Progressive 2015 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2015 Progressive annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

|

|

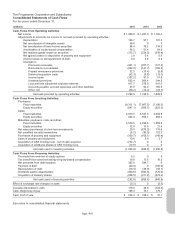

New Accounting Standards In February 2016, the Financial Accounting Standards Board (FASB) released an accounting

standards update (ASU) intended to eliminate the off-balance-sheet accounting for leases. The new guidance will require

lessees to report their operating leases as both an asset and liability on the statement of financial position and disclose key

information about leasing arrangements; the expense recognition will be consistent with existing guidance. The ASU, which

is required to be applied on a modified retrospective basis, will be effective for fiscal years (including interim periods within

those fiscal years) beginning after December 15, 2018 (2019 for calendar-year companies). We are currently evaluating the

impact the guidance will have on our financial statements.

In January 2016, the FASB released an ASU intended to improve the recognition and measurement of financial

instruments. The new guidance will require the changes in fair value of equity securities to be recognized as a component of

net income. The ASU is effective for fiscal years beginning after December 15, 2017 (the first quarter 2018 for calendar-

year companies). The new guidance could create more volatility in net income, but will have no impact on comprehensive

income.

In May 2015, the FASB issued an ASU related to disclosures about short-duration contracts. The disclosures are intended

to provide users of financial statements with more transparent information about an insurance entity’s initial claim estimates

and subsequent adjustments to those estimates, the methodologies and judgments used to estimate claims, and the timing,

frequency, and severity of claims. This standard, which is required to be applied on a retrospective basis, is effective for

fiscal years beginning after December 15, 2015 (2016 for calendar-year companies), except for those disclosures that

require application only to the current period (e.g., information about significant changes in estimation methodologies and

assumptions made in calculating the claim liability for short-duration contracts). We are currently evaluating the impact the

guidance will have on our financial statements.

In May 2015, the FASB issued an ASU related to investments measured at net asset value (NAV). The intent is to exclude

certain investments measured at NAV from the fair value hierarchy. This guidance is effective for annual and interim periods

after December 15, 2015 (January 2016 for calendar-year companies). We did not hold any securities at December 31,

2015, that were priced at NAV. To the extent we acquire such securities, we will follow the guidance to determine the

appropriate treatment in the fair value hierarchy table.

In April 2015, the FASB issued an ASU related to the balance sheet presentation of the cost of issuing debt. This standard

requires that all costs incurred to issue debt be presented in the balance sheet as a direct deduction from the carrying value

of the debt. In August 2015, the FASB further amended this ASU to clarify the treatment of debt issuance costs related to

lines-of-credit arrangements. Registrants can elect to defer and present debt issuance costs related to a line of credit as an

asset and subsequently amortize the costs ratably over the term of the line-of-credit arrangement, regardless of whether

there are any outstanding borrowings on the arrangement. This ASU, which is required to be applied on a retrospective

basis, is effective for fiscal years beginning after December 15, 2015 (2016 for calendar-year companies). We have

historically deducted the majority of our debt issuance costs from the carrying value of the debt; therefore, we do not expect

this standard to have a significant impact on our financial condition, cash flows, or results of operations.

In April 2015, the FASB issued an ASU to clarify guidance around accounting for fees paid in a cloud computing

arrangement. The standard prescribes when a cloud computing arrangement should be treated as software and when it

should be treated as a service contract based on whether the arrangement includes a software license. This ASU, which

allows for both prospective and retrospective methods of adoption, will be effective for annual periods (including interim

periods within those annual periods) beginning after December 15, 2015 (2016 for calendar-year companies). We adopted

this standard on January 1, 2016, on a prospective basis, and do not expect this standard to have a material impact on our

financial condition, cash flows, or results of operations.

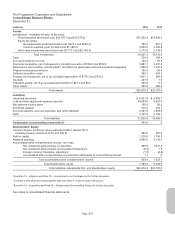

Reclassification For the period ended December 31, 2015, we reclassified goodwill and intangible assets out of “other

assets” to be reported as separate line items to conform with the current-year presentation. There was no effect on total

assets.

App.-A-11