PNC Bank 2005 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2005 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

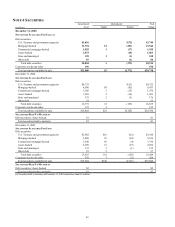

89

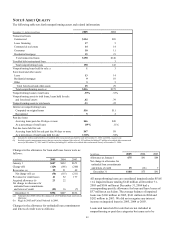

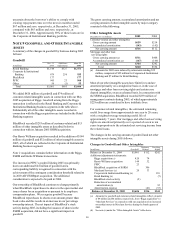

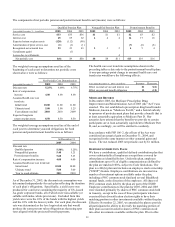

NOTE 8 ASSET QUALITY

The following table sets forth nonperforming assets and related information:

December 31 - dollars in millions 2005 2004

Nonaccrual loans

Commercial $134 $89

Lease financing 17 5

Commercial real estate 14 14

Consumer 10 11

Residential mortgage 15 21

Total nonaccrual loans $190 $140

Troubled debt restructured loan 3

Total nonperforming loans 190 143

Nonperforming loans held for sale (a) 1 3

Foreclosed and other assets

Lease 13 14

Residential mortgage 9 10

Other 3 5

Total foreclosed and other assets

25

29

Total nonperforming assets

(b)

$216

$175

Nonperforming loans to total loans .39% .33%

Nonperforming assets to total loans, loans held for sale

and foreclosed assets .42 .39

Nonperforming assets to total assets .23 .22

Interest on nonperforming loans

Computed on original terms $16 $11

Recognized 5 2

Past due loans

Accruing loans past due 90 days or more $46 $49

As a percentage of total loans .09% .11%

Past due loans held for sale

Accruing loans held for sale past due 90 days or more $47 $9

As a percentage of total loans held for sale 1.92% .54%

(a) Includes $1 million and $2 million of troubled debt restructured loans held for sale at December 31, 2005 and 2004, respectively.

(b) Excludes equity management assets that are carried at estimated fair value of $25 million (including $7 million of troubled debt restructured

assets) at December 31, 2005 and $32 million (including $11 million of troubled debt restructured assets) at December 31, 2004.

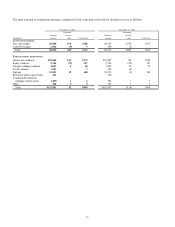

Changes in the allowance for loan and lease losses were as

follows:

In millions 2005

2004 2003

January 1 $607

$632 $673

Charge-offs (129)

(166) (260)

Recoveries (a) 99

51 49

Net charge-offs (a) (30)

(115) (211)

Provision for credit losses 21

52 177

Acquired allowance (b) 23 22

Net change in allowance for

unfunded loan commitments

and letters of credit (25)

16 (7)

December 31 $596

$607 $632

(a) Amounts for 2005 reflect the impact of a $53 million loan recovery in

that year.

(b) Riggs in 2005 and United National in 2004.

Changes in the allowance for unfunded loan commitments

and letters of credit were as follows:

In millions 2005 2004 2003

Allowance at January 1 $75 $91 $84

Net change in allowance for

unfunded loan commitments

and letters of credit 25 (16)

7

December 31 $100 $75 $91

All nonperforming loans are considered impaired under SFAS

114. Impaired loans totaling $148 million at December 31,

2005 and $106 million at December 31, 2004 had a

corresponding specific allowance for loan and lease losses of

$37 million at each date. The average balance of impaired

loans was $106 million in 2005, $141 million in 2004 and

$282 million in 2003. We did not recognize any interest

income on impaired loans in 2005, 2004 or 2003.

Loans and loans held for sale that are not included in

nonperforming or past due categories but cause us to be