assets ............................ 9,871 — — (1) —

Other assets .................................. 8,943 (639) (7) (1,420) (16)%

Total assets gain/(loss) .......................... $186,978 $(1,304) (1)% $(2,756) (1)%

Liabilities

Interest bearing liabilities ....................... $171,152 $ (730) — % $(2,002) (1)%

Other liabilities ............................... 4,128 (617) (15) (801) (19)

Total liabilities (gain)/loss ....................... $175,280 $(1,347) (1)% $(2,803) (2)%

At December 31, 2010

Interest Rates:

Change from

Increase of

100 Basis

Points

Change from

Increase of

300 Basis

Points

(Dollars in millions) Fair Value $ % $ %

Effect on Fair Values

Assets

Total FFELP Loans ............................ $147,163 $ (649) — % $(1,318) (1)%

Private Education Loans ........................ 30,949 — — — —

Other earning assets ............................ 11,641 (1) — (2) —

Other assets .................................. 9,449 (565) (6) (996) (11)%

Total assets gain/(loss) .......................... $199,202 $(1,215) (1)% $(2,316) (1)%

Liabilities

Interest bearing liabilities ....................... $187,959 $ (704) — % $(1,938) (1)%

Other liabilities ............................... 3,136 (217) (7) 257 8

Total liabilities (gain)/loss ....................... $191,095 $ (921) — % $(1,681) (1)%

A primary objective in our funding is to minimize our sensitivity to changing interest rates by generally

funding our floating rate student loan portfolio with floating rate debt. However, due to the ability of some

FFELP loans to earn Floor Income, we can have a fixed versus floating mismatch in funding if the student loan

earns at the fixed borrower rate and the funding remains floating. In addition, we can have a mismatch in the

index (including the frequency of reset) of floating rate debt versus floating rate assets.

During the years ended December 31, 2011 and 2010, certain FFELP Loans were earning Floor Income and

we locked in a portion of that Floor Income through the use of Floor Income contracts. The result of these

hedging transactions was to convert a portion of the fixed rate nature of student loans to variable rate, and to fix

the relative spread between the student loan asset rate and the variable rate liability.

In the preceding tables, under the scenario where interest rates increase 100 and 300 basis points, the change

in pre-tax net income before the unrealized gains (losses) on derivative and hedging activities is primarily due to

the impact of (i) our unhedged loans being in a fixed-rate mode due to Floor Income, while being funded with

93